No CrossRef data available.

Article contents

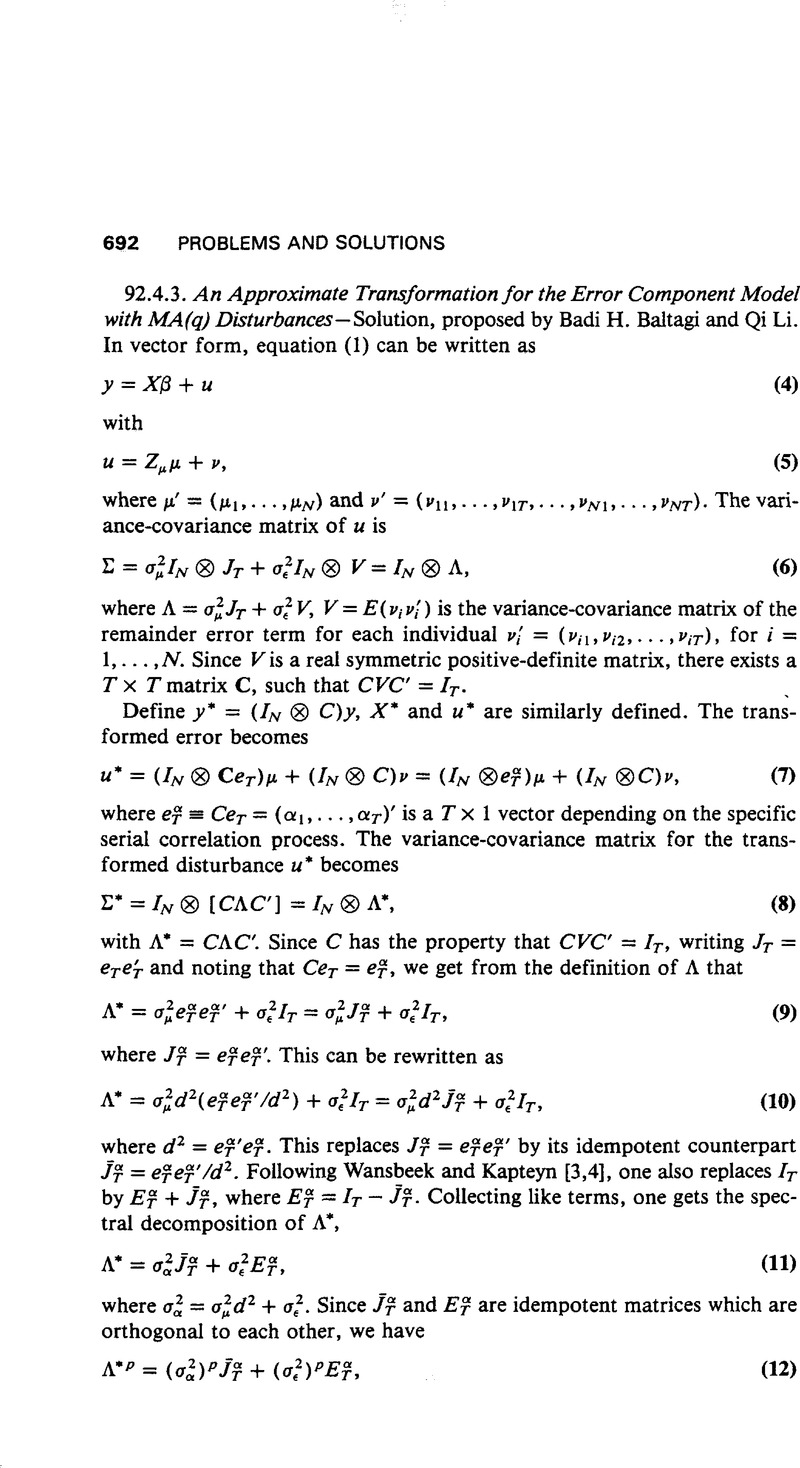

An Approximate Transformation for the Error Component Model with MA(q) Disturbances

Published online by Cambridge University Press: 11 February 2009

Abstract

An abstract is not available for this content so a preview has been provided. Please use the Get access link above for information on how to access this content.

- Type

- Solutions

- Information

- Copyright

- Copyright © Cambridge University Press 1993

References

1Choudhury, A.H. & St. Louis, R.D.. A note on Park and Heikes' (1983) modified approximate estimator for the first-order moving-average process. Journal of Econometrics 46 (1990): 399–406.Google Scholar

2Fuller, W.A. & Battese, G.E.. Estimation of linear models with cross-error structure. Journal of Econometrics 2 (1974): 67–78.Google Scholar

3Wansbeek, T. & Kapteyn, A.. A simple way to obtain the spectral decomposition of variance components models for balanced data. Communications in Statistics A11 (1982): 2105–2112.CrossRefGoogle Scholar

4Wansbeek, T. & Kapteyn, A.. A note on spectral decomposition and maximum likelihood estimation of ANOVA models with balanced data. Statistics and Probability Letters 1 (1983): 213–215.CrossRefGoogle Scholar