Genetic testing has begun to have a significant effect on society. It offers information about individual and population genetic characteristics that can improve predictions about their future health status and can offer opportunities for specific preventative actions. The paper by Deborah Wilson addressed an important issue concerning genetic information, that is, its use in the insurance market and the effect of market incentives on the demand for genetic testing (Wilson, Reference Wilson2006). Wilson adopted the framework of the ‘persuasion game’ literature to show the expected outcomes of different regimes related to the disclosure of genetic information to insurers. According to her analysis, two outcomes should concern policy makers: genetic health information searches made for public health purposes and the efficiency of the insurance market. Equity concerns were not openly addressed in her analysis.

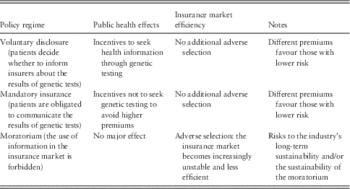

The paper is clearly written and does not require specialised expertise to be understood. However, for the sake of this short essay, I present its main arguments. The insurer and the enrolee make their decisions based on the enrolee’s risk profile; the enrolee can freely decide whether to seek and disclose genetic information and the insurer can require the enrolee to disclose the same information. The regulation of disclosure establishes market rules and, consequently, incentives. Three options are investigated: voluntary disclosure (enrolees are free to disclose their tests results), mandatory disclosure (enrolees must disclose their test results) and a moratorium (tests results cannot be used in the insurance market). The theoretical model is based on a ‘game’ in which the two agents act according to their own interests, whereas fully anticipating the other agent’s strategy. With voluntary disclosure, the enrolee decides whether to be tested and can disregard the effects of disclosure because his or her opportunities in the insurance market will not be worsened by testing. As testing is voluntary, the insurer cannot differentiate between higher-risk and untested individuals and treats both groups as higher risks. Thus, the enrolee, who anticipates the insurer’s strategy, is incentivised to demand genetic testing because he or she can reap some benefits if the results are favourable. In this regime, the insurance market produces incentives that favour testing.

With mandatory disclosure, the central issue is that individuals have incentives to lower their demand for genetic testing because they know that insurers will use the results to differentiate premiums. To reduce this risk, enrolees may refrain from seeking genetic information, even if it could be useful for treatment purposes or personal planning. Paradoxically, mandating the disclosure of tests may result in reducing the amount of genetic information available to both insurers and enrolees.

Finally, with a moratorium (or a general prohibition of the use of genetic information in the insurance market), individuals can decide whether to seek genetic testing information without needing to consider the implications for their insurance opportunities, but at the cost of adverse selection in the insurance market. Faced with uncertainty and an asymmetry of information, insurers might spiral into a situation in which higher premiums reduce the number of enrolees, so that the overall supply of insurance is reduced. Table 1 recaps the effects of the three policy regimes considered in Wilson’s article.

Table 1 Effects of different regimes regarding the disclosure of genetic information

In the following, I discuss whether and how the paper can offer guidance for policy making. The first issue is methodological and concerns the assumptions of the analysis and the general assumptions of similar studies that use models based on rational agents. The main assumption is that agents act rationally. In the model presented by Wilson, the central point is whether it can be assumed that enrolees have enough information and adequate computation skills to understand the effects that their testing decisions have on the insurance market. The model assumes that enrolees anticipate the extent to which genetic test results affect premiums. Given the large number of different genetic tests, the uncertainty surrounding their predictive value for specific diseases, the uncertainty regarding current and future treatment options and the costs of testing, it hardly seems realistic to assume that enrolees base their decisions on such considerations. It is also unlikely that such considerations form even an acceptable approximation of actual behaviour. It is instead likely that ‘heuristic’ approaches prevail and/or that individuals’ choices are completely driven by criteria other than their anticipated effects on the insurance market. However, I understand perfectly that this issue is a radical objection that is common to this entire class of models and that representing human behaviours that violate rationality assumptions may lead to a ‘terra incognita’.

The paper makes what seems to be a reasonable assumption that genetic testing has public health value per se. I am afraid that this assumption is too strong. The debate about the benefits (and costs) of genetic information is still very open, and an excess of optimism is unwarranted. As the paper states, most tests are for multifactorial conditions, and the detection of an anomaly is only one determinant of whether an individual will develop the disease(s). The primary area of uncertainty relates to the information value of an increasing number of genetic tests, and the current major policy issue is how to shape scientific, commercial and policy environments that favour the use of genetics to improve health and personal well-being. In this respect, placing a moratorium on the use of genetic testing might be an acceptable short-term policy because it would temporarily freeze the insurance market’s incentives for demanding (or not demanding) genetic test results. This regime has also the advantage of being more flexible than detailed legislation, which may become difficult to modify.

A major conclusion of Wilson’s article is that a moratorium might result in enough adverse selection to destabilise the insurance market and thus reduce the availability of insurance services. This is a widely debated concern. Put simply, if enrolees conceal information about their risk premiums that would otherwise be used to calculate their risk profiles, an asymmetry of information between enrolees and the insurer will result. This asymmetry would make it possible for enrolees to use their genetic information to make a better evaluation of the expected benefits of the insurance policy than the insurer can. At a given premium, higher-risk individuals reap more benefits from insurance and thus have more incentives to enrol. If insurers cannot identify higher risks, they may react by increasing premiums for everybody; however, this response would lead to additional good risks leaving the market. The anticipated final result will be higher insurance prices and a lower overall supply of insurance services compared with markets in which information is not concealed. Wilson (Reference Wilson2006) reported interesting insights about the relevance of adverse selection: it depends on the elasticity of the demand of low-risk individuals, the proportion of (informed) high-risk types, genetic conditions and the type of insurance (e.g. health care vs life insurance). In addition, insurers generally set premiums on actuarial bases, and at present, it is unlikely that they have enough information to systematically incorporate genetic information into their models. At present, they may have information about very few genetic conditions.

There is some evidence that individuals use genetic information in the insurance market. For life insurance, there is evidence of the adverse selection of individuals who carry the Huntington’s disease genetic mutation (Oster et al., Reference Oster, Shoulson, Quaid and Dorsey2010). In addition, one study found that among women, fear of discrimination in the insurance market has been negatively associated with the decision to undergo genetic testing for breast cancer, and information about increased breast cancer risk was associated with an increase in life insurance purchases (Armstrong et al., Reference Armstrong, Weber, FitzGerald, Hershey, Pauly, Lemaire, Subramanian and Asch2003). However, the study found no evidence of actual premium discrimination (Armstrong et al., Reference Armstrong, Weber, FitzGerald, Hershey, Pauly, Lemaire, Subramanian and Asch2003). Furthermore, in another study, women who had positive results on a similar test did not purchase more life insurance compared with women who did not undergo genetic testing (Godard et al., Reference Godard, Raeburn, Pembrey, Bobrow, Farndon and Ayme2003). More empirical evidence and studies in other socio-economic contexts are needed to investigate the occurrence of adverse selection attributable to genetic testing. It is also important to highlight that classifying enrolees according to genetic information, the action that prevents adverse selection, is often referred to as ‘genetic discrimination’ to reflect a general disapproval of this practice. A recent review of the evidence of genetic discrimination reported scant empirical evidence and no “irrefutable evidence of a systemic problem of genetic discrimination” (Joly et al., Reference Joly, Feze and Simard2013). However, the same study also reports that Huntington’s disease is a notable exception (Joly et al., Reference Joly, Feze and Simard2013). Patients with genetic testing results that are positive for Huntington’s disease are more likely to seek insurance (Oster et al., Reference Oster, Shoulson, Quaid and Dorsey2010), and episodes of supposed discrimination in the life insurance sector have been reported (Joly et al., Reference Joly, Feze and Simard2013). Unsurprisingly, this is a genetic test with a clear and substantial information value.

Wilson did not discuss whether policy regimes might have different outcomes across different types of insurance. At least three main insurance types could be affected by genetic testing: health, disability and life. At least two issues should be considered when analysing different regimes for the disclosure of genetic information across different insurance types. The first concerns the existence of statutory insurance. Currently, in virtually all affluent countries worldwide, health care coverage is universal or almost universal. This means that for most citizens, the main issue is what the statutory insurance covers rather than the risk of incurring higher premiums from private insurers. Regardless of the practice followed by private insurers, compulsory insurance, in which premiums are generally independent of individual risks, reduces the demand for voluntary insurance and reduces the risk that individuals may refrain from being tested to avoid the risk of higher insurance premiums. The situation is clearly different in the case of life insurance because it is a product that is generally not publically funded (although it may be generally tax subsidised). The second issue concerns the calculation of premiums. Given the limited historical data on which estimates of expected costs and premiums can be based, there is considerable uncertainty surrounding the use of genetic information. Presumably, this uncertainty is even greater for health insurance, which requires estimating the expected costs of care and not simply the risk of death. It is likely that disability insurance occupies an area between health care insurance and life insurance in terms of its role as a statutory insurance, the limits of possible incentives for refraining from genetic testing and problems with the actuarial calculation of premiums.

In her paper, Wilson mentions policies that European countries have adopted regarding access to genetic information. The landscape has not changed much in recent years; in virtually all countries, regimes fully prohibit or strongly limit the use of genetic information by insurers (e.g. genetic information can only be applied to premiums for coverage beyond a specified level). Importantly, in 2008, the United States approved the Genetic Information Nondiscrimination Act (GINA), which forbids insurers from requesting, requiring or purchasing genetic information for underwriting purposes; more generally, according to GINA, genetic information cannot be used in health insurance markets. In addition, the 2010 Patient Protection and Affordable Care Act (PPACA) has outlawed any variation in premiums on the basis of information about an enrolee’s health status or genetic information since 2014 (Hudson, Reference Hudson2011). It should be noted, however, that GINA and PPACA do not apply to life, disability or long-term insurance.

Although there are some exceptions (e.g. Polborn et al., Reference Polborn, Hoy and Sadanand2006), the economic analysis of health insurance generally suggests that regulating the disclosure of genetic information may harm citizens by leading to adverse selection (e.g. Hoel et al., Reference Hoel, Iversen, Nilssen and Vislie2006; Barigozzi and Henriet, Reference Barigozzi and Henriet2011). However, the extent of this effect is debatable, and welfarists’ approaches are based on strong rationality assumptions and have little regard for equity and social justice concerns. Legislation in several countries has limited or completely banned the use of genetic information in the health insurance market, an action that contrasts somewhat with most of the insurance economics literature. Sound empirical research should be conducted to monitor the overall effects of these legislations and the validity of the models used to guide policy making.

Genetic testing has begun to have a significant effect on society. It offers information about individual and population genetic characteristics that can improve predictions about their future health status and can offer opportunities for specific preventative actions. The paper by Deborah Wilson addressed an important issue concerning genetic information, that is, its use in the insurance market and the effect of market incentives on the demand for genetic testing (Wilson, Reference Wilson2006). Wilson adopted the framework of the ‘persuasion game’ literature to show the expected outcomes of different regimes related to the disclosure of genetic information to insurers. According to her analysis, two outcomes should concern policy makers: genetic health information searches made for public health purposes and the efficiency of the insurance market. Equity concerns were not openly addressed in her analysis.

The paper is clearly written and does not require specialised expertise to be understood. However, for the sake of this short essay, I present its main arguments. The insurer and the enrolee make their decisions based on the enrolee’s risk profile; the enrolee can freely decide whether to seek and disclose genetic information and the insurer can require the enrolee to disclose the same information. The regulation of disclosure establishes market rules and, consequently, incentives. Three options are investigated: voluntary disclosure (enrolees are free to disclose their tests results), mandatory disclosure (enrolees must disclose their test results) and a moratorium (tests results cannot be used in the insurance market). The theoretical model is based on a ‘game’ in which the two agents act according to their own interests, whereas fully anticipating the other agent’s strategy. With voluntary disclosure, the enrolee decides whether to be tested and can disregard the effects of disclosure because his or her opportunities in the insurance market will not be worsened by testing. As testing is voluntary, the insurer cannot differentiate between higher-risk and untested individuals and treats both groups as higher risks. Thus, the enrolee, who anticipates the insurer’s strategy, is incentivised to demand genetic testing because he or she can reap some benefits if the results are favourable. In this regime, the insurance market produces incentives that favour testing.

With mandatory disclosure, the central issue is that individuals have incentives to lower their demand for genetic testing because they know that insurers will use the results to differentiate premiums. To reduce this risk, enrolees may refrain from seeking genetic information, even if it could be useful for treatment purposes or personal planning. Paradoxically, mandating the disclosure of tests may result in reducing the amount of genetic information available to both insurers and enrolees.

Finally, with a moratorium (or a general prohibition of the use of genetic information in the insurance market), individuals can decide whether to seek genetic testing information without needing to consider the implications for their insurance opportunities, but at the cost of adverse selection in the insurance market. Faced with uncertainty and an asymmetry of information, insurers might spiral into a situation in which higher premiums reduce the number of enrolees, so that the overall supply of insurance is reduced. Table 1 recaps the effects of the three policy regimes considered in Wilson’s article.

Table 1 Effects of different regimes regarding the disclosure of genetic information

In the following, I discuss whether and how the paper can offer guidance for policy making. The first issue is methodological and concerns the assumptions of the analysis and the general assumptions of similar studies that use models based on rational agents. The main assumption is that agents act rationally. In the model presented by Wilson, the central point is whether it can be assumed that enrolees have enough information and adequate computation skills to understand the effects that their testing decisions have on the insurance market. The model assumes that enrolees anticipate the extent to which genetic test results affect premiums. Given the large number of different genetic tests, the uncertainty surrounding their predictive value for specific diseases, the uncertainty regarding current and future treatment options and the costs of testing, it hardly seems realistic to assume that enrolees base their decisions on such considerations. It is also unlikely that such considerations form even an acceptable approximation of actual behaviour. It is instead likely that ‘heuristic’ approaches prevail and/or that individuals’ choices are completely driven by criteria other than their anticipated effects on the insurance market. However, I understand perfectly that this issue is a radical objection that is common to this entire class of models and that representing human behaviours that violate rationality assumptions may lead to a ‘terra incognita’.

The paper makes what seems to be a reasonable assumption that genetic testing has public health value per se. I am afraid that this assumption is too strong. The debate about the benefits (and costs) of genetic information is still very open, and an excess of optimism is unwarranted. As the paper states, most tests are for multifactorial conditions, and the detection of an anomaly is only one determinant of whether an individual will develop the disease(s). The primary area of uncertainty relates to the information value of an increasing number of genetic tests, and the current major policy issue is how to shape scientific, commercial and policy environments that favour the use of genetics to improve health and personal well-being. In this respect, placing a moratorium on the use of genetic testing might be an acceptable short-term policy because it would temporarily freeze the insurance market’s incentives for demanding (or not demanding) genetic test results. This regime has also the advantage of being more flexible than detailed legislation, which may become difficult to modify.

A major conclusion of Wilson’s article is that a moratorium might result in enough adverse selection to destabilise the insurance market and thus reduce the availability of insurance services. This is a widely debated concern. Put simply, if enrolees conceal information about their risk premiums that would otherwise be used to calculate their risk profiles, an asymmetry of information between enrolees and the insurer will result. This asymmetry would make it possible for enrolees to use their genetic information to make a better evaluation of the expected benefits of the insurance policy than the insurer can. At a given premium, higher-risk individuals reap more benefits from insurance and thus have more incentives to enrol. If insurers cannot identify higher risks, they may react by increasing premiums for everybody; however, this response would lead to additional good risks leaving the market. The anticipated final result will be higher insurance prices and a lower overall supply of insurance services compared with markets in which information is not concealed. Wilson (Reference Wilson2006) reported interesting insights about the relevance of adverse selection: it depends on the elasticity of the demand of low-risk individuals, the proportion of (informed) high-risk types, genetic conditions and the type of insurance (e.g. health care vs life insurance). In addition, insurers generally set premiums on actuarial bases, and at present, it is unlikely that they have enough information to systematically incorporate genetic information into their models. At present, they may have information about very few genetic conditions.

There is some evidence that individuals use genetic information in the insurance market. For life insurance, there is evidence of the adverse selection of individuals who carry the Huntington’s disease genetic mutation (Oster et al., Reference Oster, Shoulson, Quaid and Dorsey2010). In addition, one study found that among women, fear of discrimination in the insurance market has been negatively associated with the decision to undergo genetic testing for breast cancer, and information about increased breast cancer risk was associated with an increase in life insurance purchases (Armstrong et al., Reference Armstrong, Weber, FitzGerald, Hershey, Pauly, Lemaire, Subramanian and Asch2003). However, the study found no evidence of actual premium discrimination (Armstrong et al., Reference Armstrong, Weber, FitzGerald, Hershey, Pauly, Lemaire, Subramanian and Asch2003). Furthermore, in another study, women who had positive results on a similar test did not purchase more life insurance compared with women who did not undergo genetic testing (Godard et al., Reference Godard, Raeburn, Pembrey, Bobrow, Farndon and Ayme2003). More empirical evidence and studies in other socio-economic contexts are needed to investigate the occurrence of adverse selection attributable to genetic testing. It is also important to highlight that classifying enrolees according to genetic information, the action that prevents adverse selection, is often referred to as ‘genetic discrimination’ to reflect a general disapproval of this practice. A recent review of the evidence of genetic discrimination reported scant empirical evidence and no “irrefutable evidence of a systemic problem of genetic discrimination” (Joly et al., Reference Joly, Feze and Simard2013). However, the same study also reports that Huntington’s disease is a notable exception (Joly et al., Reference Joly, Feze and Simard2013). Patients with genetic testing results that are positive for Huntington’s disease are more likely to seek insurance (Oster et al., Reference Oster, Shoulson, Quaid and Dorsey2010), and episodes of supposed discrimination in the life insurance sector have been reported (Joly et al., Reference Joly, Feze and Simard2013). Unsurprisingly, this is a genetic test with a clear and substantial information value.

Wilson did not discuss whether policy regimes might have different outcomes across different types of insurance. At least three main insurance types could be affected by genetic testing: health, disability and life. At least two issues should be considered when analysing different regimes for the disclosure of genetic information across different insurance types. The first concerns the existence of statutory insurance. Currently, in virtually all affluent countries worldwide, health care coverage is universal or almost universal. This means that for most citizens, the main issue is what the statutory insurance covers rather than the risk of incurring higher premiums from private insurers. Regardless of the practice followed by private insurers, compulsory insurance, in which premiums are generally independent of individual risks, reduces the demand for voluntary insurance and reduces the risk that individuals may refrain from being tested to avoid the risk of higher insurance premiums. The situation is clearly different in the case of life insurance because it is a product that is generally not publically funded (although it may be generally tax subsidised). The second issue concerns the calculation of premiums. Given the limited historical data on which estimates of expected costs and premiums can be based, there is considerable uncertainty surrounding the use of genetic information. Presumably, this uncertainty is even greater for health insurance, which requires estimating the expected costs of care and not simply the risk of death. It is likely that disability insurance occupies an area between health care insurance and life insurance in terms of its role as a statutory insurance, the limits of possible incentives for refraining from genetic testing and problems with the actuarial calculation of premiums.

In her paper, Wilson mentions policies that European countries have adopted regarding access to genetic information. The landscape has not changed much in recent years; in virtually all countries, regimes fully prohibit or strongly limit the use of genetic information by insurers (e.g. genetic information can only be applied to premiums for coverage beyond a specified level). Importantly, in 2008, the United States approved the Genetic Information Nondiscrimination Act (GINA), which forbids insurers from requesting, requiring or purchasing genetic information for underwriting purposes; more generally, according to GINA, genetic information cannot be used in health insurance markets. In addition, the 2010 Patient Protection and Affordable Care Act (PPACA) has outlawed any variation in premiums on the basis of information about an enrolee’s health status or genetic information since 2014 (Hudson, Reference Hudson2011). It should be noted, however, that GINA and PPACA do not apply to life, disability or long-term insurance.

Although there are some exceptions (e.g. Polborn et al., Reference Polborn, Hoy and Sadanand2006), the economic analysis of health insurance generally suggests that regulating the disclosure of genetic information may harm citizens by leading to adverse selection (e.g. Hoel et al., Reference Hoel, Iversen, Nilssen and Vislie2006; Barigozzi and Henriet, Reference Barigozzi and Henriet2011). However, the extent of this effect is debatable, and welfarists’ approaches are based on strong rationality assumptions and have little regard for equity and social justice concerns. Legislation in several countries has limited or completely banned the use of genetic information in the health insurance market, an action that contrasts somewhat with most of the insurance economics literature. Sound empirical research should be conducted to monitor the overall effects of these legislations and the validity of the models used to guide policy making.