Public investments can have significant impact on land values; for example, climate resilience is highly valued by tenants and property developers.Footnote 1 Infrastructure investment can have a significant and beneficial impact on adjacent land value. “Land value capture” (LVC) mobilizes some or all of the land value increases resulting from actions other than the landowner’s, such as public investments in infrastructure, climate resilience investments, or administrative changes in land use norms and regulations, for the benefit of the community at large.Footnote 2 The objective of LVC is to draw on publicly generated land value increases to enable local administrations to improve their land use management practices and to help them fund infrastructure and service provisions.Footnote 3

A good example of LVC is property tax, which requires landowners to share a percentage of the land value with the government (see for example Box 2.1). The amount of property tax paid increases as the value of the land increases (no matter the cause of the increased value). However, property taxes are generally ill suited to capture the value created by public investments, as they focus on the factual value of the land with improvements. Property tax should aim to differentiate tax burden based on “windfall” benefits of unimproved land location, physical characteristics, and neighboring uses, incentivizing improvement of underused sites by making land idling and holding prime lands for speculation a burdensome option for landowners. This is not an easy transition to make. Property tax reforms can increase the complexities of tax administration, necessitate additional technical capacity for maintaining advanced land cadaster and land reassessment systems, and require that fiscal powers be devolved so that local governments can structure and impose such taxes.Footnote 5

Box 2.1 Property tax reform in Mexicali, Mexico

The city of Mexicali stopped assessing a composite property tax on land and permanent structures and started taxing only the value of the land, requiring major changes in tax administration including changes in land assessment. During the first period of implementation the new taxing system allowed the city to double property tax revenue, prompting other municipalities to implement similar reforms.Footnote 4

There is huge potential in LVC. It represents a more equitable sharing of the cost of public investment, enables government to mobilize more capital to deliver investments, and incentivizes efficient use of public capital and public investments that create real value. For example, for the development of the Canary Wharf Crossrail station in East London, LVC policies yielded more than USD 1.2 billion of the USD 23 billion capital costs for the rail network, also known as the Elizabeth line.Footnote 6

In practice, the successful implementation of LVC requires access to significant data and specific management skills to engage with diverse stakeholders and understand land market conditions; implement comprehensive property monitoring systems; achieve a fluid dialogue among fiscal, planning, and judicial entities; and engage the political resolve of local government leaders.Footnote 7 Land value increases are captured more successfully from landowners and other stakeholders who perceive they are receiving greater benefits from a public intervention than those accruing from business as usual.Footnote 8

Moreover, LVC can improve the sustainability of a project, embedding it with the local community and ensuring that local landowners will benefit from the project in real terms. Projects embedded with the community are more likely to survive changes in government, changes in circumstances, and crises that may arise from time to time.

There is an emerging body of knowledge documenting LVC practices.Footnote 9 LVC is a government policy approach to increase land value and promote equal and sustainable development. It also helps cities finance urban infrastructure by borrowing against property taxes and other LVC revenues. LVC has been well developed by analysts and practitioners.Footnote 10 This chapter will focus on presenting an introduction to LVC and will provide references to facilitate readers seeking an in-depth study.

2.1 LVC Instruments

A number of LVC instruments and approaches have been adopted globally, to meet local needs and to achieve the desired impact, as LVC is extremely context specific. This section will describe some of the key instruments and the lessons learned globally when implementing LVC.Footnote 11

2.1.1 Land for Cash

Excess/underutilized public assets (e.g., land or property) can be disposed (through sale or lease) for cash, which is reinvested in infrastructure. The disposition can require the investor to make additional investments, deliver public goods/services, or carry out other restructuring of the asset. See, for example, Box 2.2 on using abandoned riverfront property for development.

Box 2.2 The city of Ahmedabad, India, opens up Sabarmati riverfront

The Sabarmati riverfront in Ahmedabad was a blighted urban space with large informal settlements, lack of accessibility, and a shortage of new commercial investment or jobs created. The city undertook to support residential redevelopment through USD 17 million of upfront public investment, including a twenty-two-kilometer promenade, slum resettlement, sewage upgrade, environmental rehabilitation, and land reclamation. The result was a well-serviced and walkable waterfront, river access open to public, 202 hectares of land made available for modern development, reduced erosion and exposure of the city to flood risk, and 30 hectares of reclaimed land for sale.Footnote 12

2.1.2 Land as Public Contribution

The public sector “invests” its land (e.g., as an equity contribution into a public–private partnership, joint venture, or other structured arrangement) and the private sector provides capital investment. The public entity captures the value of the land through delivery of public services and its share in project profits.

2.1.3 Land as Collateral

Value can be captured through the sale or lease of publicly owned land whose value has been enhanced by public investment. For example, for a port project, a government can transfer the land surrounding the port to a public–private development corporation. The private entity can then borrow against the land as collateral, to finance the port construction, and repay the debt by selling or leasing the land whose value had been enhanced because of access to the new port.

2.1.4 Developer Exactions and Impact Fees

Developers may be obliged to fund part or all of the costs of infrastructure needed to deliver public services to the site. For example, developer exactions may include the following:

Dedication of land for public use, for example, reserving a certain percentage of land for parks or other public space;

Construction of public improvements, for example, the developer constructs a public road to connect the proposed development with the existing public road network or trunk lines that deliver water and remove wastewater to the neighborhood; or

Funding, for example, the developer provides a financial contribution toward the cost of a section of highway, a new bus stop, or a light rail train station.

It can be technically cumbersome to estimate appropriate exactions to be imposed on a landowner.Footnote 13 With the exception of some robust real estate markets, imposing an extra levy can at times have the effect of discouraging, rather than incentivizing, private sector investment. Any government discretion regarding assessment amounts can create perceptions of corruption and can also result in (expensive) legal challenges, testing whether there is a direct relationship between the project proposed and the exaction required (the “essential nexus” test) and whether the exaction is roughly proportional to the impact created by the project.Footnote 14

2.1.5 Land Pooling/Readjustment

Landowners or occupants voluntarily contribute part of their land for infrastructure development and for sale to cover some project cost. In return, each landowner receives a serviced plot of smaller area with higher value within the same neighborhood. Landowners’ consensus can be difficult to obtain, especially if projects fully rely on voluntary participation. This mechanism requires strong project management and technical capacity, particularly in negotiation and building consensus with landowners; it can also result in disputes, resentment, and legal challenges over participation and the plots allocated as compensation. As an example, land readjustment has been used in Japan since the late nineteenth century for urban expansion, urban development or renewal, disaster prevention, and reconstruction. It was formalized in 1954 by the Land Readjustment Act. Land readjustment needs approval from prefectures and the consent of at least two-thirds of involved landowners and leaseholders. Newly readjusted areas generally include publicly owned plots for sale, which are used to recover development costs. Typically, 30–40 percent of readjusted plots are reserved for public improvements such as infrastructure and utilities.Footnote 15

2.1.6 Betterment Levies/Special Assessments

Instead of value-based property taxes, a betterment levy requires property owners to contribute based on the specific benefit their property receives from public improvements.Footnote 16 Levies can be charged to support a specific project or can be charged periodically against a program of investments (see the example from Chile, in Box 2.3).

Box 2.3 Development in Chacabuco, Chile

In late 1990s Santiago metropolitan region started expanding north in the Chacabuco province with fourteen major real estate projects approved (primarily housing), adding 40,000 new households to the metro region, in an area lacking urban infrastructure services or connectivity to Santiago’s urban core. A twenty-one-kilometer radial highway connecting to central Santiago was to be built with additional forty-one kilometers of byways and interchanges under a concession model, comprising 39 percent government funding and 61 percent developer impact fees levied per buildable housing unit based on each project’s impact on the road network.Footnote 19

For example, in Johannesburg, South Africa, property owners in city improvement districts (CIDs) agree to pay for supplementary services and improvements, such as security measures, infrastructure upgrades, litter collection, and upkeep of public spaces. A CID can be formed when a petition is filed by at least 51 percent of the property owners in a geographic area and then approved by the municipality. The CID levy is compulsory and is calculated based on the value of the individual property and applied pro rata. Other common terms used for CIDs around the world include special assessment districts, benefit assessment districts, local improvement districts, and business improvement districts.Footnote 17

While levies can be imposed by the government, there is an opportunity to use the levy to engage with the local business community, to get them involved in the planning and decision processes, to ensure that infrastructure investments fit well with community needs, and to encourage local economic growth and job creation. Local property owners might consider betterment levies as disguised taxes and demand a public vote, with the legal and institutional complexity that entails.Footnote 18 Approaches that bundle projects citywide have proven more successful.

2.1.7 Density Bonus

The government can permit a developer to increase the maximum allowable development (e.g., floor area or height or buildings), or to change the nature of development, on a site in exchange for funds and/or in-kind support. This works best in cities in which market demand is strong and land availability is limited or for projects or sites in which the developer financial incentives outweigh alternative development options. These additional development rights may require investment that fits with the infrastructure plan, which in turn may improve the leverage effect of infrastructure investment and the additional development rights.

2.1.8 Upzoning

Another approach to LVC using development rights is to change the zoning in and around the infrastructure development to allow for higher value (e.g., from industrial to residential) or more dense use (e.g., increasing allowable floor area ratio). As with density bonuses, upzoning can be successfully deployed as a kind of financing tool for urban regeneration only when sufficient market demand exists and where the system for enforcing zoning regulations and collecting fees/taxes associated with zoning provide sufficient income (see, for example, the up-zoning program in Brazil described in Box 2.4). Upzoning does not allow as much direct control of development investments as density bonuses but may be easier to implement for government.

Box 2.4 Porto Maravilha urban waterfront revitalization, Rio de Janeiro, Brazil

This project involved the revitalization of about 1,250 acres of underutilized and mostly government-owned Guanabara Bay waterfront. It was home to 35,000 residents and is to become a mixed-use mixed-income community of more than 100,000. The development plan includes complete reconstruction of local water, sanitation, and drainage systems, extensive streetscaping and landscaping, installation of three sanitation plants, historic preservation, at least 3,000 social housing units, and cultural and education facilities. The program commenced in 2009 and is to be completed by 2025.

Infrastructure has primarily been financed through Certificates of Additional Construction Potential bonds (CEPACs) – development rights for upzoning sold to developers to raise funds to finance infrastructure construction. More than four million square meters of additional density was sold via CEPACs during 2011–2013, generating USD 1.8 billion in upfront infrastructure funding (the initial purchaser of CEPACs was a state-owned financial bank, which then sold the CEPACs at a profit to private real estate developers as demand rose).Footnote 20

2.1.9 Transferable Development Right

A transferable development right (TDR) uses a similar concept to upzoning or density bonuses to direct new developments away from historic landmarks and other sensitive sites needing preservation to areas that are looking to promote more concentrated developments. One of the key concerns identified around TDRs has been poor planning of additional infrastructure needs to accommodate the incremental development density. For this reason, TDRs must be integrated into comprehensive master development plans.Footnote 21

2.1.10 Joint Ventures

A joint venture can be set up between private investors and government to deliver investments. For example, local businesses and industries may band together to develop specific infrastructure that will benefit their commercial interests and the community, while government provides approvals, permits, and land. The asset developed will be available to and delivered in accordance with the needs of the community. This model has been used in particular for rail and other transport development.Footnote 22

2.2 Bringing Forward LVC Funding

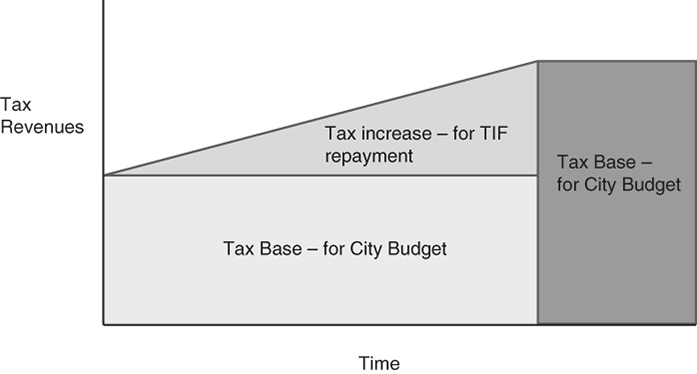

In many cases LVC mechanisms provide additional revenues to government only after the fact, that is, after the land value has increased. Yet, governments need to mobilize these resources in advance to fund the investments that create the land value increase. Various financing mechanisms have been developed to borrow against future LVC. For example, under tax increment financing (TIF), government issues a bond on the capital markets to borrow against anticipated increases in tax receipts that accompany successful urban redevelopment.Footnote 23 The tax revenues, which exceed the taxes that would have been collected without the redevelopment, constitute the “tax increment,” and the TIF captures that gain to pay the bond holders, borrowing against the future anticipated increase in tax revenues generated by the project (see Figure 2.1).

Figure 2.1 The basic TIF model

The performance assessments of TIFs have been mixed. In some cases, TIFs have been overleveraged, diverting significant property tax revenues from other taxing entities.Footnote 24 The tendency has been to overinflate the incremental revenue projections to help secure the upfront financing, which frequently results in large and mounting TIF debts for local governments, in excess of the actual tax revenues generated.Footnote 25

2.3 Lessons Learned

As discussed in the earlier sections, LVC has been implemented under a number of different structures and using instruments appropriate to the context and conditions in which it is implemented. It is a powerful financing and planning tool, but the risks of overreliance, corruption, and gentrification should be carefully addressed. This section shares a few best practice lessons learned from LVC design and implementation.

2.3.1 Consultation with Property Owners, Developers, and Other Stakeholders

Land value increments are captured more successfully when communication channels with landowners and stakeholders exist and the benefits from a proposed public intervention are clearly laid out. Providing opportunities for dialogue between affected owners and the government is important to share information and garner public support.

2.3.2 Setting Appropriate Charges on Owners/Developers

Clear legislation concerning LVC, its processes, the determination of fees and taxes, institutional mandates, affected landowners, and procedures for resolving disputes can reduce conflict, elicit public support, and bring LVC to the political mainstream. Developers are usually receptive to such charges (which are generally passed on to buyers and tenants) as long as approval and other processes are streamlined and decision processes do not carry too much risk.

2.3.3 Consultation with Community

The nature of LVC can make it difficult for the average citizen to understand. It can appear as though government is providing opportunities to property developers and large financiers and/or can look like tax-like impositions on citizens, without an understanding of the advantage received by the government and the community. This is of particular concern in countries where land is a particularly sensitive issue or where communities suffer from the denial of services to certain areas, races, or ethnicities, spatial segregation, or social stratification. In other cases, communities may object out of a desire to avoid change, a “not in my backyard” or NIMBY response, or, more seriously, resistance to resettlement or other more fundamental changes to the community that the government believes are essential. Legal proceedings against the use of LVC instruments are common.Footnote 26 A robust public consultation process is critical. The community can also help identify key risks that require mitigation and challenges that need to be managed, which might not be obvious to those outside of the community. But consultation can also be tricky. The LVC structure is often negotiated/implemented as the development takes shape. Consultation processes will need to adjust as the LVC evolves. Some information will be commercially sensitive, and the government will not want to give away its plans too early to avoid giving property developers too much leverage.

2.3.4 Administrative Capacity

Spatial planning frameworks should clearly define the roles of different levels of government in preparing plans and land use regulations that serve as the baseline for LVC administration. Local governments are mostly responsible for sound planning and land use principles, managing land assets, identifying affected landowners and negotiating with them, setting fees and contributions, and engaging with the community on development plans and terms, among other items. Local governments may face huge challenges delivering on these responsibilities, where they suffer from institutional capacity limitations. Central governments need to provide support to local government, including administrative capacity, policy guidelines, and accurate cadaster and land transaction data for LVC implementation.

2.3.5 Legal Framework

Land value capture structures require the certainty of a legal framework that protects the rights of all parties and allows flexibility in the kind of instruments used to deliver LVC. Avoiding weaknesses in the legal framework, including in enforcement and access to justice for all stakeholders, is critical for a robust LVC framework. Lower-income countries tend to give less discretion to local government officials to implement LVC than do higher income countries, but central governments may have more difficulty implementing LVC.Footnote 27

2.3.6 Land Controls, Cadaster or Land Registry, Technology, and Data Systems

Even where the legal framework is robust, data can be difficult to obtain, and registration of the rights created under an LVC program needs to be formalized, for example, through a land registry or cadaster. In many developing countries these are difficult mechanisms to implement well, but improvements in data generation (through satellites and drones) and software tools have improved significantly the access of developing countries to these mechanisms.

2.3.7 Dynamic Real Estate Market

As LVC leverages the increase in property value, it works best in dynamic real estate markets, that is, in areas that are most responsive to infrastructure upgrades (urban core, waterfront, etc.), where the highest land value differential is achieved. Where timing of disposal of land or capturing land value is important to the LVC model, government may not have the experience or capacity to act in a timely manner. Current spending can become dependent on unrealistic expectations of future land price increases. Given the uncertainty of LVC, it is critical that proceeds be used for infrastructure investment and not for operating budgets.

2.3.8 Transparent Land Sales

Transparent and competitive land auctions can greatly enhance revenues – in some cases increasing the realized land price per square meter by a factor of ten or more. Direct negotiations with land developers are tempting; they seem easier and faster than auctions but generally result in inferior financial and developmental results.

Transparent public accounting of the use of proceeds can help to manage perceptions of corruption or bureaucratic capture. In an effort to maximize LVC, governments may be tempted to use restrictive zoning to drive up land values or abuse developer exactions. This practice can harm the local economy, unduly raise real estate prices, and distort urban development patterns.

2.3.9 Readiness of Financial and Capital Markets

Access to finance for infrastructure developments can benefit from local financial markets that are able to manage and absorb the kind of investment vehicles used for LVC, in particular allowing for borrowing against future LVC revenues like TIFs. Local financial markets may be shallow (not have much available liquidity), short (able to provide debt only over short tenors), or lacking sophistication (where the available types of financial instruments are limited and those working in the industry are not familiar with many of the models discussed here). Regulatory reform in local financial markets can help, as can partnering with global financiers to help local financiers gain experience with LVC instruments.

2.3.10 Fiscal Mandates and Powers of Enforcement

Land value capture may rely on tax or other regulatory functions to define and enforce LVC principles. If a government’s fiscal mandate is not clear or where fiscal obligations cannot be or are not enforced effectively, this may undermine the LVC program. Those holding mandates to set and enforce rules around LVC also need the capacity to implement their mandates well. This may also be a question of perception; investors need to have the confidence that the tax and other regulatory functions will be implemented.

2.3.11 Need for Accurate and Complete Data

An inventory of land assets owned by government agencies can identify current land use and determine its market value. Access to such a pool of data, to the extent it is complete and accurate, improves government’s ability to obtain best price and identify issues/challenges in advance to address them when they arise and to improve the value of the property to the market. The government can then decide which land parcels would be more beneficial to urban development if sold, determine the kind of additional services or investments that purchasers should be required to deliver, and identify the potential purchasers of such land to allow the government to prepare and get maximum value from it. This exercise often leads governments to discover they own far more undeveloped land than they had realized.

2.3.12 Risk of Overreliance

Overreliance on LVC exposes projects to excessive market risk. While a robust real estate market and rising land prices are good for LVC, projects should estimate the revenue to be generated from LVC schemes based on cautious and realistic assumptions, given the unpredictability of the real estate market. Governments should prepare contingency plans in case revenues are lower than projected.

2.3.13 Managing Corruption and Perceptions Thereof

In general, in many developing countries, the public has a negative perception of government disposal of land, the assumption being that the buyers will be the elites and those with connections. To secure public support, government should implement transparency in decision processes, monitoring, and evaluation. It should raise public awareness of the chosen scheme and its objectives, principles, rules, and regulations. It is also important for governments to involve civil society organizations in planning and project development activities. Probably the most important way to prevent potential corruption is to require transactions to follow market pricing, based on an independent assessment. Transparent information systems will also help prepare future LVC schemes, by making the relevant market data available.

2.3.14 Avoiding Excessive Gentrification

Property developers under LVC schemes often displace low-income households by increasing property values and pricing out low-income communities. LVC should not just create economically efficient and environmentally friendly urban spaces, it should also address urban poverty and deprivation. Where possible, government should pursue affordable housing and provide developers with incentives to ensure that affordable housing is built close to transit stops. A density bonus for constructing social housing can be included in LVC agreements.