INTRODUCTION

Across Africa, the size structure of farms is changing, with an increasing proportion of medium-scale farms (Jayne et al. Reference Jayne, Chamberlin, Traub, Sitko, Muyanga, Yeboah, Anseeuw, Chapoto, Wineman and Nkonde2016). This is having profound implications for the patterns of agrarian accumulation and the possibilities of commercialisation. In Ghana and Zambia, for example, medium-scale farms now account for more land area than small-scale farms, defined as cultivating under five hectares (Sitko & Chamberlin Reference Sitko and Chamberlin2015; Jayne et al. Reference Jayne, Chamberlin, Traub, Sitko, Muyanga, Yeboah, Anseeuw, Chapoto, Wineman and Nkonde2016).

Land concentration in medium-scale farms, under new ownership and land tenure arrangements, occurs through different routes – either through accumulation of land by those who earlier had smaller plots via local land markets, or acquisition of land by ‘outsiders’ through political and other connections. In Zimbabwe, the emergence of a medium-scale farm sector is linked to land reform after 2000, which created around 23,000 additional medium-scale farms (ranging in size from c. 10 ha to over a thousand hectares, averaging 153 ha). These land reform resettlement farms (denoted A2) account for 3.5 million hectares, nearly 9% of the area of all agricultural landholdings (Moyo Reference Moyo2011: 498).

This paper explores the origins and implications of these medium-scale farms in Zimbabwe, asking how they fit into the post-land reform agrarian structure, who the owners are, what they produce and sell and how they are differentiated. As a now major, but poorly understood, part of the agricultural economy, the aim is evaluate the A2 farm experience against the wider story of the rise of medium-scale farms in Africa more broadly, examining in particular the processes of differentiation among such farms, and so the diverse trajectories of change observed.

Farm size distributions in agrarian economies matter, as they influence overall patterns of inequality, the opportunities for accumulation and the potential linkage effects between farm sectors in regional economies (Sitko & Jayne Reference Sitko and Jayne2012). Agrarian structure also often reflects rural political settlements, with different agrarian classes linked to farms of different sizes (Moyo Reference Moyo2011; Scoones Reference Scoones2015). In former settler economies, land reforms have been focused on overturning a highly unequal land distribution, creating new opportunities for both smallholders and ‘emergent’ commercial farmers.

In Zimbabwe, land reform was aimed at transforming the former dualistic structure, creating a ‘tri-modal’ structure (Moyo & Chambati Reference Moyo and Chambati2013). This involves small-scale farms, including communal areas, as well as old and new (A1) resettlement areas (total 1.3 million farms, over 25.8 million ha), medium-scale farms (A2 farms, plus older small-scale commercial farming areas, total 31,200 farms, over 4.4 million ha) and large commercial farms and estates (total 1,618 farms, over 2.6 million ha) (Moyo Reference Moyo2011: 512).Footnote 1

Medium-scale farms are crucial in this new agrarian structure. They are neither small-scale, often subsistence-oriented peasant farms, nor are they large-scale, highly capitalised farms and estates, sometimes owned by multinational capital. Previously, black-owned, medium-scale farms were created as ‘Purchase Areas’ from the 1930s (Cheater Reference Cheater1984), but the extent was limited. Today, medium-scale farms in Zimbabwe, as defined by the A2 ‘model’, are mostly sufficiently large that they offer the opportunities for commercialised agriculture, involving mechanisation, the employment of a permanent workforce, the use of high levels of ‘modern’ inputs and the generation of substantial market offtake. All this requires capitalisation and regular flows of finance, as well as considerable skill in both production and marketing. Of intermediate scale, embedded in regions where smallholder farming dominates, they take on a new role in regional economies, potentially offering support for equipment sharing, labour employment and market assistance.

This is the theory at least and was the driving inspiration behind Zimbabwe's resettlement planning from the 1990s. This paper explores the practice, nearly 20 years after the land reform of 2000, asking whether such medium-scale farms offer a vision of the future of commercial agriculture, as some claim based on studies elsewhere in Africa, or whether in fact there are more diverse trajectories of change emerging, with some succeeding, while others struggle.

STUDY AREA AND METHODS

This study was undertaken in Mvurwi, a high-potential area to the north of Harare, and Gutu and Masvingo districts in Masvingo province, in the drier south-east of the country. The study focused exclusively on those farms designated as A2 during the ‘fast-track’ land reform programme. The study therefore does not adopt the size classifications used in other recent studies of medium-scale farms, which rather arbitrarily designate medium-scale to be any farm above five hectares and below 100 hectares (e.g. Jayne et al. Reference Jayne, Chamberlin, Traub, Sitko, Muyanga, Yeboah, Anseeuw, Chapoto, Wineman and Nkonde2016).Footnote 2 Nor does it include farms that are medium-scale operations, such as those designated as self-contained A1 (smallholder) farms or former ‘Purchase Areas’ (Scoones et al. Reference Scoones, Mavedzenge and Murimbarimba2018a).

In each of the study regions, a full list of A2 farms was compiled. This had to rely on a variety of sources, given the sensitivity of the data. A government audit of all A2 farms undertaken in 2006 was also used, along with data held by the then ministries of land and agriculture. We also cross-checked these listings with farmers, extension officers and government officials in the field. There has been a large turnover in A2 areas, with take-overs, inheritances and subdivisions affecting farm owner listings, making establishing a sampling frame especially challenging.

From these comprehensive listings, we collected basic census data for all farms, including date of settlement, farm size, main farm activities and former/current non-farm occupations.Footnote 3 The listings were then used to draw a random sample in each site. In the end, the sample was 39 farms in Mvurwi (19% of A2 farms in the area), reduced because of drop-outs, and 51 across the Masvingo-Gutu sites (21% of farms). Our sample was broadly representative of the wider population, in terms of land area, focal activities and occupations of the farm owners, as indicated by an analysis of census results. A random sample, however, presented problems for data collection given the dispersed geography of the farms and the frequent absence of farm owners, and the survey took a long time to implement. A short questionnaire survey,Footnote 4 combined with in-depth interviews with owners/managers/workers, was conducted with all sampled cases. In both sites, the sample overlapped with earlier surveys undertaken in 2006–07, allowing some limited analysis across time.Footnote 5

A preliminary stratification into three categories was generated, based on the survey data. Sample households were ranked according to the average of maize and tobacco (for Mvurwi only) output for the 2016–18 seasons, as well as cattle ownership in 2017. These variables were chosen following discussions with farmers, who confirmed that these were the most significant factors that differentiated farms. A composite ranking was created and then the full listing was divided into three, as there were no obvious breaks in the data distributions. While a simple division into three equal groups means that the distinctions between the bottom of one group and the top of the next are not significant, the overall categorisation correlated well with a range of other variables (relating to income, marketing, asset ownership and other indicators of agricultural commercialisation; see Tables I–IV), even though the distribution of values overlap, as indicated by often wide ranges. The broad correlation between indicators gave us confidence in this initial categorisation, and so the stratification of the survey data. However, to gain a deeper insight into processes of differentiation and accumulation, the farmer categorisation and the associated survey results must be taken together with the other more qualitative data from particular cases, which were collected through interviews in each site.

Table I Profiles of A2 farmers

Table II Previous/current occupations of farm owners

Table III Asset ownership patterns (average, with standard deviations in parentheses)

Table IV Patterns of production and farm employment (average, with standard deviations in parentheses)

As we discuss below, while there are broad trends and tendencies highlighted by the three farmer categories, there are other cases that are outliers. For example, some who engage in particular ‘projects’, may generate significant income, say from broiler production, but may not be ranked highly in relation to crop income and cattle ownership. The advantage of a small sample size of course is that we know each of the cases well, and the story that emerges below – including the identification of ‘projects’, such as broiler production, as a key commercialisation strategy – derives from a triangulation of insights, with the three categories only being a useful starting point. To complement the survey and case study interviews, we therefore conducted 20 more detailed follow-up interviews with farmers and farmworkers selected purposively in both sites and across the three categories, focusing on farm and household biographies, and so changes over time.

In addition to our core sample, we also undertook seven studies of joint-venture A2 farms in Mvurwi; these included farms operated both by Chinese companies and those managed by displaced white farmers. As discussed later, a simple classification of ‘commercial’, ‘aspiring’ and ‘struggling’ farmers emerged through an interpretation of the data. While broadly centred on the three categories derived from our survey data, the classification takes into account other factors. It focuses less on the static patterns of agricultural output and asset ownership, but more on the dynamics of change, linked to ongoing processes of social differentiation, accumulation and class formation, in turn offering insights on the emergent politics in Zimbabwe's post-land reform countryside as influenced by medium-scale A2 farms.

A NEW AGRARIAN STRUCTURE: WHO ARE THE MEDIUM-SCALE FARMERS?

The A2 model was proposed as part of the 1998 land policy, with land allocated mostly during 2001–2, as part of the ‘fast-track’ land reform programme. The new farm structure reflected a commitment to supporting commercial agriculture outside remaining large-scale farms and estates. Allocations of medium-scale farms represented a political class compromise by the party-state to help satisfy land demands from the middle class (mostly professionals, including many civil servants) and party-military-business elites (members of the security forces, as well as business-people and ruling party officials). While land demands of mostly poorer people involved in land invasions were met under the A1 scheme, the A2 resettlement areas targeted a different group (Moyo & Chambati Reference Moyo and Chambati2013).

One frequently heard narrative about land reform in Zimbabwe is that it was captured by ‘cronies’, with allegedly over half the land taken by ZANU-PF officials.Footnote 6 However, such claims are disputed, as research shows how the A1 smallholder resettlement areas were largely occupied by landless/land-poor peasants from nearby communal areas and un/underemployed people from urban areas (Moyo et al. Reference Moyo, Chambati, Murisa, Mujeyi, Dangwa and Nyoni2009; Scoones et al. Reference Scoones, Marongwe, Mavedzenge, Mahenehene, Murimbarimba and Sukume2010; Matondi Reference Matondi2012). Within the A2 medium-scale farm areas, there is a mixed population, which includes well-connected elites, but nowhere near to the extent claimed.

Officially, applicants for A2 farms had to present a business plan and show they had the necessary experience and sufficient capital before allocation. However, political factors did intervene and this technocratic allocation process could be overridden through influence on provincial and district land committees (Marongwe Reference Marongwe2011). Subsequent to initial allocations, rearrangements were sometimes forced, particularly around election times, with this rising to a peak before the contested elections of 2008, when political favours were granted and scores settled. Those with significant influence – notably government ministers and high-ranking military officers – were also able to break the land-ceiling regulations and the ban on multiple holdings. However, as our data show, these instances were rare. War veterans were notionally given preferential access, with 20% of farms supposedly reserved for them (Matondi Reference Matondi2012: 64). However, most only managed to gain access to A1 farms, as they helped lead invasions, and it was usually only war veteran association leaders and officials who were allocated A2 plots.

The result is a diverse population on the A2 farms, as we explore below. How does this match up to the pattern seen elsewhere in Africa? Studies from Ghana, Kenya, Nigeria, Malawi, Tanzania and Zambia (Sitko & Chamberlin Reference Sitko and Chamberlin2015; Anseeuw et al. Reference Anseeuw, Jayne, Kachule and Kotsopoulos2016; Jayne et al. Reference Jayne, Chamberlin, Traub, Sitko, Muyanga, Yeboah, Anseeuw, Chapoto, Wineman and Nkonde2016; Hall et al. Reference Hall, Scoones and Tsikata2017; Muyanga et al. Reference Muyanga, Aromolaran, Jayne, Liverpool-Tasie, Awokuse and Adelaja2019), for example, show that medium-scale farms emerge both through land consolidation in an area, as locals buy out smaller farmers, and through the purchase of blocks of land from outside. This is sometimes combined with state-directed redistribution, and assistance with settlement. Those occupying such farms include both active and retired civil servants, investing salaries and pensions in farms; businesspeople, with urban enterprises, but a desire to extend commercial activities to agriculture; as well as councillors, chiefs, politicians and others with connections. Patronage politics and processes of ‘accumulation from above’ are common (Mamdani Reference Mamdani1987), and such farms represent the fast-changing political and commercial interests in agriculture across Africa (Morris et al. Reference Morris, Binswanger-Mkhize and Byerlee2009).

How does this compare with A2 medium-scale farms in Zimbabwe? Table I offers profiles of the farmers in our sample, comparing the two sites. It shows that household heads are mostly men and relatively old, more so in Mvurwi where the average age was around 60. The younger average age of the farm owners in Masvingo-Gutu reflects a process of inheritance since settlement, as many original occupants have died and farms have been passed on to sons and wives, indicated by the higher proportions of female-head owners. Most farm owners had completed secondary education, and over half in Mvurwi had completed an agricultural qualification (concentrated in category 1 households), including ‘Master Farmer’ certificates and agricultural diplomas, especially among those previously working as extension agents. Some had university degrees, even one MSc in agricultural economics. Others also had specific tobacco-related qualifications, gained at the nearby Blackfordby College. The lower level of agricultural qualification in Masvingo-Gutu reflects the turnover in household heads, as sons and wives of the original owners had not pursued such courses, even if the original owner had gained access to the land on the back of such qualifications.

The patterns of residence are quite different. In Mvurwi, over two-thirds of household heads were based on the farm (all of those in category 2), even though nearly three-quarters also had houses in town (usually Harare, 100 km away), especially those in category 1. This relates to the intensity of production (often of tobacco) and the need for regular, on-site supervision. This pattern has changed since 2000, as farmers have retired from jobs, and moved to engage in farming. Many realised that ‘cell-phone’ farming does not necessarily deliver. In Masvingo-Gutu, by contrast, only a third are based on their farms full-time, although this rises to just over a half among category 1 farmers. Partly this is due to the lack of infrastructure in many of the Masvingo-Gutu farming areas, making it difficult to settle for families used to the relative of comforts of town life. It also relates to the nature of production in low-potential agro-ecological regions, with many operating extensive cattle ranches, which require less supervision and so the possibilities of managing the farm through weekend visits.

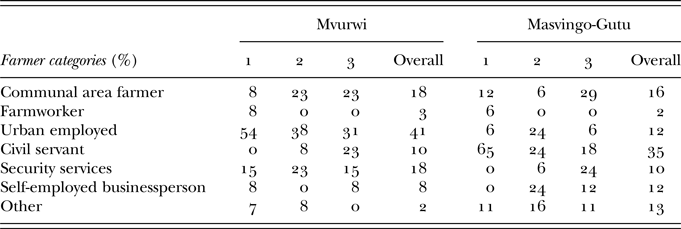

Table II indicates the previous/current occupations of A2 farmers across the sites. The narrative that these farms were captured by ‘cronies’ is not supported. That said, those in the ‘security services’ category, including those employed by the police, army and Central Intelligence Organisation, were often able to manipulate the application process and gain access to land. Those with jobs, current or past, in the security services were more common in Mvurwi (18% compared with 10%), which is closer to Harare and has more desirable land. Civil servants were especially common in Masvingo-Gutu, concentrated in category 1, and included many teachers/headmasters, health professionals, agricultural extension officers, veterinarians and others, including those working in local government. Some of these individuals were able to manipulate the system too, especially if they also had a political position, but many simply applied and met the criteria.

Those defined as urban employed were the dominant category in Mvurwi, again especially concentrated in category 1, and included those cutting across a range of jobs outside the civil service. This again reflects the proximity of the site to Harare, where those jobs are more common. Most had applied through the formal routes, demonstrating a business plan and a level of capital available. Jobs included those in private sector companies, NGOs, charities and churches. Again, some were able to influence allocations through political connections, but this was very much the minority. Those defined as self-employed business people were present in both sites, and include those working locally, frequently in nearby towns, often in transport firms, restaurants/bars and retail shops. In addition, there were a few former farmworkers in both sites, who, having been displaced from farms by the land invasions in 2000, applied for land; perhaps surprisingly all within category 1, possibly reflecting their high skills at farming and so higher output.

Finally, there were politicians. There were no serving politicians in our random samples, but there were cases within the whole population, including several retired ministers, one now late Vice-President and some MPs, current and past, as well as a few with political posts in the ruling party. All these, we suspect, gained land outside the formal application procedure. Political favours do not necessarily last, however, and there were several cases where high-ranking figures were removed in both sites. Data on political party affiliation cannot be collected because of sensitivities, but most resettlement areas, as with the rural areas of the country in general, have consistently voted for ZANU-PF. That said, there are plenty of opposition supporters in these areas too, who will ‘perform’ being ruling party members to avoid retribution (Mkodzongi Reference Mkodzongi2013).

Across these groups, 31% and 18% identified as war veterans in Mvurwi and Masvingo-Gutu respectively. This category is a flexible one, and includes many who were war collaborators, rather than liberation war fighters. However, the data show the continuing influence of the ‘war veteran’ identity in political processes in Zimbabwe. War veterans appear across all occupation groups, except for farmworkers. Since demobilisation after Independence, they have taken up diverse jobs, many returning to farming in their original communal areas.

In sum, the A2 farms are populated by a hugely diverse group of people, with different identities, occupations and affiliations. While certainly existing, so-called cronyism does not dominate, and the population is the result of a combination of allocation processes: some formal and technocratic, others based on political position and patronage. As already discussed, the overall composition is actually very similar to that recorded in the other studies of medium-scale farms elsewhere in Africa.

In class terms, we observe an influential, but numerically relatively small, group of business-political-military elites, combined with a much larger professional middle class (often former and current civil servants), together with urban-based, well-networked business people, and some former peasant farmers from communal areas and a few former farmworkers. People's identities are complicated by political affiliations, historical associations with the liberation war and also regional and local alliances, including with influential churches. For example, in the wider census in Masvingo-Gutu, there were five farmers who were officials of the ruling party-aligned Apostolic Faith Mission church, including a bishop and several pastors.

However, to understand the class dynamics emerging in the A2 areas, we cannot rely on these simple assignations of occupation or affiliation; indeed, class formation and emerging relations are highly dynamic, and have changed significantly over the last 20 years. Therefore, in the next sections, we focus on processes of accumulation and differentiation across farms, and ask the key questions of critical agrarian studies, following Bernstein (Reference Bernstein2010): who owns what, who does what, who gets what and what do they do with it?

SETTLEMENT AND BUILDING ASSETS FOR AGRICULTURE

Most farmers in our sample got allocated land in 2002. The A2 allocations followed on from the land invasions, which subsequently became A1 resettlement schemes. The sub-division of large farms into A2 plots involved more planning, as attempts were made to distribute land and farm assets in ways that a single operational farm could emerge. There were disputes over who got what, with some rejecting their allocations, while others contested allocations of farmhouses and other desirable assets. In Mvurwi area, the issue of control over and responsibility for farm labour compounds was contentious, with some welcoming access to labour from a nearby compound, often housing several hundred former farm worker families, while others mentioned in interviews that the presence of such populations was a liability, blaming them for thefts, disruption and refusing to work. It was a turbulent period, and initially little farming was carried out.

Even when disputes cooled off and new patterns of labour hiring and control were negotiated, establishing a farm required considerable investment of time, money and skill. With land audits always on the horizon, assuring occupancy and some level of activity was always important. This sometimes meant the placing of a few workers or relatives to hold the farm, while resources were mobilised. For those who gained farms with previously cultivated land, it was possible to move into production relatively quickly; for others it was more challenging. For tobacco, Chinese finance through contracting arrangements was essential (Mukwereza Reference Mukwereza2015). For those establishing livestock operations, acquiring or moving stock was the first step, often starting with small herds and flocks.

The studies in these sites from the mid-2000s showed that, with a few exceptions, the A2 farms were performing extremely poorly, with extensive under-utilisation of land and limited production (Moyo et al. Reference Moyo, Chambati, Murisa, Mujeyi, Dangwa and Nyoni2009; Scoones et al. Reference Scoones, Marongwe, Mavedzenge, Mahenehene, Murimbarimba and Sukume2010; Matondi Reference Matondi2012). Unlike for the smallholder A1 settlements, getting started without capital and with limited external support was challenging. While there were various schemes, initiated through the Reserve Bank of Zimbabwe, these were ad hoc and notoriously corrupt, making accessing equipment, cattle or finance difficult for many (Shonhe Reference Shonhe2018). From around 2006 inflation accelerated, rising to a peak in 2008, after which the economy was dollarised. The hyperinflationary period disrupted investment plans and, while some were able to exploit the parallel currency arrangements through black market deals, most suffered through losses of money value. Production, which by then was beginning to get going, collapsed. It was only during the period from 2009, coinciding with the Government of National Unity and a period of relative stability, that things picked up again. This period was when some people were able to accumulate and the pattern of differentiation seen today emerged. With inflation rising and an economic crisis engulfing the country once again from 2018, the threats to investment in the A2 farms are high, potentially undermining the gains made.

What is the pattern of asset ownership seen across the three farmer categories identified from the survey data according to ranked crop output and cattle ownership? Table III offers a snapshot from 2018–19, showing clear trends across the categories, but also large variations within. Land holdings are lower in high-potential Mvurwi than lower-potential Masvingo-Gutu, but vary significantly. There is high variation in land utilisation, where only those in the top category are cropping significant areas. Tractor ownership is surprisingly low given the areas cropped by the top farmer categories, but there is a vibrant rental market in the A2 areas. Cattle holdings are unsurprisingly much higher in Masvingo-Gutu, but those in the bottom category have very few on average. The same applies to categories 2 and 3 in Mvurwi, and it is only those in the top group who have a commercial herd (above 10). Goats are not common in any site, and relatively few are kept as a household flock. In terms of other equipment, at least one car or truck is owned by 51% of households in Mvurwi and by 57% of households in Masvingo-Gutu. The long distances to town and the lack of any other transport make having vehicles crucial, and many category 1 farmers have invested in small five-tonne trucks. With electricity being so unreliable, many have also bought generators, which power homes as well as small-scale irrigation operations.

PATTERNS OF PRODUCTION AND EMPLOYMENT

How does asset ownership translate into agricultural production and income? As Table IV shows, the difference between the top category and the others is stark. With some exceptions, it is mostly those in category 1 who have the resources and external finance to crop significant areas, although the ranges of production/sales levels are large. The top farmer category is the only group who employ significant numbers of permanent employees (at least in Mvurwi to run tobacco operations), and they are most likely to employ a farm manager to oversee the farm. They also have the greatest number of pig and broiler projects, although these are relatively few in number. Horticultural production is again most common among category 1 farmers, although most are trying some at varying scales. Irrigation facilities are unevenly distributed, and it is category 2 that has the highest proportion in both sites. Access to irrigation partly depends on inherited installations; although, as time has passed, many farmers, especially in Mvurwi, have invested in boreholes, pumps, pipes and generators.

The pattern of differentiation observed reflects a divergence in strategies amongst A2 farmers. Those who are able to raise finance from different sources are able to invest and make profits from maize and tobacco production. Production among the more commercially oriented farmers is increasingly mechanised. For example, land preparation in 2017 was by tractors in 34% of farms in Masvingo-Gutu and 79% in Mvurwi, much of it through rental/borrowing arrangements. From small beginnings, Mrs M explains how she is slowly building a commercial operation:

When we came here there was nothing. Just tall grass. We had to build houses, dig boreholes. My late husband was a farm manager. He wanted to farm. We came with two head of cattle, one plough and the clothes we were wearing. We had two young kids at that time. It was tough. The first year we grew only maize and beans on a small plot. Today we plough seven hectares (of a total farm size of 27 ha), and have ten cattle. I don't have a tractor, but hire, and also use my own oxen. This last year I harvested four tonnes of maize from three hectares, retaining several tonnes to feed the family and pay labour. I also planted 0.75 ha of sweet potatoes, selling 500 buckets, together with groundnuts (80 buckets) and Bambara nuts (40 buckets) at the roadside. My son is now 24 years old and is married. He works together with me, but also brings in money from a taxi service he runs using a car we bought from our farming. I rent out three hectares and get paid in fertiliser. I also sell gum poles from the plantation to pay for labour from the nearby compound. I want to expand further, especially in horticulture if I can get another borehole.Footnote 7

Alternative strategies involve intensification of production through investment in irrigation for commercial horticulture. With markets locally, as well as through contracts with supermarkets, hospitals and boarding schools, this is an option favoured by many, as it is easier and less risky than crop production. However, as many noted, there are today multiple challenges arising from the variable supply of fuel or electricity for generators and pumps, and this is hitting aspiring horticultural farmers hard. Mr M from Gutu explained:

I am a retired teacher and got the farm in 2003 through an application. I only started farming in 2006, and initially focused on maize. The maximum we got was 23 tonnes. This year it was little because of drought. We do not live on the farm, but it's near and go most days. These days, I am concentrating on pig farming and horticulture. I irrigate one hectare of vegetables. I get orders from hotels, restaurants and shops from as far as Kwekwe and Harare. One of my sons works in a hotel and purchases vegetables, and also invests in the garden project.Footnote 8

Projects, including pig farming, aquaculture and broiler production, require limited land areas, but significant funds. Across our cases, there were multiple cases, usually involving investment from sons and daughters of farm owners through remittances, very often from the diaspora.

Levels and styles of employment also differentiate sites and categories of farmers. In Mvurwi, labour compounds provide a ready pool of labour, which can be hired on a piecework basis, via intermediaries. Temporary hiring is common in Mvurwi among all categories of farmer, where 67% of male temporary workers and 74% of female temporary workers are recruited from the compounds. However, those living in the compounds, in order to survive, are also diversifying their livelihoods, and many have acquired small plots of land, and so have partially withdrawn from the labour market (Scoones et al. Reference Scoones, Mavedzenge, Murimbarimba and Sukume2019), making labour recruitment more challenging.

Some, however, prefer to hire permanent labour. The highest level of permanent employment was 13 in Masvingo-Gutu and 100 in Mvurwi, while maximum temporary employment was 40 and 110 respectively. Those with skilled farm managers, and with a well-remunerated labour force, are profiting, but some offer poor, exploitative conditions and labour unrest is common. Most however have a hybrid arrangement, with a few permanent employees, often guards and housemaids, and rely on temporary employment for agricultural labour, hired on a seasonal basis. Mr C explained:

There is a large compound near our farm. In the beginning, I hired some of the workers of the former farmer, and in those days we produced a lot of tobacco. Up to 30 tonnes. This allowed me to buy tractors, cars, motorbikes and cattle. But later I failed to keep up with salary payments. It was a tough time when inflation hit. I now hire temporary workers from the compound. They are often unreliable though. Last season I produced 45 tonnes of maize, and I have 600 broilers and 300 indigenous chickens. It's difficult farming here. The workers from the compound frequently steal from the farm. The transformer was stolen, and we now cannot irrigate the citrus.Footnote 9

Wage employment is much less common in Masvingo-Gutu given the different pattern of extensive livestock production. Here, with farm owners often absent, there are farm managers, guards and herders employed, and often a different trajectory of accumulation centred on cattle production.

FINANCING AGRICULTURE

Access to finance is perhaps the key factor affecting commercial agriculture on the A2 farms. As discussed already, economic conditions since 2000 have not been favourable, especially between 2006 and 2009 and again since 2018. Lack of financing for agriculture contrasts with the situation before Independence, when large-scale commercial farming was heavily subsidised and received generous soft finance through seasonal and medium-term bank loans. This was essential for both the establishment of white commercial agriculture at the beginning of the twentieth century and for its sustenance thereafter (Dunlop Reference Dunlop1971; Palmer Reference Palmer1977). While state subsidies were progressively withdrawn after Independence, there were effective subsidies operating through preferential trade deals and continued generous financing from commercial banks. This has not been available to the A2 farmers over the last 20 years.

In the absence of this level of support, how have A2 farmers fared? Table V offers an overview of the different financing options observed in 2018–19. Many farmers make use of a variety of options. With the exception of category 1 farmers in Mvurwi, bank loans and credit were accessed by under a third of farmers. This contrasts very unfavourably with the previous era. This relates in part to the liquidity crisis in the country and the preference of banks to loan outside the agricultural sector. It also links to the collateral requirements of banks. While all farmers in our sample had ‘offer letters’ from the state, only four had leases; and even those with leases have been refused credit because of ongoing disputes around the lease terms. Without having their land to offer as collateral, some have mortgaged houses or business properties in town, but this is not available to everyone.

Table V Financing options

Instead, many in Mvurwi have gone into contract arrangements for the production of tobacco with private companies. This is most common among category 2 farmers, who do not have the independent resources of category 1 farmers, but can afford the risk of a contract arrangement unlike category 3 farmers (Scoones et al. Reference Scoones, Mavedzenge, Murimbarimba and Sukume2018b). Sixteen tobacco contracting companies were operating in Mvruwi area in 2017, offering seed/seedlings, fertiliser and fuel, as well as technical support and guaranteed markets. Many of those with their own resources prefer to farm independently than sell through contract arrangements, as they get a better price on the merchant auction floors. However, as a way of securing stable financing and a route to accumulation, contracting tobacco production is important for others.

Command agriculture is a government-financing scheme, supported by the military and the current president. It offers subsidised inputs, including seed and fertiliser, and is focused on maize production in A2 farms in the higher potential areas, particularly those with irrigation (Mazwi et al. Reference Mazwi, Chemura, Mudimu and Chambati2019). Access to the scheme, at least to timely provision of the full package of inputs, is often reliant on having the right patronage networks. Nevertheless, this has been an important source of financing for some in Mvurwi in particular.

Some, however, can go it alone, or at least combine independent resources with institutionally derived financing. Remittances, from both local sources and the diaspora, are especially important. In both sites, but particularly in Masvingo-Gutu, A2 farmers also have businesses that help finance agriculture, including shops, bars, transport businesses and house rentals. Investment in shops and transport is essential in areas in the land reform areas where formerly there was no transport or market infrastructure. Over the last decade, particularly in the period when the economy stabilised, farmers have invested farm profits in real estate, often in booming small towns such as Mvurwi, so generating rental income (Scoones & Murimbarimba Reference Scoones and Murimbarimba2020). For many, though, self-financing of agriculture from agricultural production surpluses is the most common route. Profits from one crop can be invested in the next, and particularly the paying of labour and the purchase of fertiliser. Others choose to sell some cattle to finance the purchase of inputs and payment of labour, while others rely on maize to pay labour. Those growing tobacco may choose to make arrangements with workers for payment at the end of the season or to pay through allocation of pieces of land or bales of tobacco. This is a slow route to accumulation and holding onto cash across a season in the absence of an effective banking system, and with periods of high/hyperinflation, is challenging.

Finally, there are those who prefer to let others finance and run the farm. We undertook a focused study of the seven joint-venture arrangements in Mvurwi to complement the randomly sampled survey. Joint ventures involve foreign or local private investors who invest in A2 farmers jointly with the land beneficiary or sub-lease whole or sections of the farms and share profits annually after the marketing of farm produce. These joint ventures arise either through choice, recognising that they have neither the resources nor skills to run the farm, or out of necessity, as banks reclaim the farm due to outstanding loan repayments. In Mvurwi, there are several former white farmers who sub-lease farm sections, while Chinese investors in tobacco are operating four farms as joint ventures. These involve significant external investment in building infrastructure and covering operating costs. For instance, a Chinese firm from Szechuan has leased a farm with 146 ha of arable land north of Mvurwi. An annual lease payment is made of a fixed amount over a 20-year period, and the owner has no role in the operation. One of the Chinese managers explained:

All but 20 ha is under pivot irrigation. We grow tobacco intensively. We have invested in a new ‘rocket barn’, and sell to different companies, depending on the type of tobacco. We have bought all new equipment – generators, irrigation, tractors, pivots. Perhaps a million US dollars. We suffered a major hailstorm last season, but still managed 3.15 tonnes per hectare. We also have a cattle-fattening project, but it's just getting going. Yes, we manage a compound here, and employ around 100, mostly on a temporary basis. It's difficult to do business in Zimbabwe – we have a consultant who used to be in the tobacco business, who helps us, but it's a challenge here.Footnote 10

In sum, A2 farmers, and their joint-venture counterparts, have found it difficult to finance farming since land reform. They use a variety of routes, but all have their downsides. The problems become exacerbated with the fragility of the macro-economy, notably the lack of liquidity, the intransigence of the banking sector to use leases/permits as collateral, the shortages of physical cash, the wildly fluctuating parallel currency rates and the bouts of high inflation. The controlled and changing tobacco pricing structure where farmers are paid only 50% in US dollars, with the balance being paid in local currency using the official exchange rate, also lowers their earnings. Our data show how different people navigate such complexity and so gain access to finance. Mr M from Mvurwi explained the challenges he has faced:

I started the farm when I was still in my (agricultural extension) job, but I couldn't farm and work at the same time, so committed to farming. We harvested lots of maize – several hundred tonnes per year! Then inflation hit, and we suffered. I had to sell my cars, and 30 cattle, which I had accumulated from farming. Since dollarisation things improved, but I have not been able to get finance from the banks. I haven't got access to command agriculture. In my view it's designed for looting! I cannot finance 30 hectares from my own pocket. This year, we planted only one hectare of maize, and concentrated on sugar beans (sold on contract to boarding schools) and sweet potatoes (bought by traders from Mbare in Harare). Next year, I will scale down and look for joint ventures or sub-letting arrangements.Footnote 11

Access to finance therefore substantially underpins the variations in outcomes in terms of production, agricultural investment and household accumulation from agriculture. Those in category 3 are unable to move beyond effectively subsistence production; those in category 2 aspire to step up to more independent commercial production and often make use of contract farming to do so; but it is only those in category 1 who really offer an example of ‘successful’ medium-scale farming, although many struggle too.

PATTERNS OF DIFFERENTIATION AND ACCUMULATION

Locating our understanding of medium-scale farms in a relational and dynamic understanding of agrarian change is essential. We have asked ‘who owns what?’, through an assessment of assets owned, and have explored ‘who does what?’ in terms of differentiated livelihoods. The key remaining questions now are ‘who gets what?’ and ‘what do they do with it?’, requiring an exploration of how patterns of accumulation result in differentiated livelihood pathways.

In particular, we must ask how on-farm and own-business profits are translated into farm-based ‘accumulation from below’ (Neocosmos Reference Neocosmos1993), whereby a positive cycle of investment and asset building results in the growth of farm income and employment (Cousins Reference Cousins, Hebinck and Shackleton2010). An exploration of the opposite trend is also important. If on-farm or business profits are limited, through lack of finance, scarcity of labour, limited assets and lack of markets, then how do people construct their livelihoods? For example, how is social reproduction squeezed due to the deployment of family labour, particularly that of women and children? What alternative income-earning options are sought? What relations of labour emerge, as people engage in employment, including with richer farmers, to survive? And cutting through all these processes, what is the role of the state – and networks of patronage associated with the party-state – in supporting some trajectories of accumulation, while preventing others?

In the analysis above we have contrasted three categories of farmer, derived through a ranked ordering of indicators of crop output and cattle asset holding. As we have shown, these in turn relate to a range of other variables that influence how people make a living. While recognising that there are large ranges, overlaps between categories, significant outliers and particular cases, how can we make sense of the emerging differentiation in A2 farms? Mapping broadly, but not exclusively, onto our three farmer categories, we suggest a simple typology below, focusing now less on static outputs and assets, but more on the processes of social differentiation and accumulation. This in turn can inform our understanding of the emerging dynamics of class formation in these areas, and so rural political dynamics.

Commercial farmers

First, there are what might conventionally be designated commercial farmers. They are producing substantial quantities of agricultural outputs, selling large proportions and making profits. They are, in turn, investing on the farm, whether in farm equipment or infrastructure, as well as ploughing back funds to purchase inputs and build up assets, including livestock. They are employing others in significant numbers, including having a permanent workforce, and very often a professional farm manager. In other words, such farmers, centred broadly, although not exclusively so, on category 1 farmers described above, are ‘stepping up’ (Dorward et al. Reference Dorward, Anderson, Bernal, Vera, Rushton, Pattison and Paz2009), accumulating from farm production, even if this is co-financed.

There are two routes to accumulation for such farmers. One is ‘from below’, from own-farm production, combined with other businesses, where investment from profits moves between different enterprises in a portfolio. External finance may be important, but this involves paying loans and interest, as part of a business plan. The other route to an upward dynamic of accumulation is through involvement in patronage networks, including access to ‘command agriculture’ subsidies for around 40% of category 1 farmers. The net effect is the same – often an outwardly highly successful commercial operation, but accumulation is both ‘from above’ as well as ‘from below’. The first trajectory is the ideal-type commercial farmer: independent, hard-working, business-oriented and profitable. As we have seen, these exist but they are rare, and all are finding it difficult to run farm businesses. The other trajectory is one that is reliant on subsidies, soft loans and close connections with the state. This is of course another classic route to commercial agriculture, given the nature of farm support the world over; and indeed was the way settler agriculture was nurtured in Zimbabwe throughout the colonial era (Hanlon et al. Reference Hanlon, Manjengwa and Smart2012). Most farmers in this category show a combination of these trajectories – demonstrating effective business management and generating their own profit, but also being reliant on external support of different sorts.

The joint ventures discussed earlier do not fit easily into either of these patterns. These are certainly ‘commercial’ farms, although questions must be raised about the timeframe for generating profit streams. They are, however, less embedded in the A2 areas, and rather an external model is transplanted, with a very separate system of management and business practice, linked, in the case of the Chinese investors, to a large, sometimes global, portfolio of diverse operations. They certainly have an impact on the local agrarian economy, as they sell to the same markets, employ from the same labour pool and make use of the same natural resources, but the ‘farm owners’, while profiting from the arrangement, are set apart from those engaging directly in agriculture.

Commercial farmers, of the sort described here, are more common in Mvurwi than in Masvingo-Gutu, but breaking into this group is hard given the economic conditions constraining the first accumulation trajectory and the closed nature of political networks constraining the second.

Aspiring farmers

There are also what we call ‘aspiring farmers’; those who would like to be commercial farmers, but are constrained by lack of finance and face challenges of production and investment. These farms, centred on category 2 explored earlier, are not reaching their potential, either as tobacco/maize farms in Mvurwi or as livestock ranches in Masvingo-Gutu, and many have limited areas cultivated and large under-grazed areas. There is sporadic investment and some basic assets, such as tractors and irrigation equipment, but these may be in a state of disrepair. They are largely not employers of much permanent labour and rely on temporary employment. For many, the role of external jobs and partnership connections is less evident, and they rely more on their own, often limited, production. However, although they are ranked lower in terms of crop outputs and livestock ownership, they are aspiring to improve, and deploy a variety of strategies to do so.

Two trajectories of (constrained) accumulation are evident in this group. These include those who attract family members to come and stay on the farm, and share assets, labour and management of often quite large properties. This we call the ‘villagisation’ strategy; something seen over generations in the former ‘Purchase Areas’ (Scoones et al. Reference Scoones, Mavedzenge and Murimbarimba2018a). As Mr C explained, this is now beginning to emerge on the A2 farms, as sons establish homes and join their now ageing parents:

Four of my sons are resident here, three are married. I have two wives, each with five children. The farm is essential for our family. We have nearly 20 hectares of arable land in a 30 ha farm. Normally we cultivate the full arable area. Everyone works on their own plot, and all my sons have a tobacco grower number. I came from the communal areas in 2002, when my family was young. We had 12 cattle, one scotch cart and two ploughs. I applied through the normal route, as I had a Master Farmer certificate from Chiweshe. Today we have 40 cattle, a truck, a trailer and much other farm equipment. We had a tractor, but sold it to raise capital, and now hire. We all have contracts for tobacco, and this year sold seven tonnes (less than before, as prices are so low). Together, we also produced 26 tonnes of maize. We hire temporary labour from the compound nearby, but rely on family labour a lot. I also make money from transporting tobacco with my truck, and sell vegetables and ‘road runner’ chickens. I don't receive any external finance: everything is from the farm.Footnote 12

Another trajectory also involves other family members, but through investment in ‘projects’ from outside. Sons and daughters working elsewhere, very often abroad, invest in particular ‘projects’, whether a pig unit, broiler production, fish farming, an orchard or a focused agricultural project, such as chilli production. The relative covers the costs through remittances, while residents, often ageing parents and workers, manage the project. Mr D, a worker, highlighted the importance of such projects:

This farm is quite large (over 600 ha), but we don't do much cropping (just four ha), and there are only five cattle. We produce maize just for the home and the workers. The main business is pig production. We have several hundred in well-constructed sheds. We sell perhaps 20 per month, mostly to restaurants in nearby Masvingo. A more recent project is fish farming, and we have six ponds now constructed, and sell bream. The farm is looked after by myself and two other permanent workers, and I have been here for eight years. The owner lives in Masvingo town, and gets support from her children who are living in different countries, including the UK.Footnote 13

Both these strategies act to mobilise finance and/or labour in different ways and help such otherwise constrained but aspiring farmers to improve livelihoods, and begin to accumulate. Such aspiring farmers must rely primarily on kin relations to support production and accumulation. As they are less well-connected politically, they are not big beneficiaries of state subsidies and loans, nor do they have the connections to broker joint-venture arrangements, although, as they explain, they would certainly like both.

Across our sample, aspiring farmers are perhaps the most common group. Some are tentatively ‘stepping up’, others are ‘stepping out’ and diversifying, while others are simply ‘hanging in’. For them, economic, social and political constraints faced in Zimbabwe seriously limit potentials.

Struggling farmers

Finally, there are those whom we call struggling farmers. They are simply ‘hanging in’, if not ‘dropping out’. On these farms, broadly centred on category 3, there is frequently little happening. There are few farm assets, limited production and the farm is occupied often by an elderly person; sometimes the owner, but often a relative, perhaps together with some workers. This may be due to a mix of misfortune, age or ill-health, and this befalls both young and old farmers. Quite a few war veterans are in this group, as they came with few physical assets, relying on their political capital to gain access to land. Many are of an age when ill-health and infirmity strike, and some have abandoned the farms, returning to communal areas or seeking plots in A1 schemes, where the social fabric of a farming community is more evident. Mrs M explained:

I come from a family of war veterans. I fought in the war, and was later a school teacher. I got the farm in 2002, but came in 2007 with little – a scotch cart, a harrow and a plough. I bought cattle when here, and now there are 25. I have 22 ha arable on a 54 ha farm, but I cannot farm much. Last year I farmed a few hectares, but started too late. I slipped a disc and couldn't work. I live alone here, with a worker and survive off my pension, renting my house in Harare and help from my son. Last year he paid for tractor ploughing. He also helps with a chicken project, and I sell in Harare. Right now, he's not interested in farming, and is working in town as a lawyer for a bank. He wanted to join the ‘command’ programme, but failed. I hope he will take over, as there's now a good house and lots of potential.Footnote 14

Overall, there are struggling farmers of very different types. There are also those whose farms are not producing and are being held for the future, as part of an investment for the next generations, for retirement or as speculation. This group has a very different social profile to those who have fallen on hard times and are struggling. They are absent from the farm, leaving workers or relatives to give the impression of occupation, and may be involved in jobs or businesses in town, or even abroad. They have sufficient political connections to retain the land in the face of an audit inspection, but are not using these to leverage investment.

CONCLUSIONS

What then does this analysis mean for the future of medium-scale farms in Zimbabwe? Over nearly 20 years, a process of differentiation has emerged in the A2 areas, as it has in the A1 schemes (Scoones et al. Reference Scoones, Marongwe, Mavedzenge, Murimbarimba, Mahenehene and Sukume2012) and before in the communal areas (Cousins et al. Reference Cousins, Weiner and Amin1992). Redistributing land unleashes a set of social, economic and political processes that are complex and intertwined, and our analysis suggests a number of different trajectories of accumulation, within and between commercial, aspiring and struggling farmers.

In class terms, we can observe the emergence of a distinct group of capitalist farmers, perhaps a new rural bourgeoisie, amongst the commercial farmer group, but linked to quite different underlying drivers. Not all in this group are so-called ‘cronies’, connected to and dependent on the party-state. Some have made links with external, global and agribusiness capital to develop partnerships, while others are accumulating ‘from below’. Aspiring farmers contain a significant proportion of what we might call ‘petty commodity producers’, combining family-based production with forms of capitalist production. All aspire to become successful rural capitalists, although many cannot. The final group includes those who, because of hard times, are operating essentially as peasant producers, but on often very large land areas. Some have moved into combining limited agricultural production, with selling labour, merging with the fragmented ‘classes of labour’ (Bernstein Reference Bernstein2006), common amongst both landholders and former farm workers across the communal and smallholder resettlement areas (Scoones et al. Reference Scoones, Mavedzenge, Murimbarimba and Sukume2019). Those whose farms are struggling, but are just holding the land for speculation, may occupy a variety of class positions, from salaried workers to urban-based capitalists to the political-military elite.

The A2 areas are therefore a complex socio-political mix. The analyses of medium-scale farms in Africa that have dominated the literature to date focus only on size and operated area distributions, together with a limited assessment of the profiles of farmers. These assessments tell us neither about the social and political importance of such farms in the wider agrarian setting, nor about the longer-term consequences of differential accumulation on rural class formation. Only with a more detailed delving into social, political and economic relations, as has been attempted here, can we get a sense of what these farms mean in terms of the wider agrarian political economy. This study suggests therefore a new avenue for Africa-wide research, going beyond simply describing changes in farm size structure to understanding the underlying dynamics of on-going agrarian change. For Zimbabwe, our analysis suggests a rejection of the simplistic assessments that claim the overwhelming dominance of ‘cronies’ or the writing-off of such areas as wholly unproductive and under-utilised. As our disaggregated analysis shows, there is much more going on both within and across areas, reflected in very different patterns of accumulation. While the assumption that the A2 farms would uniformly unleash a new form of commercial agriculture in Zimbabwe after land reform has to be significantly tempered, there is clearly potential. As noted at the beginning of this article, Zimbabwe's land reform was a cross-class compromise, with the A2 farms being part of a political deal with the professional middle class and the party-military elite. That a diversity of outcomes on these farms has been experienced over nearly 20 years should not be a surprise.

The implications for rural politics are not straightforward. If the A2 ‘commercial farmers’ continue to gain state support and are able to extend processes of accumulation, they may act to push out the ‘struggling farmers’, who may lease (or informally sell) land and take up labouring for the larger, more successful farmers, or move away altogether. Much will hinge on the significant group of ‘aspiring farmers’, whose political connections, and so allegiances, are less certain. With greater stability in Zimbabwe's political and economic context, they may yet emerge as the new drivers of commercialisation, as seen elsewhere in Africa.

Such a differentiated examination of what people are doing, and the underlying trajectories of accumulation, to date largely absent in the wider literature on medium-scale farms in Africa, suggests diverse implications for policy. A dominant theme is access to finance and markets, sufficient to allow those who are aspiring – and often trying under desperate circumstances – to step up to a more stable, commercial trajectory. The wild fluctuations in macro-economic conditions in Zimbabwe, and periodic bouts of extreme economic chaos, mean that attempts to accumulate are wiped out. A stable, functioning economy is a basic requirement for any business and, if there is any single policy priority for the future of medium-scale farms in the post-land reform setting of Zimbabwe, macro-economic stabilisation must be it. This must come with effective financing options, including private finance using land leases as collateral, as well as transparent, accountable, but time-limited and targeted, subsidy policies. Lessons from the past are relevant. The emergence of large-scale commercial agriculture in Zimbabwe during the colonial era and into Independence occurred through an alliance between white-owned agrarian capital – ranging from family farmers to large agribusiness concerns – and the state (Scoones et al. Reference Scoones, Shonhe, Chitapi, Maguranyanga and Masikinye2020). This was essential to the political compact that existed through colonial occupation, the Unilateral Declaration of Independence period and that continued after Independence (Herbst Reference Herbst1990).

That large areas of potentially productive land are being under-used is clear. But we also have to recall that extensive use of land for livestock grazing (in Masvingo-Gutu) and cultivation in patches due to the rocky, mountainous terrain (in Mvurwi) means that land utilisation figures have to be evaluated with caution. Equally, it is not as if commercial agriculture in the past always fully used the land. Indeed, estimates from the 1960s to the 1990s have shown only 15–23% of land being used in ‘European’ commercial farm areas,Footnote 15 even in the productive Mazowe district (Weiner et al. Reference Weiner, Moyo, Munslow and O'Keefe1985). Nevertheless, land utilisation on the A2 farms remains a key policy issue.

What, then, is the significance of medium-scale farms for Zimbabwe's agrarian future? Compared with the earlier surveys in the mid-2000s, there was much more activity in 2018–19 and, from some farms, a considerable volume of production and sale. Sometimes very closely allied with the party-state, sometimes as independent or joint-venture arrangements, there is an emergence of a new form of capitalist, commercial agriculture, and this is especially evident in Mvurwi on the back of the tobacco boom. Beyond this, there are others who aspire to become part of a new class of capitalist farmer, but remain severely constrained. The state's lack of resources, combined with entrenched corruption and patronage relations, means that this group is not achieving what it might. But with new investment, new forms of joint-venture and an injection of flexible finance, the scope of vibrant commercial agriculture could be expanded. Meanwhile, the dynamics of what we have termed ‘villagisation’ and investment in ‘projects’ will continue, often linked to diaspora remittance finance.

The now numerous studies of medium-scale farms across Africa have highlighted their importance for the future of Africa's agrarian economies. As this article shows, the emergence of medium-scale farms in Zimbabwe, in this case through land reform, is also reshaping the political economy of agrarian change. We must, however, avoid taking medium-scale farms as a unitary category. In Zimbabwe, processes of differentiation are resulting in different trajectories of accumulation and class formation, with commercial, aspiring and struggling farmers. These differentiated groups have divergent political interests, with some closely allied with the party-state and reliant on patronage connections for accumulation, while others are ‘accumulating from below’ or not at all, joining wider, fragmented ‘classes of labour’ in Zimbabwe's post-land reform countryside. As the focus for emergent capitalist agriculture and the location of influential political, military and professional elites, the medium-scale A2 farms are thus defining a new politics of commercial agriculture in Zimbabwe's countryside following land reform.

Open access

Open access