1. Introduction

Economic history books will commemorate the era we currently live in as the second wave of financial globalization, following the first wave during the Classical Gold Standard period. Our era is characterized by an unprecedented expansion of global financial flows. Partly, these flows form the counterpart to global value chains and the globalization of trade in goods and services. In the last few decades, however, they have been increasingly decoupled from the real sector. The financial infrastructure that enables this expansion is the international monetary system.

How the international monetary system is set up is of paramount importance for the global political economy and crucially influences issues such as financial stability, social inequality and the global distribution of power. Despite this significance, conceptualizing today's financially globalized international monetary system has proven very difficult (Hodgson, Reference Hodgson2015). Historical configurations such as the Gold Standard or the Bretton Woods System are well understood, but how can we characterize the contemporary setup? As it has not been purposefully designed, scholars frequently describe it even as a ‘non-system’ (e.g. Ocampo, Reference Ocampo2017). In particular, the profound reduction in the significance of states under the conditions of financial globalization provides an intellectual challenge. To a large degree, the international monetary system is now dominated and organized by private institutions.

The institutional evolution of the international monetary system has been discussed at various times in the past century, e.g. in the lead up to the Bretton Woods conference in the 1940s (cf. Keynes, Reference Keynes1944) and around the collapse of the Bretton Woods System in the 1970s (cf. Cohen, Reference Cohen1977; Cooper, Reference Cooper1975; Machlup, Reference Machlup1968; Mundell, Reference Mundell, Keith Acheson, Chant and Prachowny1972; Triffin, Reference Triffin1960). In the post-2008 crisis era, a new debate has emerged (cf. Eichengreen, Reference Eichengreen2009; Eichengreen et al., Reference Eichengreen, Mehl and Chiţu2017; Farhi and Maggiori, Reference Farhi and Maggiori2018; Farhi et al., Reference Farhi, Gourinchas and Rey2011; Ocampo, Reference Ocampo2017; Prasad, Reference Prasad2006; Zhou, Reference Zhou2009). Scholarship on the international monetary system's evolution typically focuses on the role of reserve currencies, in particular whether the US-Dollar (USD) is likely to keep this status, and whether that is desirable. The international monetary system is usually viewed as encompassing the particular setup of fixed or flexible exchange rates between monetary jurisdictions, the degree of international capital mobility as well as the extent to which autonomous national monetary policy is possible (Eichengreen, Reference Eichengreen2008). Such thinking is in line with the ‘Impossible Trinity’, which holds that a country can only have two of the three following features: open capital accounts, fixed exchange rates and an independent monetary policy (Broz and Frieden, Reference Broz and Frieden2001). Operating in this framework, scholarship often leaves out key characteristics of today's financially globalized world, or treats them at best as a footnote while not acknowledging that they have become essential features of the system: Firstly, scholars are biased towards discussing the role of the state in the international monetary system while neglecting privately created money substitutes (Frasser and Guzmán, Reference Frasser and Guzmán2020). Secondly, they focus on money forms that are issued onshore within a given monetary jurisdiction, while neglecting the enormous significance of offshore credit money creation (Awrey, Reference Awrey2017).

To adopt categories that are more fitting for a financially globalized world, we describe the current setup of the international monetary system as paradigmatically based on the creation of private USD-denominated credit instruments abroad and thus label it as ‘Offshore US-Dollar System’. This system evolved primarily through the initiative of private profit-oriented financial institutions that shifted the activities of credit money creation offshore. While public authorities facilitated the process, they were not its main drivers. The primacy of the political came about only in a systemic crisis when emergency interventions steered the system's further evolution. Thus, the article adopts the analytical perspective that the transformation which led to the emergence of the Offshore US-Dollar System followed a functionalist logic – private agency pushes institutional transformation forward and with a time lag public agency follows suit to backstop the system in a crisis (Minsky, Reference Minsky1986; Murau, Reference Murau2017a; Ülgen, Reference Ülgen2014).

Financial globalization is not an automatic or natural state of affairs, but a specific institutional configuration that has materialized as the result of evolutionary processes since the end of the Second World War in a situation characterized by the political, economic and monetary hegemony of the United States (US). As a construct built by humans, it is not there to stay forever but we cannot know for how long this era of financial globalization will prevail. The international monetary system continues to be subject to ongoing transformation dynamics, with a multitude of exogenous and endogenous factors, both political and economic, contributing to these dynamics. Taking into account the distinctive institutional evolution of the international monetary system in the last decades, we extrapolate different contemporary trends into the future. We will follow four different potential trajectories for the continuous institutional evolution which give rise to four respective possible futures for the international monetary system and financial globalization.

The remainder of this article is organized as follows. Section 2 explains our conceptual framework, which is based on categories that go beyond the traditional notions of money and the nation state. It develops a figurative language that will allow us to depict specific historical and possible future institutional setups of the international monetary system. Section 3 explains the evolution of the international monetary system into its current shape as Offshore US-Dollar System. Section 4 compares four different possible trajectories of the international monetary system's institutional evolution. In addition to a continuation of USD hegemony, we present the emergence of competing monetary blocs, the formation of an international monetary federation and the drifting into an international monetary anarchy. Section 5 concludes.

2. Conceptualizing the contemporary international monetary system as ‘Offshore US-Dollar System’

As an entry point of our analysis about the past, present and possible futures of the international monetary system, we seek to transcend the traditional categories of the Mundell Fleming model (Fleming, Reference Fleming1962; Mundell, Reference Mundell1963). We contend that this standard model overly relies on categories tied to the Westphalian nation state such as the idea that money creation is connected to public institutions and confined to a state's territory. Many of our basic intuitions which are connected to this idea of Westphalian monetary sovereignty are at odds with the realities of a financially globalized world (Murau and van ’t Klooster, Reference Murau and van ’t Klooster2019).

This traditional view on the international monetary system assumes what the Bank for International Settlements (BIS) calls ‘triple coincidence’: that a state's territory, the decision-making area and the monetary area are identical (Avdjiev et al., Reference Avdjiev, McCauley and Shin2015). In the age of financial globalization, however, this triple coincidence has disappeared. Instead, the international monetary system is built on money creation that is substantially de-coupled from the nation state. Not only is the vast majority of credit money created by private institutions, but the core of the system also relies upon credit money created outside of a state's decision-making area.

In this article, we develop a framework that allows us to use categories which are more fitting to the realities of financial globalization than those of the nation state with Westphalian monetary sovereignty and the world of the Mundell Fleming model. We follow the approach of a market-based credit theory of money (Murau, Reference Murau2017b) which assumes that what is often defined as ‘currencies’ such as the USD, the Euro (EUR) or the British Pound (GBP) are primarily nominal units of account. These are used for denominating debt certificates some of which are referred to as ‘money’. The origins of this view may be traced back to Alfred Mitchell-Inness (Reference Mitchell-Innes1914: 155) who famously states that ‘the eye has never seen and the hand has never touched a dollar. All that we can touch or see is a promise to pay or satisfy a debt due for an amount called a dollar’. This view has inspired works such as Keynes (Reference Keynes1930) and Minsky (Reference Minsky1986). In fact, in the current age of financial globalization, all systemically relevant forms of money are credit money (Mehrling, Reference Mehrling2011; Pozsar, Reference Pozsar2014).

The units of account that are de facto in use today are closely intertwined with state structures. The USD is the US' unit of account, the GBP is that of the United Kingdom (UK), and the EUR is the unit of account of the European Union – or rather those EU countries that have chosen to join the European Monetary Union. However, creating money denominated in those units of account does not have to be carried out by state actors themselves nor take place within the political decision-making area of a state. We call this decision-making area the ‘monetary jurisdiction’ because it is a legal, not a geographical, category. It refers to the legal space in which a state's banking regulation applies and where, in turn, liquidity and solvency backstops are in place for banks.

The term ‘monetary area’, by contrast, denotes the sphere in which a given unit of account is used to denominate credit money creation. We base this notion of a monetary area that exceeds a state's territory on recent conceptual and empirical work by the BIS (Avdjiev et al., Reference Avdjiev, McCauley and Shin2015; Borio et al., Reference Borio, McCauley and McGuire2017; Ito and McCauley, Reference Ito and McCauley2018). ‘Offshore’ money creation in our definition takes place outside of a state's monetary jurisdiction, but within the monetary area of that state's unit of account. When using the term ‘offshore’, readers may be prone to think about tax havens and the Cayman Islands. However, we use the term in a more general sense. Empirically, the largest centre for offshore money created is located in the City of London. In this conceptualization, a London bank is located in the monetary jurisdiction of the UK and in addition can feature as part of the monetary areas of the USD and the Euro.

The extent to which a unit of account is used for offshore money creation depends on how much it is sought after in global finance and trade (Maggiori et al., Reference Maggiori, Neiman and Schreger2019). As a rule of thumb, the more commodity and financial markets make use of this unit of account for the purpose of denomination, the more credit money denominated in that unit of account will be created offshore. This is particularly relevant for the USD. In fact, BIS analyses suggest that today more USD creation takes place offshore than onshore (Aldasoro and Ehlers, Reference Aldasoro and Ehlers2018; Borio et al., Reference Borio, McCauley and McGuire2017; Ito and McCauley, Reference Ito and McCauley2018).

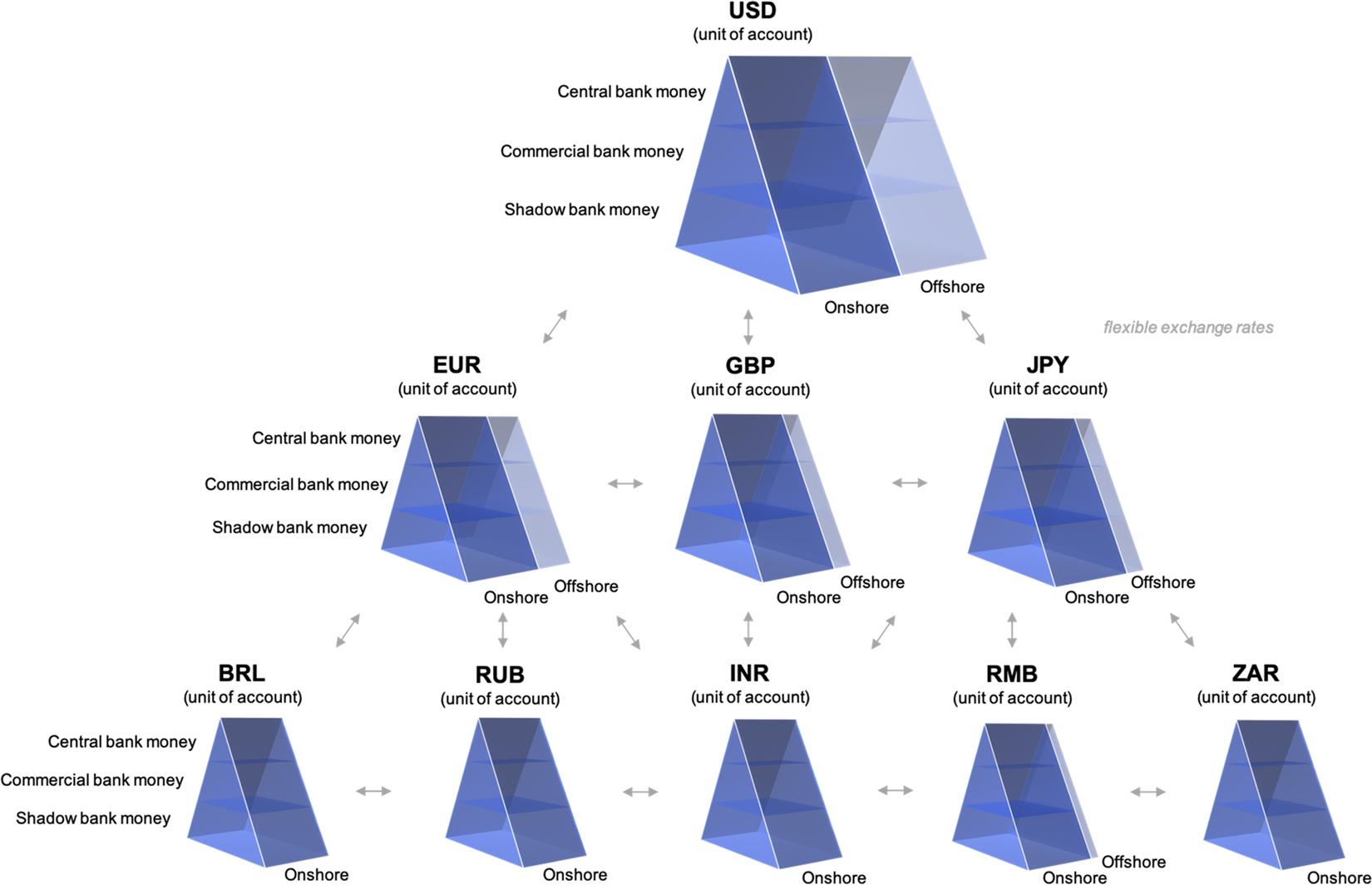

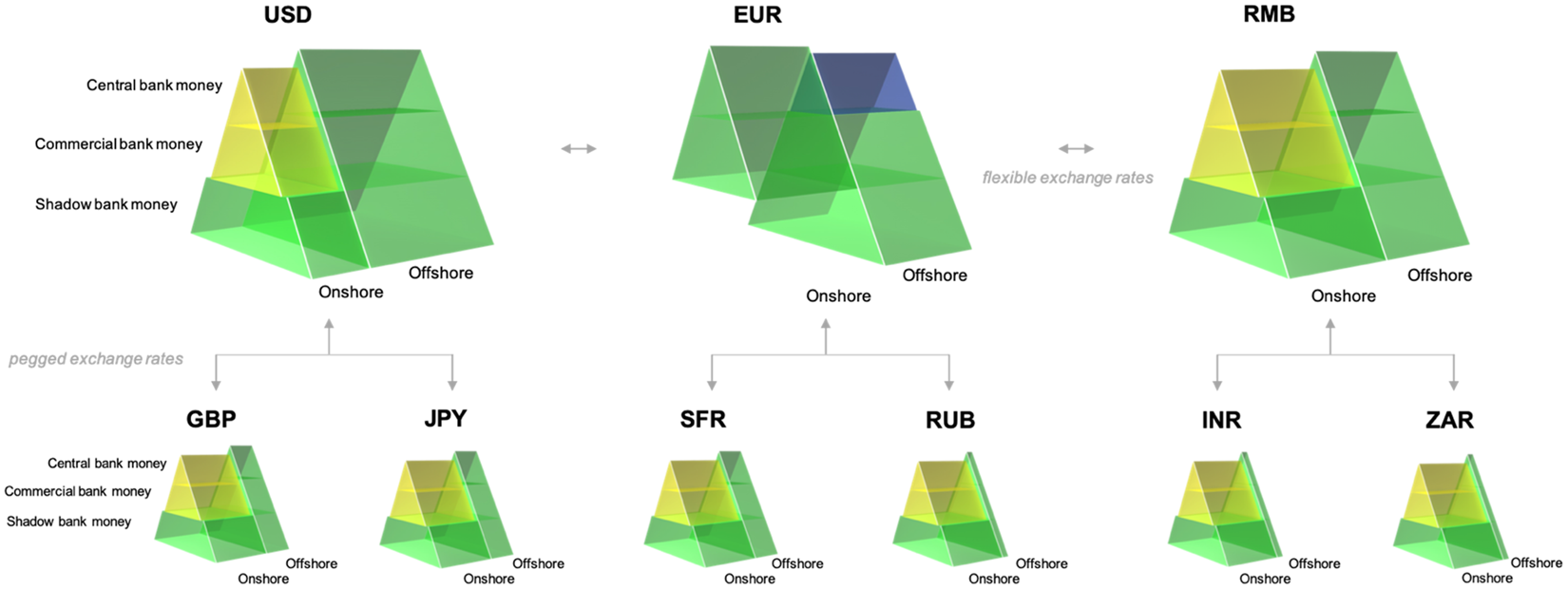

Figure 1 presents our visual analytical framework to depict the Offshore US-Dollar System. It frames today's financially globalized international monetary system as a hierarchical construct in a double sense: as a pyramid of pyramids that represent monetary areas. Within a monetary area, the monetary system is configured as a hierarchy of money forms issued by different types of financial institutions, both onshore and offshore. Globally, different monetary areas form a hierarchical system with an apex and a multilayered periphery. Let us look at it more in detail.

Figure 1. The international monetary system as ‘Offshore US-Dollar System’. USD, US-Dollar; EUR, Euro; GBP, British pound; JPY, Japanese yen; BRL, Brazilian real; RUB, Russian ruble; INR, Indian rupee; RMB, Chinese renminbi; ZAR, South African rand. © 2020 Steffen Murau (CC-BY).

First, within a monetary area, three types of public and private financial institutions – central, commercial and shadow banks – create credit money when they expand their balance sheets to simultaneously extend a loan and issue credit money as their liability (Werner, Reference Werner2016). Central bank money – made up of central bank notes and reserves – is the hierarchically highest and at the same time scarcest form of money. We think of it not as fiat money or exogenous reserve assets for fractional reserve banking (Bauwens, Reference Bauwens2016) but as public credit money (Mehrling, Reference Mehrling2020). More abundant and hierarchically lower money forms include deposits created by commercial banks and deposit substitutes typically created by shadow banks, often termed ‘shadow money’ (Gabor and Vestergaard, Reference Gabor and Vestergaard2016; Murau, Reference Murau2017a; Pozsar, Reference Pozsar2014).

Generally speaking, shadow banks can be defined as non-bank financial institutions which have a legally different status than traditional banks but which in some respects related to money creation perform functionally equivalent operations (Ricks, Reference Ricks2016). This definition, however, has its limitations. In Europe's universal banking system, for example, shadow banking activities are traditionally largely carried out on commercial banks' balance sheets (Bayoumi, Reference Bayoumi2017), even though there is a trend towards shifting more to non-bank balance sheets (European Central Bank, 2020). As shadow banking is geared towards circumventing banking regulations in various ways, it is hard to find specific definitions that apply broadly across space and time. Whether or not a given institution is a shadow bank may easily be subject to contestation, and also some commercial banks act as shadow banks. Still, on the level of instruments, we can more easily maintain a distinction between traditional commercial bank money and different forms of shadow (bank) money (Murau and Pforr, Reference Murau and Pforr2019). This is the analytical entry point we adopt in this article.

Money creation, denominated in a given unit of account, occurs within a monetary area either onshore or offshore. ‘Onshore’ money creation takes place within a monetary jurisdiction, for example, when USD-denominated credit money is issued legally in the US. This is the dark blue space on the left side of each pyramid. ‘Offshore’ money creation, represented by the grey-blue space on the right of each pyramid, takes place, for example, when a bank creates USD-denominated deposits in London. To re-iterate, the offshore space belongs to the monetary area specific to a unit of account, but it is legally situated in a different monetary jurisdiction which allows offshore money creation and where the issuing institution is domiciled.

The money forms created by central, commercial and shadow banks denominated in one unit of account, whether onshore and offshore, typically trade with each other at par, at a one-to-one rate. This conceals inherent differences between the different money forms, especially when we speak in the everyday language of ‘the Dollar’, ‘the Euro’, etc. That they trade at par with each other is the defining feature that makes them money, as opposed to other credit instruments denominated in that unit of account which are subject to price fluctuations (Mehrling, Reference Mehrling2011; Pozsar, Reference Pozsar2014).

Second, the ensemble of different monetary areas forms an international hierarchy with the USD situated at the top of it (Kaltenbrunner and Lysandrou, Reference Kaltenbrunner and Lysandrou2017). Other units of account form a multi-layered periphery to it (Cohen, Reference Cohen1998; Strange, Reference Strange1971). This conceptualization follows a ‘key currency’ approach to the international monetary system (Kindleberger, Reference Kindleberger1970; Williams, Reference Williams1934). The contemporary empirics of it can only be roughly sketched in Figure 1. The units of account of other G7 members such as the EUR, the GBP or the Japanese yen (JPY) constitute the first layer of peripheral monetary jurisdictions. A second layer is formed by other advanced economies, here represented by the BRICS. They issue Brazilian real (BRL), Russian rubles (RUB), Indian rupees (INR), Chinese renminbi (RMB) and South African rand (ZAR). The model could be further extended with additional layers and monetary areas, but in this depiction, we think of it as sufficient to convey the idea.

The different monetary areas interface with one another via international exchange rates, which can be fixed or floating. Traditional analyses of the international monetary system predicated on categories of the Westphalian monetary system place primary importance on these exchange rate arrangements. Our analysis, however, shifts the attention away from exchange rates because the possibility of offshore money creation reduces the need to convert into different units of account in cross-border transactions (Awrey, Reference Awrey2017).

In the current historical shape of the international hierarchy, international payment flows in overwhelming quantity are organized via the USD monetary area. The USD-denominated credit money for this purpose is predominantly created offshore, first and foremost via the Eurodollar market. Therefore, the USD monetary area has the most sizable offshore component, followed by that of the EUR, and lastly those of the JPY and the GBP (Denbee et al., Reference Denbee, Jung and Paternò2016; Gabor, Reference Gabor2013). The BRICS countries so far have only a marginal share of offshore credit money creation, although China in particular is heavily pushing its offshore RMB market (Bernes et al., Reference Bernes, Jenkins, Mehrling and Neilson2014; He and McCauley, Reference He and McCauley2012).

3. The institutional evolution of the Offshore US-Dollar System

In July 1944, when delegates of the Allied countries which were about to win the Second World War met at a now legendary conference in Bretton Woods, New Hampshire, to discuss the future of the international monetary system, the various domestic monetary systems that were to become part of the international regime corresponded relatively well to the Westphalian ideal of ‘one country, one currency’ (Cohen, Reference Cohen1998). The first wave of globalization during the Classical Gold Standard era had been scaled back. Finance was predominantly organized nationally again, and John Maynard Keynes – head of the British delegation to the Bretton Woods conference – famously called for leaving it this way.

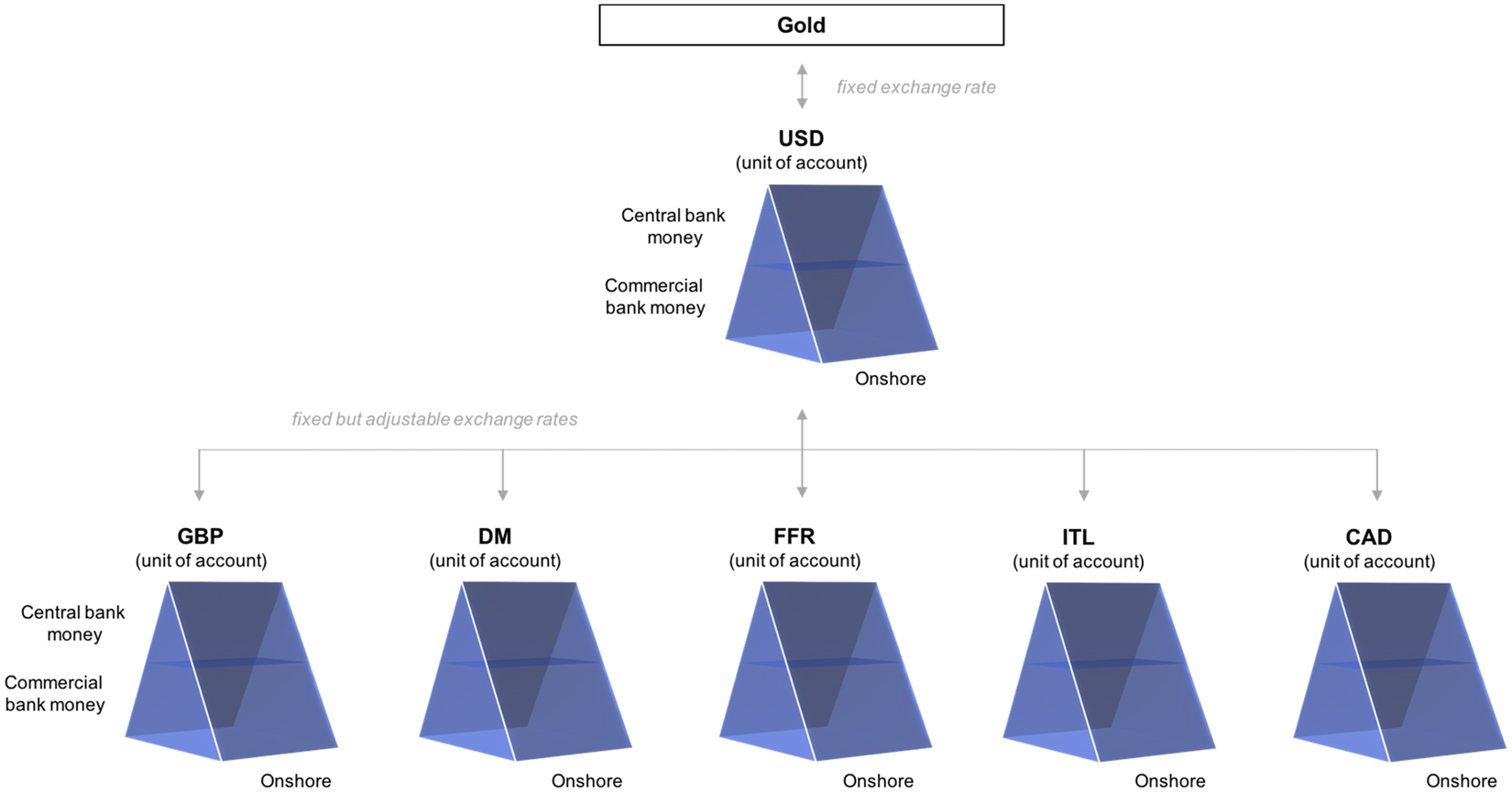

The outcome of the Bretton Woods conference was the establishment of a US-Dollar-gold-standard. Figure 2 visualizes the design of the Bretton Woods System, considering the setup of the various national monetary areas. Nominally on top of the international hierarchy was gold as a commodity. US authorities guaranteed a fixed exchange rate of it into USD, i.e. the liabilities issued on the balance sheets of the Fed and US commercial banks. All other units of account had fixed but adjustable exchange rates to the USD. The figure depicts a not comprehensive number of monetary areas that were part of the system and formed a periphery to the USD as the apex. These peripheral monetary areas had a roughly similar setup as the US with onshore central and commercial bank money. An important issue to appreciate is that the system, despite its gold convertibility, was a credit money system with the balance sheets of the Federal Reserve and US banks as the dynamic core (Mehrling, Reference Mehrling2016).

Figure 2. The design of the Bretton Woods System. USD, US-Dollar; GBP, British pound; DM, Deutsche Mark; FFR, French franc; ITL, Italian lira; CAD, Canadian dollar. © 2020 Steffen Murau (CC-BY).

Much has been written on the deficiencies of the Bretton Woods system. With a constant increase in the volume of USD-denominated credit money, the ratio between the US’ gold stock and USD credit money became smaller and smaller, making it more and more likely that at some point the gold conversion promised by the US could no longer be redeemed. This problem, most famously described by Triffin (Reference Triffin1960), is widely perceived as the structural core deficiency that led to the suspension of gold convertibility by the Nixon Administration in 1973.

Even more important for the trajectory of the international monetary system's transformation was the rise of offshore USD creation. What had started off as a fringe phenomenon had been established firmly enough by the 1970s to replace the then crumbling US-Dollar-gold-standard of the Bretton Woods System. The international monetary system entered the era of the Offshore US-Dollar System. The usual emphasis of scholarship lies on the shift from fixed to flexible exchange rates. But this is only part of the story. Offshore USD creation made it possible to use a single unit of account for cross-border real and financial transactions, and thus to reduce the need for currency conversion and exchange rate risk. Instead, exchange rates in between different units of account were replaced by a par exchange rate between onshore and offshore USD. Hence, as the Bretton Woods System became increasingly dysfunctional, the emerging Offshore US-Dollar System provided an institutional alternative that had not been centrally planned but evolved in an evolutionary process. Whether the rise of the Offshore US-Dollar System was a cause for or an effect of the demise of the Bretton Woods System is subject to ongoing contestation among scholars (Braun et al., Reference Braun, Krampf and Murau2020; Burn, Reference Burn2006; Eichengreen, Reference Eichengreen2008; Helleiner, Reference Helleiner1994; Mehrling, Reference Mehrling2016).

Figure 3 depicts the institutional evolution of the USD monetary area, located at the apex of the Offshore US-Dollar System, to sketch the most important steps in the emergence of offshore USD creation. We may describe the dynamics at play here as functionalist institutional evolution (Minsky, Reference Minsky1986; Murau, Reference Murau2017a): Private profit-driven financial institutions have used available regulatory spaces for financial innovations to create new forms of credit money outside of the regulated US banking system. Within the US monetary jurisdiction, non-bank financial institutions created new forms of shadow money. Outside of the US monetary jurisdiction, banks and non-banks created various offshore instruments. The role of public institutions was largely that of a bystander who was partly passive, partly complicit, but certainly not in the driver's seat. The dominance of public institutions has only set in major crises when the inherently instable private system needed public balance sheets as ‘deus ex machina’ to prevent it from imploding. At the end of the institutional transformation stands a symmetric system of onshore and offshore money creation by central, commercial and shadow banks. This is where we stand today at the beginning of the third decade in the 21st century.

Figure 3. The institutional evolution of the US-Dollar monetary area. MMF, money market fund; ABCPs, asset-backed commercial papers; repos, repurchase agreements. © 2020 Steffen Murau (CC-BY).

Let us look at the institutional evolution of the US monetary area more in detail. Offshore USD creation started with the emergence of the Eurodollar marketFootnote 1 in 1956 (Einzig, Reference Einzig1964) – a financial innovation that did not emerge out of systematic planning, but ‘more or less by accident’ (Kindleberger, Reference Kindleberger1970: 173). London bankers, with the vigorous support of the Bank of England and the British treasury (Burn, Reference Burn2006; Helleiner, Reference Helleiner1994), invented Eurodollars as a new form of USD-denominated credit instruments that were not subject to US regulation and oversight – in particular regulation Q, a rule introduced after the Great Depression which capped the interest rates payable on onshore dollar deposits.

In the early years, communist countries were interested in USD business without directly engaging with the US, and global oil trade was organized through the market: petrodollars are Eurodollars. In the 1960s, New York banks discovered the Eurodollar market for their purposes to circumvent domestic US regulations. ‘Roundtrip transactions’ from the US via London back to the US became the dominant feature (He and McCauley, Reference He and McCauley2012), turning the Eurodollar market into what it effectively is today: an extension of the US onshore interbank market, the Fed Funds market, into the offshore segment. Hence, the usage of the Eurodollar skyrocketed in the 1970s, which correlates of course with the collapse of the Bretton Woods system.

In 1972–73, representatives of the G-10 central banks held intensive negotiations at the BIS whether the Eurodollar market could and should be regulated. Altamura (Reference Altamura2017) refers to these as the ‘Battle of Basel’. The German Bundesbank and the Banca d'Italia presented tangible proposals but could not create a majority among the central banks for concerted action. These proposals would have implied that central banks reciprocally apply regulation and coordinated monetary policy operations for offshore deposits created in their respective monetary jurisdictions. While the Bank of England was strongly opposed to such reforms, the Federal Reserve changed its opinion several times on whether the emerging Offshore US-Dollar System was a threat or an opportunity (Hawley, Reference Hawley1984). From 1974, after the first oil crisis, the G-10 central banks decided to actively use the Eurodollar market to tackle the policy challenges they were facing and began to organize ‘petrodollar recycling’ through the Eurodollar market. This turned offshore USD creation into a truly global phenomenon and filled the gap that the collapse of the Bretton Woods System had left.

The 1970s also was the time when the financial structures evolved that have come to be called the shadow banking system today. Non-bank financial institutions based in the US invented new instruments that, just as the instruments on the Eurodollar market, competed with the highly regulated onshore USD bank deposits. A key prerequisite was to find ways to establish par between those ‘shadow money forms’ and onshore deposits. This was achieved through a combination of private guarantees, creative accounting techniques and exploiting the balkanized US regulatory system. Money market funds offered shares as deposit alternatives but were able to pay higher interest than banks because they were regulated as funds. Security dealers developed a parallel banking system around overnight repos. Large institutional investors could deposit funds overnight against high-quality collateral with interest, just as they would do at a bank. If they roll over the overnight repo, they keep their deposit. If they refrain from rolling it over, they ‘withdraw’ it (Murau, Reference Murau2017a).

Shadow money was initially an onshore phenomenon but developed a sizable offshore component in the 1980s, in particular via the market for asset-backed commercial papers (ABCPs). This market evolved in the context of the international regulatory standards that oblige banks to build up reserves when they grant loans and thus draw on their customers' deposits. Since such reserves reduce profitability, banks invented the trick to set up a special purpose vehicle offshore and handle some of their lending business via that channel. Instead of bank deposits, they drew on ABCPs that did not appear on their balance sheets. In this way, they could circumvent the rules on building up reserves and increase their profitability. When it boils down to it though, this is not much different from ordinary credit money creation, apart from the fact that shadow money is used (Acharya and Schnabl, Reference Acharya and Schnabl2010; Haberly and Wójcik, Reference Haberly and Wójcik2017).

The turning point for the quantitative and qualitative expansion of private USD-denominated deposit substitutes was the 2007–9 Financial Crisis. The crisis was a worldwide bank run that simultaneously took place within the offshore USD segment and the shadow banking system, marked red in Figure 3. In August 2007, falling prices on the US real estate market put investors in offshore and shadow money into doubt whether those instruments could keep up the promised par exchange rate vis-à-vis onshore deposits. Investors' impulse to convert their offshore and shadow money balances into onshore deposits which are protected by the federal deposit insurance triggered a self-fulfilling prophecy. Out of fear that par might break away, a critical mass of investors behaved in a way that actually broke par. The ensuing chain reaction infected more and more segments of the financial system and led the leading investment bank Lehman Brothers go into bankruptcy due to its defaulting repo dealer.

In reaction to the crisis, US authorities adopted a number of unprecedented emergency measures to reduce strains on the US onshore banking system and maintain the par exchange rate between onshore USD deposits and USD-denominated offshore and shadow money. Within the US monetary jurisdiction, the Fed and the US treasury extended deposit insurance to money market funds shares and repos. To stabilize the Eurodollar market in the offshore segment, the Fed established temporary emergency USD swap lines with 14 partnering central banks. This put the partnering central banks de facto in the position to create offshore USD as public money on their own balance sheets and lend it on to banks domiciled in their jurisdiction (Baba et al., Reference Baba, McCauley and Ramaswamy2009). The Fed effectively turned the other central banks into its branches to extend its reach into the offshore USD segment and safeguard the structures of financial globalization.

After the crisis, the Fed made five of the emergency swap lines which had been created as immediate crisis response permanent in time and unlimited in volume. The partnering central banks that form this ‘C6 Swap network’ are the ECB, the Bank of England, the Bank of Japan, the Bank of Canada and the Swiss National Bank (Mehrling, Reference Mehrling2015). The C6 swap network represents the ultimate line of defence against new systemic financial crises in the present version of the Offshore US-Dollar System. The six central banks, chaired by the Fed, thus form a multilateral forum which – at least for the leading advanced economies in the West – can act as an international lender of last resort.

4. What future trajectories for the evolution of the Offshore US-Dollar System?

Setting up the C6 swap network has opened up a new chapter in the history of the international monetary system (Tooze, Reference Tooze2018). The swap lines form a new multilateral last line of defence to backstop the financially globalized Offshore US-Dollar System. In the post-crisis environment, offshore USD creation has even gained pace (Shin, Reference Shin2013). At the same time, the post-crisis version of the Offshore US-Dollar System relies more than ever on one single global backstop, the Federal Reserve, which does not have any officially codified global responsibility. How stable and resilient will this institutional arrangement turn out to be in the decades to come?

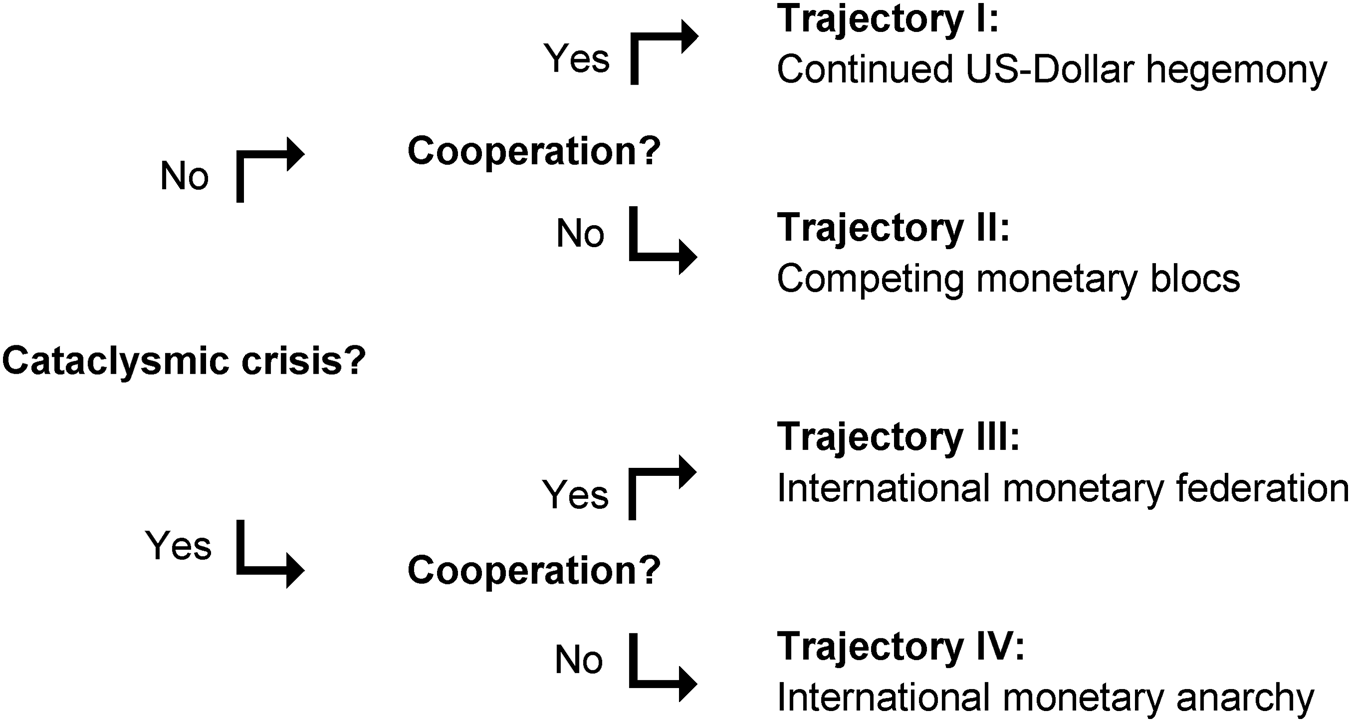

To explore the possibility space for the future systemic transformation, we will now spell out four different trajectories, i.e. development paths, leading to different setups of the system by 2040. We extrapolate existing trends into the future to discuss possible evolutionary paths of the international monetary hierarchy and offshore money creation. Our key analytical questions are whether there will be a system-changing financial breakdown (think 2007–9 without the Fed's emergency measures) and whether global economic governance is shaped by collaboration or competition (see Figure 4).

Figure 4. Four trajectories for the Offshore US-Dollar System's evolution.

Following these four trajectories will yield different outcomes for which we sketch brief narrative examples. The first two trajectories highlight ‘evolutionary’ outcomes that are close to today's Offshore US-Dollar System. The latter two trajectories depict two examples for ‘revolutionary’ outcomes and a profoundly changed international monetary system. We do not claim that these trajectories are the only possible or relevant futures of the international monetary system – without a doubt, the number of possible futures is infinite. Instead, our key interest lies in sketching a strict subset of the possibility space for the structural setup of the international monetary system and connecting it to specific transformation dynamics. To add plausibility and also to de-naturalize the current evolutionary trajectory, we point to historical precedence in which the international monetary system had indeed fundamentally different structural setups.

We resist the temptation to attribute probabilities to individual trajectories, even though each era has its fashionable beliefs about how the future may look. Rather, we focus on the interplay of technical institutional alternatives, political-economic power and path dependencies. We argue that as long as the Fed is willing and able to play its role as de facto but not officially announced backstop for the global credit money system, the Offshore US-Dollar System has too strong of a network externality to be entirely replaced, even if the institutional alternative may look much more promising on paper.

4.1 Trajectory I: continued USD hegemony

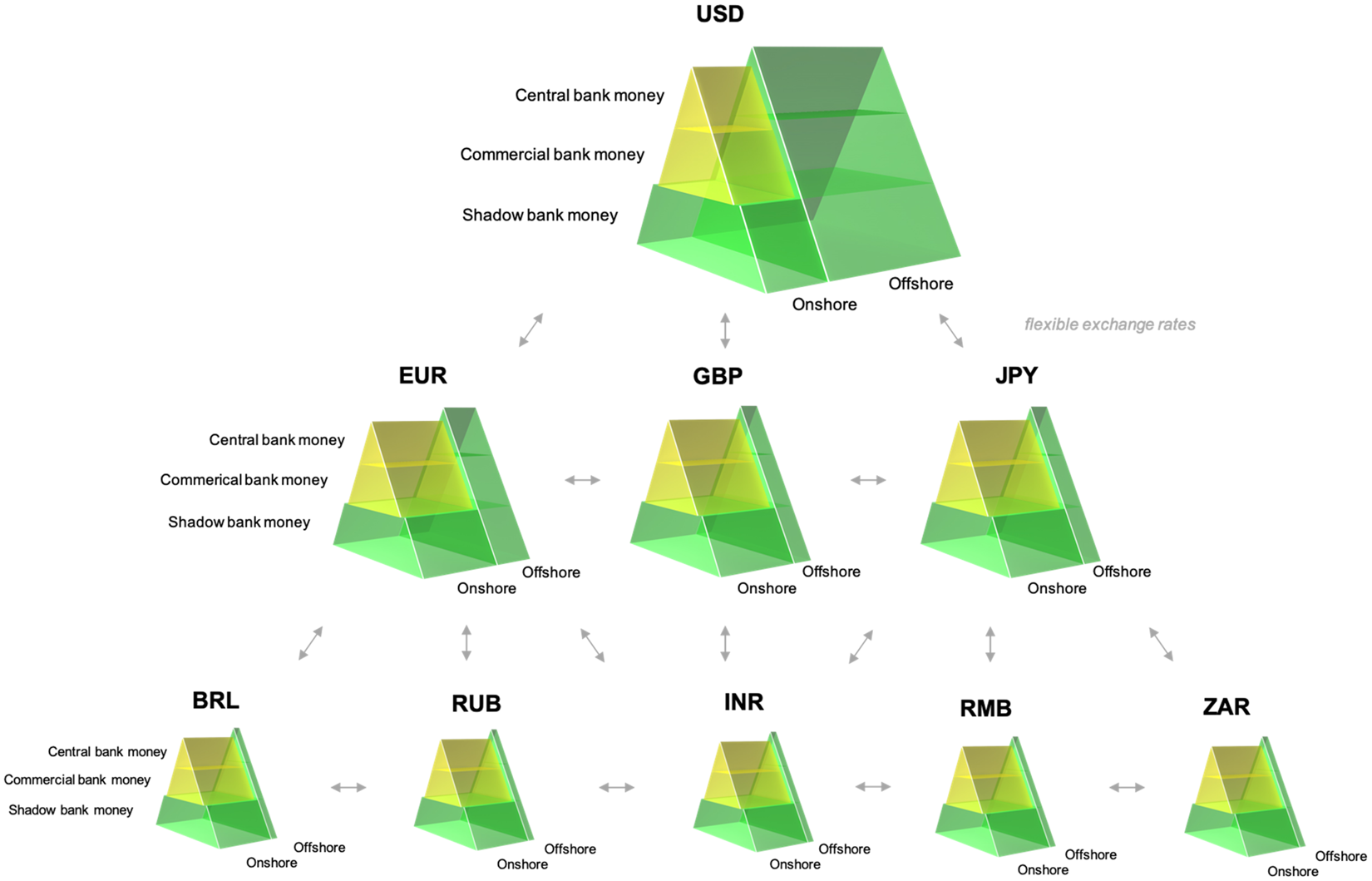

In the trajectory that leads to continued USD hegemony, a situation evolves in which the offshore dollar system has further expanded along similar dynamics as in the past decades. Private profit-oriented institutions remain the dominant force in institutional transformation. The international monetary system stays with the shape of a single international hierarchy with the USD at its top, and offshore credit money creation expands further as the discrepancy between states' monetary jurisdiction and their unit of account's monetary area grows (see Figure 5). This is still a world of financial globalization.

Figure 5. Continued US-Dollar Hegemony. USD, US-Dollar; EUR, Euro; GBP, British pound; JPY, Japanese yen; BRL, Brazilian real; RUB, Russian ruble; INR, Indian rupee; RMB, Chinese renminbi; ZAR, South African rand. © 2020 Steffen Murau (CC-BY).

While classical central bank and commercial bank money have declined in importance (marked yellow), the offshore and shadow money components of the USD monetary area are further expanded (marked green). We see an international monetary system that is further stabilized and backstopped by the Fed's network of unlimited swap lines, which are perceived as credible and safe.

Peripheral monetary areas have also increased their share of offshore and shadow money creation, yet at a lower scale. The network externality of the smoothly functioning Offshore US-Dollar System, supported by the powerful Fed, proves too strong for other currencies to break the USD hegemony. Monetary jurisdictions that have access to the Fed's unlimited swap lines are still higher up in the international hierarchy than those which do not.

This trajectory is a conservative continuation of today's Offshore US-Dollar System. It is likely to materialize if there is no system-changing financial crisis and the US continues to back the liberal world order. Global Trumpism and the America First mentality would turn out to be merely a transitory phenomenon. The Eurozone, by contrast, would remain in the gridlock of a dysfunctional monetary governance architecture, while China does not succeed in developing the deep and liquid financial markets it currently lacks.

4.2 Trajectory II: competing monetary blocs

In the trajectory that leads to competing monetary blocs, we envision the EU and China emerging as serious counterweights to the US monetary hegemony. The unipolar hierarchy of today's system gives way to three different hierarchical structures that co-exist next to each other. In each of the blocs, the monetary area of the centre country forms the apex of the respective regional hierarchy and sub-ordinates peripheral monetary jurisdictions (see Figure 6). Exchange rates tend to be fixed within and flexible in between the blocs. As a result, the interconnectedness in finance and consequently trade has been sharply reduced between the blocs. This is a world of financial regionalization.

Figure 6. Competing monetary blocs. USD, US-Dollar; GBP, British pound; JPY, Japanese yen; EUR, Euro; SFR, Swiss francs; RUB, Russian ruble; INR, Indian rupee; RMB, Chinese renminbi; ZAR, South African rand. © 2020 Steffen Murau (CC-BY).

The US and the Chinese monetary jurisdictions both allow shadow and offshore money creation. The Fed and the Bank of China have further invested in their swap networks that provide backstops to offshore USD and Renminbis, respectively. In the EU, calls for stricter financial regulation have been heard, and policy makers have dried out onshore shadow banking by introducing a financial transactions tax, as often discussed by French and German policymakers. However, this would likely shift financial activity offshore, providing profit opportunities for the bloc's periphery which supplies large amounts of offshore Euros, hesitantly backstopped by the ECB's swap network.

Establishing and maintaining competing blocs requires some political clout. The world may follow this trajectory if the US further withdraws from stabilizing the international system and a weakened Fed can no longer sustain its network of unlimited swap lines for political reasons, while the US competitors fix their structural problems. The EU would find a monetary architecture that overcomes the Eurozone's current design flaws, and China's state-driven mercantilism would succeed in internationalizing the Renminbi and restoring trust into its financial system.

The mid-19th century is a precedent for a setup of the international monetary system structured around competing monetary blocs when the British gold bloc stood opposite the US and German-dominated silver bloc and the French bimetallic bloc (Flandreau, Reference Flandreau2003). Further examples for such a setup of the international monetary system are the Cold War world and the division in a liberal, a fascist and a communist bloc in the 1930s and 40s.

4.3 Trajectory III: international monetary federation

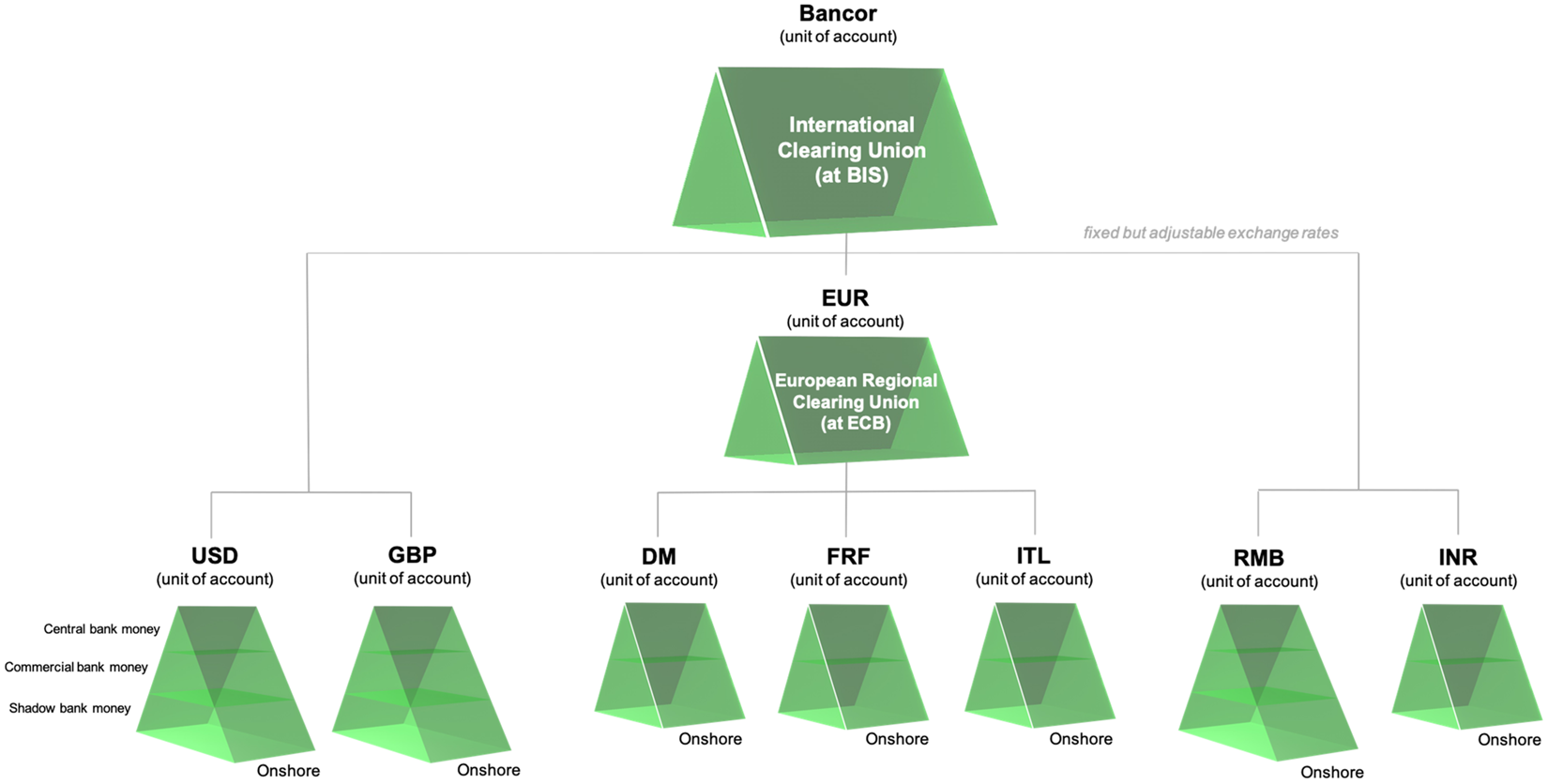

In the trajectory that leads to an international monetary federation, the Offshore US-Dollar System collapses in a cataclysmic financial crisis that puts an end to financial globalization. To compensate for the default, the international community has been able to agree on joint emergency measures and a multilateral public monetary infrastructure with fixed but adjustable exchange rates. This is a world of financial federalization.

At the top of the international hierarchy stands no longer a state, but an international organization – the BIS (see Figure 7). The BIS administers the international payments system, which is organized between national central banks, and functions as international clearing union (ICU) that is able to create genuine international credit money using its own unit of account. Reminiscent of the Keynes Plan for the Bretton Woods conference (Keynes, Reference Keynes1944), we call it ‘Bancor’, without implying that this trajectory sketches an identical proposal. The national monetary jurisdictions are located on the same hierarchical level. In addition, some states have formed regional clearing unions (RCUs) that connect them to the ICU. The Eurozone becomes a European RCU, whereby EU members have re-introduced national currencies, but kept the EUR as the RCU's unit of account.

Figure 7. International monetary federation. BIS, Bank for International Settlements; EUR, Euro; ECB, European Central Bank; USD, US-Dollar; GBP, British pound; DM, Deutsche Mark; FRF, French franc; ITL, Italian lira; RMB, Chinese renminbi; INR, Indian rupees. © 2020 Steffen Murau (CC-BY).

The Federation reminds in some respects of the Bretton Woods System that avoids the destabilizing gold base and responds to the demand that no longer the unit of account of a state should be the basis for international money but that of a ‘neutral’ institution. With the BIS, it has a bank in the apex with a fully elastic balance sheet, in contrast to the IMF that is a fund. The prevalence of Bancor overcomes the legal discrepancy between a state's decision-making and monetary area, and closes the legal offshore spaces. Hence, offshore money creation is fully abrogated. Individual states have received more autonomy to organize their onshore monetary systems. Some have opted to keep shadow money in place; others implement stricter regulation without shadow money.

Prerequisite for this trajectory is an endogenous implosion of the Offshore US-Dollar System without the Fed acting as a global backstop as its swap line network fails. This may happen for political reasons: An America First mindset does not align with protecting international financial stability as a global public good.

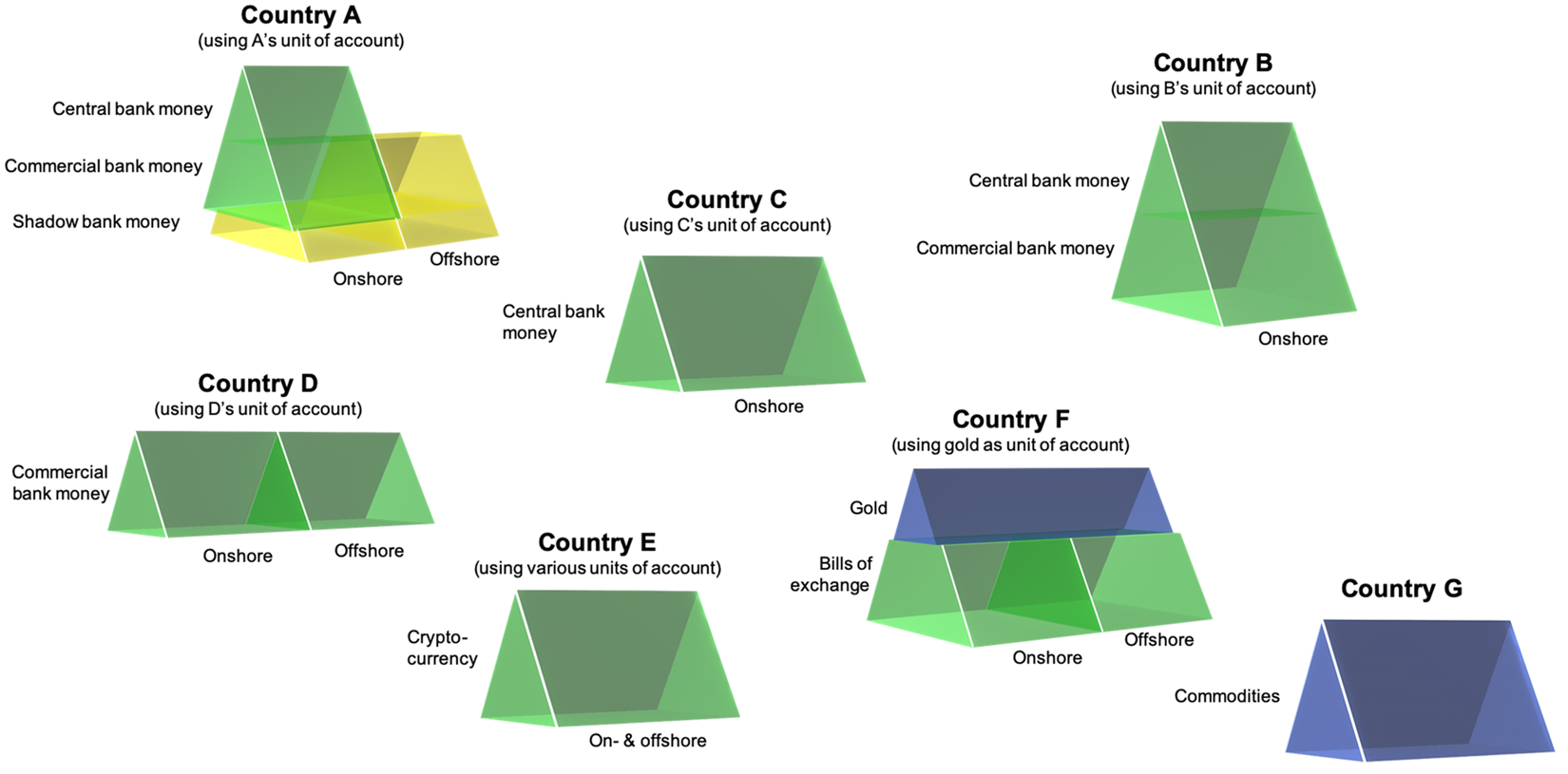

4.4 Trajectory IV: international monetary anarchy

In the trajectory that leads to an international monetary anarchy, the Offshore US-Dollar System has been hit by a cataclysmic financial crisis, too. This time, however, no coordinated international political response emerged. In consequence, the international monetary system's hierarchical structure is replaced by a non-system without apparent hierarchical order. International trade and financial transactions largely come to a halt. Financial globalization has given way to financial disintegration.

States follow their very own strategies to deal with the anarchic setting. Convertibility between different units of account can no longer be taken for granted. A clear exchange rate regime is absent. Money creation is predominantly shifted back onshore, yet some versions of offshore money remain in place.

Figure 8 depicts some of these strategies, without pointing to specific actual states and units of account. One group of states sticks to versions of the credit money system. Country A continues with a system similar to today, but with a strongly reduced shadow money and offshore component, while swap lines have broken down. Country B has resorted to a highly regulated onshore system with only central and commercial bank money as in the 1950s. Country C adopts a fully public system that exists exclusively onshore, Country D pushes a fully private banking system with a potentially strong offshore component. Another group is bolder and experiments beyond established credit money systems. Country E has introduced a pure cryptocurrency system, Country F a pre-modern gold cum bills of the exchange system, whilst Country G has resorted to abandoning money in general and becoming a barter economy.

Figure 8. International monetary anarchy. © 2020 Steffen Murau (CC-BY).

Situations of monetary anarchy occurred historically after major wars and may also be perceived as Hayek's utopia of currency competition (Hayek, Reference Hayek1976). However, such an arrangement would likely be merely a transitory stage before a more stable systemic structure evolves. Fundamental design alternatives such as a global cryptocurrency (Davidson et al., Reference Davidson, De Filippi and Potts2018) or a private global digital currency now have a chance to rise to systemic importance. In the logic of our trajectories, such outcome is only possible if the network externality of the Offshore US-Dollar System is overcome due to an endogenous implosion of the existing system and no concerted immediate political response.

5. Conclusion

The article has developed a conceptual framework to analyse the international monetary system in the age of financial globalization. We have sketched the institutional evolution from the Bretton Woods System to today's global Offshore US-Dollar System. Subsequently, we have presented four possible trajectories for its future evolution which depict possible setups of the system by 2040. These are not meant to be exact predictions, normative evaluations or institutional blueprints. Rather, they are extrapolations of existing trends into the future to show what the outcome of different possible trajectories could look like.

Our analysis implies that a continued USD hegemony with financial globalization is not a no-brainer. The space of possibilities is vast, and alternate evolutionary paths are possible. With the discrepancy of the political decision-making area and the global scope of the monetary system, we do not expect that policymakers have the clout to bring about profound changes of the system while it functions smoothly, only changes within the system (Trajectory II). However, due to the inherent instability of credit money, the next crisis is only a matter of time. An endogenous implosion of the global credit money system could be the critical juncture that opens up new evolutionary paths such as those towards federalization (Trajectory III) or disintegration (Trajectory IV).

Acknowledgements

This article would not have seen the light of day without the support of a great number of people. We are deeply grateful to Yulia Elupova of Studio Infografika Moscow for assistance in developing the figures and Yaroslav Maltsev for excellent research assistance. We wish to thank the research group Systemic Risks at the Institute for Advanced Sustainability Studies (IASS) Potsdam led by Pia-Johanna Schweizer and Ortwin Renn. Kathleen Molony at the Weatherhead Center for International Affairs of Harvard University as well as Kevin Gallagher and William Kring at the Global Development Policy Center at Boston University have helped our research in a multitude of ways. For invaluable feedback that we received in various forms and on multiple occasions, we express gratitude to Stefano Battiston, Michael Beggs, Andrea Binder, Dorothee Bohle, Benjamin Braun, Ben Clift, Ann E. Davis, Christine Desan, Lorenza Belinda Fontana, Daniela Gabor, Farsan Ghassim, Jean Grosdidier, Andrei Guter-Sandu, Yakov Feygin, Jeffry Frieden, Eckehard Häberle, Harald Hagemann, Iain Hardie, Geoffrey Hodgson, Torben Iversen, Carlo Jaeger, Casey Kearney, Arie Krampf, Jürgen Kromphardt, Elizaveta Kuznetsova, Hélène de Largentaye, Armand de Largentaye, Sylvia Maxfield, Perry Mehrling, Anastasia Nesvetailova, Manfred Nitsch, Stefano Pagliari, Fabian Pape, Tobias Pforr, Zoltan Pozsar, Pia Raffler, Aditi Sahasrabuddhe, Maria Schweinberger, Stefano Sgambati, Alexis Stenfors, Harald Stieber, Céline Tcheng, Matthias Thiemann, Geoffrey Underhill, Leanne Ussher, Bas van Bavel, Jens van ‘t Klooster and Fabian Winkler. Moreover, the article is informed by background talks with central bankers and financial market practitioners who have to remain anonymous. Finally, the article has greatly benefited from the input of three anonymous reviewers. All remaining errors are entirely our own.

Financial support

This article has been part of the Integrated Project DOLFINS (‘Distributed Global Financial Systems for Society’), supported by the European Union's Horizon 2020 research and innovation programme [grant agreement number: 640772 – DOLFINS – H2020-FETPROACT-2014]. Moreover, Steffen Murau gratefully acknowledges financial support by the German Academic Exchange Service (DAAD) for his fellowship at the Weatherhead Center for International Affairs of Harvard University and by Deutsche Forschungsgemeinschaft (DFG) for his fellowship at the Global Development Policy Center of Boston University.

Open access

Open access