INTRODUCTION

Corporate philanthropy has received increasing scholarly attention in recent years (e.g., Jeong & Kim, Reference Jeong and Kim2019; Seo, Luo, & Kaul, Reference Seo, Luo and Kaul2021). Several studies have examined the different factors that influence corporate philanthropy (e.g., Atkinson & Galaskiewicz, Reference Atkinson and Galaskiewicz1988; Marquis & Lee, Reference Marquis and Lee2013), and one stream of research has sought to understand the role of sudden events in firms’ engagement in philanthropic activities (Luo, Zhang, & Marquis, Reference Luo, Zhang and Marquis2016; Shu & Wong, Reference Shu and Wong2018). That work has generally focused on the short-term effects of sudden events on corporate philanthropy during or immediately after the event. For example, Zhang and Luo (Reference Zhang and Luo2013) and Luo and other scholars (Luo et al., Reference Luo, Zhang and Marquis2016) have examined firms’ responses to internet activism within two months after an event. Tilcsik and Marquis (Reference Tilcsik and Marquis2013) also study the post-event impact of sudden events over a longer period of a few years although they focus on the effects of different types of mega-events on corporate-community relations. Considering post-event effects, the authors suggest that a mega-event could not have long-term, persistent effects because it brings only minimal change in the social structure and inter-organizational relationships.

A sudden event can, however, alter the social structure and institutional foundations of the society in which a firm operates (Lampel & Meyer, Reference Lampel and Meyer2008; Meyer, Reference Meyer1982; Meyer, Gaba, & Colwell, Reference Meyer, Gaba and Colwell2005). It may result in fundamental changes in social norms and attitudes and thus exert persistent influence on firms’ philanthropic behavior. Such potential for a long-term, persistent effects of a sudden event has not been adequately explored in previous studies.

This study was designed to examine the long-term impact of a sudden natural disaster (an earthquake) seeking to understand the conditions under which its impacts are more likely to persist. Unlike the work of Tilcsik and Marquis (Reference Tilcsik and Marquis2013) whose study was set in a developed economy (the US), our study examines the impacts in China, an emerging market with under-developed institutions. In the presence of well-developed institutions, it may be difficult for a sudden event to have a persistent effect; but in an economy like China's where some institutions are less well-established and still evolving (e.g., Chua, Huang, & Jin, Reference Chua, Huang and Jin2019; Huang, Reference Huang2017; Huang, Geng, & Wang, Reference Huang, Geng and Wang2017), a disaster can possibly reshape the institutional structure with more persistent impacts.

This study applied Polanyi's double movement perspective (Polanyi, [1944] Reference Polanyi2001) to examine how a sudden, large-scale, catastrophic event can have a persistent effect on firms’ corporate philanthropy. The main premise of the double movement perspective is that in market societies there is a laissez-faire orientation which may favor economic efficiency over social relations and morality. In such a ‘disembedded’ economy, economic activities are disembedded from society and predominate over other activities. While promoting productivity and economic prosperity, according to the double movement perspective, such an economy inevitably provokes a countermovement opposing marketization and toward a more embedded economy that places greater emphasis on the preservation of nature, social relations, and morality.

Building on this perspective, when a countermovement against a disembedded economy is emerging, a sudden catastrophe is likely to produce not only a significant short-term effect on corporate behavior (Luo et al., Reference Luo, Zhang and Marquis2016; Tilcsik & Marquis, Reference Tilcsik and Marquis2013), but also an enduring effect by making the negative social impacts of a disembedded economy salient, intensifying the countermovement. In many societies, corporate philanthropy is an important mechanism that helps provide social protections for labor, nature, and other public goods, the key aspirations of the countermovement. Accordingly, to the extent that a disaster intensifies a countermovement against the disembedded economy and draws society's attention to corporate philanthropy, there is likely to be a long-term, persistent effect on corporate giving. That is, firms’ philanthropic donations are likely to continue at a level higher than they would otherwise have been, even long after the sudden event.

The strength of any such effect on corporate philanthropy and its persistence is likely to depend on the extent to which a particular firm is perceived as potentially contributing to social problems. Firms which, for example, have a high level of intra-firm income disparity or operate in socially contested industries are more likely to be perceived as causing society's problems. They will then face greater countermovement pressure than other firms and thus are more likely to maintain an increased level of corporate philanthropy after a sudden event. In addition, research has documented the important role of social activists in facilitating countermovements (Levien, Reference Levien2007; Polanyi, [1944] Reference Polanyi2001). The number of social foundations in a region may correlate with the social pressure imposed on firms, thus serving as another boundary condition. These theoretical arguments were tested using empirical data from China; and the sudden event was the 2008 Wenchuan earthquake in Sichuan Province (Zhang & Luo, Reference Zhang and Luo2013). It was one of the most severe earthquakes China has ever experienced.

The study makes the following key contributions. First, there have been many studies examining the impact of major events like the Olympic Games and political developments on corporate philanthropy (Muller & Kräussl, Reference Muller and Kräussl2011; Shu & Wong, Reference Shu and Wong2018; Tilcsik & Marquis, Reference Tilcsik and Marquis2013), but few of them have examined the long-term effects of the events in a systematic way. By testing the double movement perspective with a sudden event, this study provides a new perspective on how long-term changes in corporate philanthropy come about.

Second, its findings extend scholarly understanding of the double movement perspective (Polanyi, [1944] Reference Polanyi2001). While research in this area has focused on countermovements such as government intervention (Dale, Reference Dale2012; Watkins, Reference Watkins2017), NGO activity (Bandelj, Shorette, & Sowers, Reference Bandelj, Shorette and Sowers2011; Levien, Reference Levien2007), or media debates (Reisman, Reference Reisman2019), this study examined philanthropic behavior as firm responses to a countermovement. In doing so it has established a strong, previously undocumented connection between the double movement perspective and corporate philanthropy. The findings further extend this perspective by identifying several contingencies – firm-level pay dispersion, firms’ affiliation with socially contested industries, and the presence of social foundations in a region – that can affect the magnitude and consequence of the countermovement.

THEORETICAL BACKGROUND AND HYPOTHESES

The Double Movement Perspective

Whether an economy is considered embedded or disembedded forms the basic premise of the double movement perspective (Polanyi, [1944] Reference Polanyi2001). In an embedded economy, economic activities and exchanges are embedded in social relationships. Non-economic factors such as institutions, politics, traditions, community, and religion shape the society in which economic activities are embedded. In such a context, morality, justice, and obligations to charity play important roles (Arnold, Reference Arnold2001; Booth, Reference Booth1993, Reference Booth1994; Scott, Reference Scott1976). Feudal societies with serfdom are an example of such an economy. A disembedded economy, by contrast, is characterized by a self-regulating market, atomization, and commodification. Instead of social relationships, market rules and efficiency dominate economic activity. In a disembedded economy, market transactions and contracts driven by self-interest heavily influence the relationships among firms and individuals. Labor, land, and natural resources are commercialized. Social relations play a smaller role. Capitalist societies are typical examples.

Although disembedded economies have been dominating since the 19th century, the double movement perspective suggests that disembedding forces commodify humans and nature, eventually leading to various social problems such as social disparities and environmental destruction which threaten the environment and human survival – even the functioning of the market itself, indeed (Booth, Reference Booth1993, Reference Booth1994; Polanyi, [1944] Reference Polanyi2001; Scott, Reference Scott1976). The prediction is that eventually the entire society, especially individuals who have been deprived of social and economic security by marketization, will spontaneously reflect on social problems and collectively initiate a countermovement aimed at protecting man and nature and promoting social equity and moral behavior.

Recent research has examined the explanatory power of the double movement perspective in both national and international contexts. One stream of work has focused on anti-globalization movements such as regionalization and the institutional solutions advocated by international society (Birchfield, Reference Birchfield1999; Evans, Reference Evans2000, Reference Evans, Janoski, Alford, Hicks and Schwartz2005, Reference Evans2008). Levien and Paret (Reference Levien and Paret2012) have documented increased tendencies toward re-embedding globally in the 1990s motivated by discontent with market reforms of the day. Another stream of research has focused on national countermovements. Levien, in his study of India's National Alliance of People's Movements, has elaborated the efforts of a national alliance to resist globalization, liberalization, and privatization in India in the 1990s. Despite these diverse applications of the double movement perspective, there has been only limited scholarly work applying it to corporations, which are increasingly becoming the targets of global and national countermovements opposing marketization. For example, Reisman (Reference Reisman2019) shows media-initiated debates about the wisdom of using water, a public good, for water-intensive almond production in California. These debates led to the formation of a countermovement targeting wealthy farming corporations that became rich from exploiting water resources in this way.

Countermovements in China

Historically, China has long been an embedded economy with only weak market-orientation. However, China started becoming more disembedded in the early 1980s, and since then Chinese businesses and society have generally been guided more by economic rather than social considerations (Beamish & Bapuji, Reference Beamish and Bapuji2008; Luo, Reference Luo2006). With that orientation, Chinese firms have developed rapidly for three decades. Corporations have become more important, with private firms in particular growing rapidly. Figure 1 shows the trend in the number of large, private industrial firms as a proportion of the total number of firms since 1998.[1]

Figure 1. The proportion of private firms among Chinese industrial firms per year

At the same time, income inequality, production insecurity, and environmental pollution have also increased, which has led to increasing public discontent (Wang, Reference Wang2008; Yang, Reference Yang2006). Such grievances and society's reflections on these social problems build momentum for a self-protective countermovement against disembedding forces (Escher, Schneider, & Ye, Reference Escher, Schneider and Ye2018; Wang, Reference Wang2010). As a result, since the late 1990s, there has been a growing countermovement pressing the Chinese government to take measures to address social problems and promote greater equity in society, including, for example, enacting labor laws which better protect the workforce (Wang, Reference Wang2008). Meanwhile, it is increasingly recognized that business corporations are the primary sources of these social problems. For example, real estate firms in China are believed to have contributed significantly to the increase in income disparity due to their extremely high profits and excessive salaries (Luo et al., Reference Luo, Zhang and Marquis2016). Massive greenhouse gas emissions and vast consumption of non-renewable energy are attributed to firms’ profit-seeking (Wang, Wijen, & Heugens, Reference Wang, Wijen and Heugens2018). The public has come to realize that in the 21st century the most serious environmental pollution accidents have always been associated with business corporations (Sohu, 2017). The countermovement, therefore, increasingly called on firms to address these problems.

One corporate response has been philanthropy. Corporate philanthropy can be a straightforward and appropriate way to address social problems. For example, corporate donations to foundations supporting education in poor villages can reduce income disparity arising from unequal educational opportunities. Supporting foundations that aim to protect the environment or wild animals is another example. Compared with other social entities, corporations have abundant resources and management skills, and their philanthropy can supplement government spending (Porter & Kramer, Reference Porter and Kramer2011).

Nevertheless, before 2008, the emerging countermovement had little discernable impact on corporations’ social responsibility in general or on corporate philanthropy in particular. Before 1980s, China experienced a period called planned economy during which governments, state-owned enterprises (SOEs) or collectively owned enterprises, and brigades in the commune provide social protections for individuals (Wang, Reference Wang2008). Such an economy emphasizes equity and security. Since 1980, as then the Chinese leader Xiaoping Deng noted, economic development is an absolute principle (Zhang, Reference Zhang2004). Since then, the Chinese society has thus emphasized economic development; other social demands such as equity, employment, labor rights, medical care, and environment can be secondary or even sacrificed (Wang, Reference Wang2010). Private firms started to emerge and grow, and the mandate of such firms was purely on pursuing economic development, and there was little institutional or social pressure for these firms to perform social roles. While other organizations such as SOEs still carried traditional duty for social protection, such pressure was substantially weakened with the fast market development and governments’ gradual exit from private economy in Chinese society.

Therefore, during the period from 1980 to 2008, there was little clear and consistent motivation for pro-social behavior, as both social regulation and institutional pressure were generally imperceptible (Gao, Reference Gao2011; Liu & Zheng, Reference Liu and Zheng2009). For example, in 2005, only five firms reported donating more than ¥50 million to charitable causes (SINA, 2005). While there were criticisms at the time (Yuan, Reference Yuan2003), not too much attention was paid to corporate philanthropy. Before the 2008 Wenchuan earthquake, corporate philanthropy received scant media coverage (Figure 2). The descriptive statistics in Figure 2 were compiled by searching for news articles containing the terms ‘corporate philanthropy’ or ‘corporate donation’ using Baidu.com, China's most popular search engine. The 2008 Wenchuan earthquake stimulated significant interest in corporate philanthropy, as the figure shows, and that media interest persisted.

Figure 2. The number of Chinese media reports containing the key words ‘corporate philanthropy’ or ‘corporate donation’ in each year[12]

The Wenchuan Earthquake and Corporate Philanthropy

The Wenchuan earthquake struck on May 12, 2008. It was China's strongest earthquake since the 1970s. By July, the Ministry of Civil Affairs had officially reported 69,197 deaths, 374,176 injured persons, and 18,222 ‘missing’. More than 4.8 million people became homeless (Hooker, Reference Hooker2008). The government designated May 19th to the 21st as national days of mourning.

The earthquake intensified a countermovement toward re-embedding of the economy, including toward increased corporate philanthropy. The sudden disaster directed society's attention to corporate philanthropy, as the heavy loss of life stimulated public benevolence and attention to the victims and relieving their distress. Major media channels set the tone by promoting the heroic behavior involved and praising those efforts to help. Almost all the popular Chinese news websites such as www.sina.com.cn, www.qq.com, www.xinhuanet.com, www.people.cn, www.sohu.com, www.cctv.com, www.netease.com, www.ifeng.com, and www.china.com.cn devoted coverage to donations from various sources (Luo et al., Reference Luo, Zhang and Marquis2016). Any generous donation attracted a great deal of media and thus public attention, one of the major forces of the countermovement toward re-embedding (Polanyi, [1944] Reference Polanyi2001). For example, Wanglaoji, a then relatively small herbal tea company, donated ¥100 million for disaster relief. The company became famous overnight and received enthusiastic praise from the public. The media even invented slogans such as ‘Chinese people drink only Wanglaoji’ and ‘Donate 100 million if you donate; drink Wanglaoji if you drink’. Philanthropy by Chinese firms took the center stage for the first time since China's marketization, capturing the attention of the public and media, which was reflected in the broad media coverage of the topic (refer to Figure 2 for the sudden jump in media coverage).

The sudden earthquake further intensified the countermovement by increasing the tension between forces encouraging disembedding and their opponents. This was clearly shown when some firms made donations that the public considered insufficient (Luo et al., Reference Luo, Zhang and Marquis2016; Zhang & Luo, Reference Zhang and Luo2013). When those firms’ managers tried to justify meagre donations by emphasizing their focus on market principles, especially their responsibility to shareholders, they found themselves facing strong public and media disapproval. For example, Shanda Group, a famous game company, was criticized for the small amount of its donation (Baidu Tieba, 2008). Online discussions had statements such as, ‘I am quite disappointed in these rich companies’ and ‘You earned a lot of money from us but donated little. You should be ashamed of this’. It further prompted public dissatisfaction with firms’ wealth in general, which was thought to be attributable, at least in part, to the exploitation of natural resources and human labor (Luo et al., Reference Luo, Zhang and Marquis2016; Zhang & Luo, Reference Zhang and Luo2013). Just as stretching an elastic band generates a rebound, disembedded behavior at a time of high expectation for the opposite increased tension between the movement and countermovement and resulted in a rebound in the opposite direction toward embedding (Polanyi, [1944] Reference Polanyi2001; Reisman, Reference Reisman2019).

And the effect persisted. Consistent with the double movement perspective's view of ‘enlightened’ parties as the primary drivers of countermovements (Polanyi, [1944] Reference Polanyi2001), the responses to the earthquake promoted enlightenment of the public, media, government, government agencies, and industry associations about social issues and firms’ social responsibilities. That led to a long-term effect of the earthquake in terms of changing firm's attitudes toward corporate social responsibility (CSR) in general and corporate philanthropy in particular.

There is evidence of a persistent change in public attitudes toward the countermovement, social issues, social protections, and CSR after 2008. The China Environment Yearbook reported a persistent increase in the number of environmental complaints from the public after 2008 (see Figure 3a).[2] The public's online comments related to ‘common prosperity’ – a social goal signifying economic prosperity coupled with greater social equality – in nine major online forums in China such as guba.eastmoney.com, tieba.baidu.com, bbs.tianya.cn, www.zhihu.com, www.weibo.com, www.douban.com, www.mopxz.com, bbs.hupu.com, and www.9kd.com also increased markedly after 2008 and stayed high (see Figure 3b). A similar pattern was evident for the search term ‘environmental protection’ (Figure 3c). The public was initiating more discussion of such re-embedding social topics. Another indicator is the number of books in the national library related to CSR. Figure 3d shows that it has increased steadily after 2008, again suggesting that society has been paying more attention to CSR.[3] Indeed, public and media attention has persisted long after the earthquake (Figure 2).

Figure 3. (a) The number of environment-related complaints from the public per year (b) The number of comments related to ‘common prosperity’ in major online forums per year (c) The number of comments related to ‘environmental protection’ in major online forums per year (d) CSR-related books in China's national library per year

Figures 4a–4d provide evidence that the Chinese government and government agencies have also been paying more attention to the countermovement, social issues, social protection, and CSR after 2008. As Figures 4a and 4b make it clear, there has been a persistent increase in the number of central government policies mentioning ‘common prosperity’ or ‘environmental protection’ after 2008.[4] Figure 4c shows a similar persistent increase in the number of central government policies mentioning CSR. In December 2008, the Shanghai and Shenzhen stock exchanges announced that all firms included in their Corporate Governance Index or Top 100 index would be required to issue reports on their corporate responsibility efforts along with their annual reports. These reports should disclose activities related to employee protection, environmental protection, consumer protection, community relationships, and other social welfare activities such as philanthropy (Marquis & Qian, Reference Marquis and Qian2013). In addition, data from China Stock Market and Accounting Research (CSMAR) database presented in Figure 4d show a persistent increase in Chinese banks’ ‘green’ lending (i.e., loans to environment protection or renewable energy-related projects) after 2008. Indeed, by 2021, such lending by Chinese banks was among the world's most plentiful (Baidu Baike, 2022). It is evident that the banks too are critical drivers encouraging firms to initiate more environment-friendly projects, and in China much bank lending is government-directed.

Figure 4. (a) The number of central government policies mentioning ‘common prosperity’ per year (b) The number of central government policies mentioning ‘environmental protection’ per year (c) The number of central government policies mentioning CSR per year (d) The ‘green’ lending of Chinese banks per year

The media and industry associations have also advocated CSR regularly since 2008. Chengdu's government and the Nanfang Daily held China's first CSR conference not long after the earthquake, where sustainable development and the responsibilities of Chinese firms were discussed (SINA, 2009). Such discussions have continued until today. In addition, the media and industry associations have since then taken to issuing annual social responsibility reports covering China's automobile industry, generating normative pressure for automobile firms to improve their social performance (Liu, Reference Liu2009). Similar norms have formed in other industries such as real estate and petrochemicals (Cao, Reference Cao2011; Sun, Reference Sun2019), all encouraging greater business contributions toward social goals and long-term sustainability and accelerating the increase in corporate philanthropy.

Once formed, these regulations, norms, attitudes, and practices are likely to be persistent and difficult to reverse (DiMaggio & Powell, Reference DiMaggio and Powell1983; Huang et al., Reference Huang, Geng and Wang2017; Meyer & Rowan, Reference Meyer and Rowan1977; Scott, Reference Scott2001). As a result, individual firms have also changed their attitudes toward CSR after 2008. As Figures 5a and 5b show, the percentage of firms issuing either a mandatory or a voluntary CSR report increased substantially after 2008, and the pattern has persisted. As well, many firms’ reports have become more substantial rather than symbolic. An increasing percentage of reports conform to the standards of the Global Reporting Initiative (GRI) (Figure 5c).[5] CSR reports meeting strict GRI's standards can be regarded as of good quality.

Figure 5. (a) The proportion of firms having issued separate CSR reports per year (b) The proportion of firms having issued separate CSR reports (mandatory vs. voluntary) (c) The proportion of firms having issued separate CSR reports based on GRI standards

In summary, consistent with the double movement perspective, the significant increase in corporate philanthropy after the Wenchuan earthquake was a result of increased societal attention to corporate philanthropy and intensification of a countermovement in China society. That intensification has substantially changed the social and institutional context and imposed persistent influence on firms’ behavior. Therefore, we hypothesize:

Hypothesis 1a (H1a): Philanthropic donations from Chinese firms will increase after the Wenchuan earthquake.

Hypothesis 1b (H1b): The increase in philanthropic donations after the Wenchuan earthquake will have persisted.

Although business corporations are often considered the major source of social problems in a disembedded economy and thus face pressure to provide solutions, the level of pressure experienced by different firms varies. As a result, a firm's philanthropic contributions would be expected to depend on both the extent to which the firm is perceived as contributing to social problems and on the level of pressure the firm feels from social activists. Consider, for example, the income gap between the rich and poor in China or, for another example, environmental degradation (Luo et al., Reference Luo, Zhang and Marquis2016; Wang et al., Reference Wang, Wijen and Heugens2018). If a firm is perceived as contributing to the income gap and/or environmental degradation, that should lead to social discontent and stronger pressure for the firm to engage in (and publicize) philanthropic donations. Accordingly, we examine the intra-firm pay dispersion and whether a firm operates in socially contested industries (e.g., highly polluting industry). Then, for the pressure from social activists, we examine the number of social foundations in a region in which firms operate because pressure for corporate philanthropy from countermovement may be influenced by the presence of community foundations across different geographies (Marquis, Glynn, & Davis, Reference Marquis, Glynn and Davis2007).

Intra-Firm Pay Dispersion

Pay dispersion refers to the difference in rates of pay between a firm's top managers and its other employees (Connelly, Haynes, Tihanyi, Gamache, & Devers, Reference Connelly, Haynes, Tihanyi, Gamache and Devers2016; Shaw, Reference Shaw2014). Previous research on this topic has generally focused on how pay dispersion might affect employees’ motivation and productivity. On the one hand, from the tournament perspective, pay dispersion offers the possibility of big raises, which should motivate better efficiency and performance (Lazear, Reference Lazear1995; Lazear & Rosen, Reference Lazear and Rosen1981). But from the equity perspective (Adams, Reference Adams1963), it can generate perceptions of relative deprivation (Deutsch, Reference Deutsch1985). That may reduce motivation, effort, and cooperation (Cowherd & Levine, Reference Cowherd and Levine1992) and generate antagonistic social relationships (Bloom & Michel, Reference Bloom and Michel2002) and resentment (Siegel & Hambrick, Reference Siegel and Hambrick2005).

It is said that in a disembedded economy only the fittest survive and the unfit are sidelined (Polanyi, Reference Polanyi1947; Silver & Arrighi, Reference Silver and Arrighi2003; Watkins, Reference Watkins2017). To the extent that large pay dispersion in a firm fosters internal competition among workers (Connelly et al., Reference Connelly, Haynes, Tihanyi, Gamache and Devers2016; Grund & Westergaard-Nielsen, Reference Grund and Westergaard-Nielsen2008), the more efficient get more pay and promotions while the least productive are, in principle, paid much less or even weeded out (Lazear, Reference Lazear1999). That enlarges the income gap within the firm and at the society level. Traditional Chinese culture and communist value (Marx, Reference Marx1976) encourage some Chinese people to believe that capitalism exploits the labor force for profit maximization. Indeed, journalists have frequently cautioned against abnormally large-income disparity within a firm as a sign of social injustice (Lu, Reference Lu2004). Similarly, Chinese popular internet forums such as Tianya interpret a large pay gap between top managers and other employees as indicating a firm's exploitation of its employees (Kaijiacaijing, 2022).

Before the earthquake, when the countermovement was not yet strong, negative views of large pay gaps were not often expressed. Even when they were, criticism did not penetrate the business domain or inspire social action. But after the earthquake, the re-embedding countermovement became much stronger and the public and media started to pay more attention to and react more to the economy's disembeddedness, placing greater pressure on firms for responsible social conduct. A firm with a large pay difference between C-suite managers and lower-level employees came to be considered as contributing to the unfair income gap, inviting criticism from the public and media (Bednar, Reference Bednar2012; He & Fang, Reference He and Fang2016). Reducing intra-firm pay dispersion could of course have been the direct response, but that is often challenging and rather costly to implement. It would disrupt employees’ rather routinized career paths and compensation policies and firms still have to maintain competitive compensation levels in order to attract talented managers (Connelly et al., Reference Connelly, Haynes, Tihanyi, Gamache and Devers2016; Grund & Westergaard-Nielsen, Reference Grund and Westergaard-Nielsen2008). Instead, making philanthropic donations may offer a more visible alternative. Thus,

Hypothesis 2 (H2): Firms with high intra-firm pay dispersion will increase their philanthropic donations more after the Wenchuan earthquake than firms with low intra-firm pay dispersion.

Firms Operating in Socially Contested Industries

In Western contexts, the term ‘contested’ has come to be applied to industries such as alcoholic beverages, firearms, mining, oil and petrochemicals, furs, and tobacco products. Firms operating in such industries tend to be regarded as exacerbating health and safety problems and/or pollution of the environment (Durand & Vergne, Reference Durand and Vergne2015; Koh, Qian, & Wang, Reference Koh, Qian and Wang2014). In the Chinese context, large-income gaps and environmental deterioration are two important social issues so firms with a large income gap (He & Fang, Reference He and Fang2016; Luo et al., Reference Luo, Zhang and Marquis2016) and/or causing serious environmental problems such as exhausted land, devastated forests, the extinction of species, or regional climate change (Foster, Reference Foster2011; Humphrey & Sneath, Reference Humphrey and Sneath1999; Wang et al., Reference Wang, Wijen and Heugens2018) would be analogous.

For example, rapid economic development in China has led to a boom in the real estate industry, and real estate firms and their executives are believed to have accumulated enormous fortunes (Luo et al., Reference Luo, Zhang and Marquis2016). In 2008, seven of China's ten richest people according to Forbes were real estate executives (Forbes, 2008). The finance industry has also drawn media and public attention for the high level of compensation of its managers (Sohu, 2006). And some industries in China might be classified as contested based on their influence on the natural environment (Boelens & Vos, Reference Boelens and Vos2012; Kull, Arnauld de Sartre, & Castro-Larrañaga, Reference Kull, Arnauld de Sartre and Castro-Larrañaga2015; Prudham, Reference Prudham2007). They too have received more attention in recent years, especially since 2008 (Wang et al., Reference Wang, Wijen and Heugens2018; Zheng & Shi, Reference Zheng and Shi2017). There have even been rallies and sit-ins to protest against polluting activities in some regions (Zheng, Kahn, Sun, & Luo, Reference Zheng, Kahn, Sun and Luo2014). In addition, the Chinese government has implemented new water pollution prevention and remediation policies since 2008[6], establishing a Ministry of Environmental Protection.[7] In 2011, the ministry issued its first report evaluating the environmental performance of publicly listed firms in the most polluting industries. It was accompanied by a blacklist of 40 firms (Liu, Reference Liu2011).

Compared with firms in other industries, those operating in socially contested industries are seen as having contributed more significantly to social problems. They have thus faced stronger pressure from the countermovement since the earthquake. As a result, such firms are more likely to have diverted resources to addressing social issues. But again, given the limitations and challenges involved in altering operations and switching to other industries, firms may find corporate philanthropy a viable and relatively visible technique for reducing countermovement pressure.

Hypothesis 3 (H3): Firms in socially contested industries will increase their philanthropic donations more after the Wenchuan earthquake than those in industries which are not socially contested.

Social Foundations in a Region

There is ample evidence that local communities can substantially influence organizations (Freeman & Audia, Reference Freeman and Audia2006). Religiosity in a community can, for example, influence local firms’ risk-taking (Hilary & Hui, Reference Hilary and Hui2009). Scholars have shown that local violence correlates with workplace aggression among employees (Dietz, Robinson, Folger, Baron, & Schulz, Reference Dietz, Robinson, Folger, Baron and Schulz2003). In the domain of corporate social behavior, Galaskiewicz (Reference Galaskiewicz1997) found that a firm's social ties with philanthropic leaders in the community lead to more corporate philanthropy. In addition, Tilcsik and Marquis (Reference Tilcsik and Marquis2013) have shown that sudden events in the community affect local corporate philanthropy through influencing local normative expectations.

A key local attribute which can affect corporate philanthropy is the social foundations operating there (Marquis et al., Reference Marquis, Glynn and Davis2007; Tilcsik & Marquis, Reference Tilcsik and Marquis2013). In Western societies, social foundations promote networking, acquainting the leaders of local non-profits with local corporate leaders. They may, for example, serve as board members in the same foundation. Such connections may facilitate corporate philanthropy (Galaskiewicz, Reference Galaskiewicz1997; Marquis et al., Reference Marquis, Glynn and Davis2007). Social foundations similarly connect firms and non-profits in China, but the foundations also often have their own philanthropic projects (Estes, Reference Estes1998; Lai, Zhu, Lin, & Spires, Reference Lai, Zhu, Lin and Spires2015). They raise funds from the government, individuals, and corporations and serve beneficiaries such as universities, hospitals, schools, and nature reserves. For example, the Song Qing Ling Foundation in Shanghai initiated a project supporting child education in poor regions of China in 2011 (Songqingling Foundation, 2011). Before 2003, most foundations in China were founded by the government and they served to extend government functions. Since 2004, regulatory changes have opened up the space for private foundations, which can be founded by individuals or firms (Chan & Lai, Reference Chan and Lai2018; Lai et al., Reference Lai, Zhu, Lin and Spires2015). Today about half of China's social foundations have government officials and/or corporate executives sitting on their boards, and such ties play an important role in their fund-raising activities (Johnson & Ni, Reference Johnson and Ni2015; Zhang, Wu, Chin, Yu, & Cai, Reference Zhang, Wu, Chin, Yu and Cai2020). While executives’ business ties can impose direct philanthropic pressure on a firm, political ties with the government can also promote corporate philanthropy. In China, government officers can be in a position to provide useful support for a local business in exchange for philanthropic donations.

The presence of social foundations in a region is likely to have enhanced the effect of the earthquake on corporate philanthropy. Before the earthquake, when the countermovement in the domain of corporate philanthropy was weak, so was the role of local social foundations. Even for firms connected to social foundations, there was little expectation of philanthropic acts. But with the countermovement much strengthened after the earthquake, foundations used their connections with corporate executives to press for more corporate philanthropy. Meanwhile, social foundations more actively sought to establish closer ties with business. This is evidenced by regulations on the transparency of connections between social foundations and firms issued by the Ministry of Civil Affairs in 2012 (Huang, Reference Huang2012). Overall, it is reasonable to anticipate that firms operating in regions with numerous social foundations faced stronger pressure for philanthropy after the earthquake and thus tended to donate more.

Hypothesis 4 (H4): Firms located in regions with more social foundations increased their philanthropic donations more after the Wenchuan earthquake than those in regions with fewer social foundations.

METHODS

Data

The hypotheses were tested using data on Chinese firms listed on the Shenzhen or Shanghai stock exchanges between 2001 and 2016. Information on their philanthropy, compensation patterns, financial performance, and other variables was collected from the CSMAR database.[8] The utility of the CSMAR database has been validated in prior studies (e.g., Fan, Wong, & Zhang, Reference Fan, Wong and Zhang2007; Jia, Huang, & Zhang, Reference Jia, Huang and Zhang2019). Information on industrial pollution was collected from the website of China's Ministry of Ecology and Environment. Information on social foundations was obtained from a database maintained by Chinese Research Data Services, which has been employed in recent scholarly work (Li, Yu, Mei, & Feng, Reference Li, Yu, Mei and Feng2021; Lv, Zhu, Chen, & Lan, Reference Lv, Zhu, Chen and Lan2021). This data was collected only for this project, not used previously in other studies. Meanwhile, as some of the variables were collected from existing databases such as CSMAR, there were some variables such as the typical firm-level variables (e.g., total asset, ROA, and financial leverage from CSMAR) and regional-level controls (e.g., marketization index from NERI) over certain years overlapping with those in previous publications (Wan, Xie, Li, & Jiang, Reference Wan, Xie, Li and Jiang2021).

The data covered a 15-year period – from seven years before (2001–2007) to eight years after (2009–2016) the Wenchuan earthquake. In the main analysis, 2008 was not included to minimize any effect of the dramatic increase in corporate philanthropy and noise during the year of the earthquake.[9] In addition, only firms founded before 2008 were considered, so each firm provided at least one year of observations before 2008 and one after. After matching, the resulting (unbalanced) panel dataset consisted of 1,341 firms and 12,543 firm-year observations.[10]

Empirical Strategy

In China, private (non-SOE) companies whose ultimate owner is not the state have developed rapidly since the market-oriented reforms of China's Open Door Policy initiated in 1978 (Li, Meng, Wang, & Zhou, Reference Li, Meng, Wang and Zhou2008). By 2006, private companies contributed to more than 65% of China's GDP and played a vital role in the economy (SINA, 2006). Private (non-SOE) firms are generally more market- and efficiency-oriented and profit-driven, consistent with the disembedding orientation. SOEs remain common and are quite different from private firms (Jia et al., Reference Jia, Huang and Zhang2019). Beyond economic and efficiency goals, SOEs need to support the state's political and social agenda. They are sometimes required to sacrifice profits in order to stabilize employment; they have a heavy tax load; and some of their strategic moves such as acquisitions need government approval (Greve & Zhang, Reference Greve and Zhang2017; Xia, Ma, Lu, & Yiu, Reference Xia, Ma, Lu and Yiu2014). SOEs, therefore, are not completely disembedded in the eyes of the public. That makes private firms more likely to be targeted by any countermovement advocating greater embedding. To test this statement, we analyzed the comments referring to ‘SOE and/or private firm, and disparity between the rich and the poor’ in major online forums. It is observed that the public tended to complain that private firms contribute to the disparity between the rich and poor and believe that SOEs help reduce such disparities. We conducted a similar analysis using ‘SOE and/or private firm, and environmental pollution’ and did not find any significantly different opinions between SOEs and private firms. In a similar analysis using ‘SOE and private firm’ as key terms, the comments showed that the public often associated SOEs with CSR topics while associating private firms with the discussions of efficiency. In sum, the above evidence lends further support to our arguments.

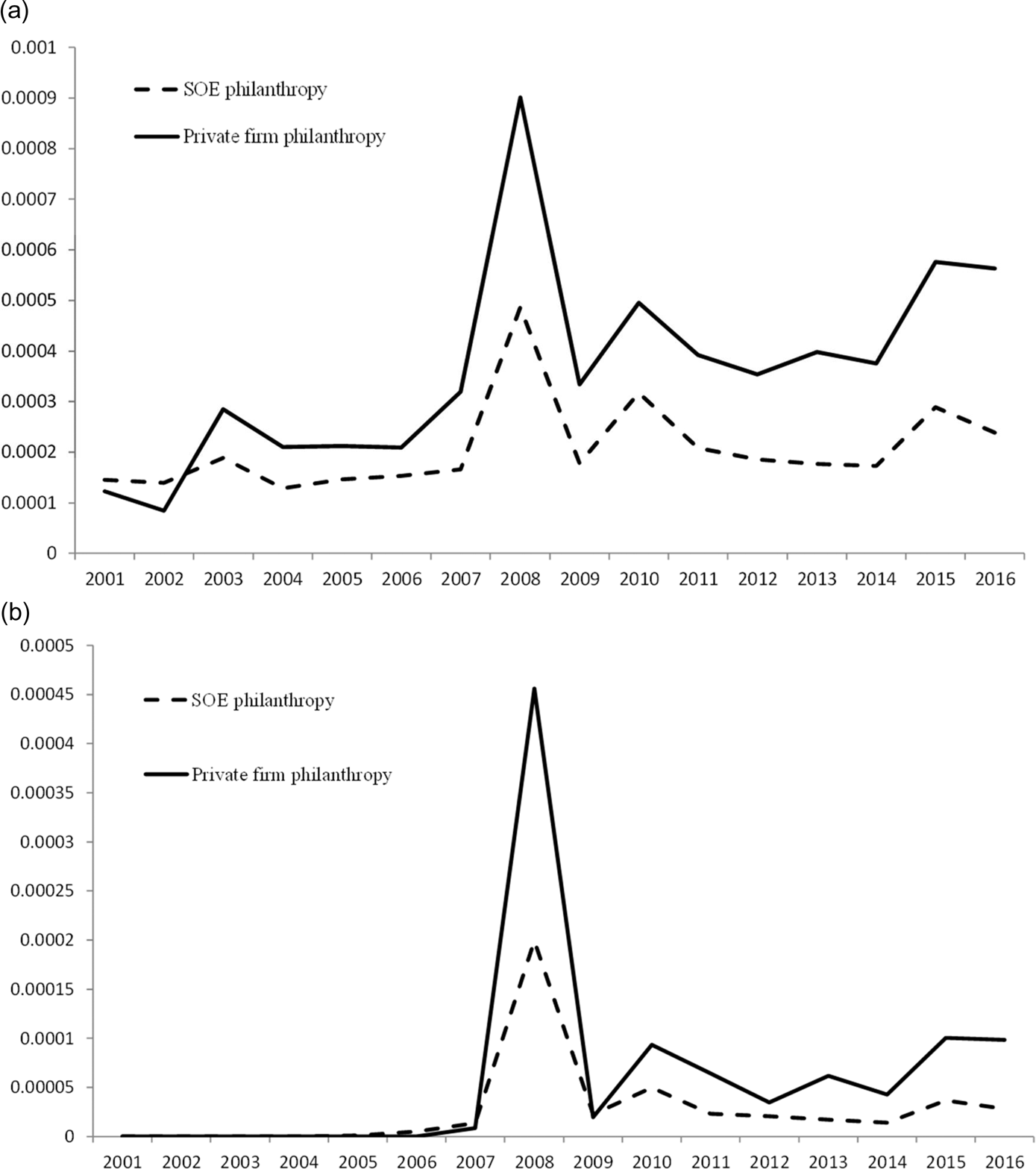

While both SOEs and private firms are affected by the earthquake, we expect private firms to be affected to a greater extent because SOEs attracted less pressure from the countermovement, which targeted primarily efficiency-oriented and profit-driven firms. Therefore, in testing the hypotheses, we take advantage of this difference: the philanthropy of SOEs is minimally affected by the earthquake compared with that of the private firms. Hence, we employ a difference-in-differences (DID) estimation approach using the affected private firms as the treatment group and the minimally affected SOEs as the control group. The DID approach is preferred to the conventional cross-sectional analysis because it allows better identification and estimation of causal relationships between the exogenous earthquake shock and corporate philanthropy over time (Huang & Li, Reference Huang and Li2019; Huang & Murray, Reference Huang and Murray2009; Singh & Agrawal, Reference Singh and Agrawal2011). To the extent that the SOEs’ philanthropy was also influenced by the earthquake, even if the impact was much less, that would make it more difficult to find significant differences between the treatment and control groups. The approach was therefore a conservative one, in that finding a significant effect would suggest stronger support for the hypotheses. The DID estimation compares the difference in the level of philanthropy between private firms (treatment group) and SOEs (control group) before to that difference after the earthquake. The general trends in the philanthropic activities of the two groups are shown in Figures 6a and 6b.

Figure 6. (a) Average donation amount (scaled by total sales) per firm in each year (b) Median donation amount (scaled by total sales) per firm in each year

The treatment group of private firms is matched with a comparable control group of SOEs using coarsened exact matching (CEM) procedure (Iacus, King, & Porro, Reference Iacus, King and Porro2012) based on key observable variables that are considered important criteria in prior research (Armanios, Eesley, Li, & Eisenhardt, Reference Armanios, Eesley, Li and Eisenhardt2017; Feldman, Amit, & Villalonga, Reference Feldman, Amit and Villalonga2019). Consistent with the approach taken by prior studies (Azoulay, Graf-Zivin, & Wang, Reference Azoulay, Graf-Zivin and Wang2010; Singh & Agrawal, Reference Singh and Agrawal2011), the observations in the treatment and control groups are matched based on industry, firm size, and return on assets (ROA) in the corresponding year.

To assess the difference between the treatment group and control group, we examine the L1 distance whereby a smaller distance indicates less difference (Blackwell, Iacus, King, & Porro, Reference Blackwell, Iacus, King and Porro2020). Specifically, the multivariate L1 distance decreases substantially from 0.76 before matching to 0.69 after matching. The L1 distance of each dimension also decreases substantially. Indeed, the L1 distance of firm size decreases from 0.14 to 0.04 and that of firm performance also decreases from 0.08 to 0.05. CEM does not require the number of firms in a treatment group to be equal to that in the matched control group. In the final matched sample, the total number of firms is 1,341 and the average number of years covered in the sample is 9.4. There are 645 private firms (38.21%) and 1,043 SOEs. The empirical results remained similar and consistent when we conduct the matching using year, firm size, firm performance, firm age, or financial leverage. As an alternative test, we use k-to-k matching in which the number in the treatment group must equal that in the matched control group. Using k-to-k matching yields similar and consistent results. As a further check, we conduct regression analyses using the original sample without CEM matching and results are again consistent.

We include firm fixed effects in all of the regression models to account for potential time-invariant, unobserved firm heterogeneity (Greene, Reference Greene1997). Heteroskedasticity-robust and cluster-adjusted standard errors are included in all of the analyses to control for any potential heteroskedasticity. Consistent with the approach used in prior studies (e.g., Low, Reference Low2009), all of our continuous variables are winsorized at the 1% level to eliminate the influence of outliers.

Variables

Dependent variables

The key dependent variable is corporate philanthropy. Consistent with the approach taken by Jeong and Kim (Reference Jeong and Kim2019), it is defined as the amount of firm's yearly donations (in RMB) scaled by its total sales (in thousands of RMB). This dependent variable is measured in year t (2001–2016).

Independent variables

The first independent variable in the DID analyses is private firms, an indicator variable which equals 1 if a firm is ultimately controlled by private owners, and 0 otherwise (Wang & Qian, Reference Wang and Qian2011). The key explanatory variable (i.e., our DID variable of interest) is an indicator variable private firm post-earthquake which equals 1 to indicate private firm ownership in the period after the Wenchuan earthquake from 2008 to 2015 and 0 in the period before 2008. For SOEs, the variable always equals 0. This construction is consistent with that used in prior studies (e.g., Huang & Li, Reference Huang and Li2019; Jia et al., Reference Jia, Huang and Zhang2019; Singh & Agrawal, Reference Singh and Agrawal2011).

Intra-firm pay dispersion is measured as the average annual compensation of a firm's three most highly paid managers divided by the average annual compensation per employee (Connelly et al., Reference Connelly, Haynes, Tihanyi, Gamache and Devers2016). For employee compensation, we exclude members of the top management team and the board because the public pays attention to income disparity between top managers and low-level employees.

Socially contested industries is an indicator variable which takes on the value 1 when a firm operates in socially contested industries and 0 otherwise. For example, firms operating in the finance or real estate industry receive this designation, as do those operating in industries considered highly polluting by China's Ministry of Ecology and Environment (2020): thermal power, steel, cement, electrolytic aluminum, coal, metallurgy, chemicals engineering, petrochemicals, construction materials, papermaking, brewing, pharmaceuticals, fermentation, textiles, leather, and mining. As a robustness check, we add the fur and alcoholic beverage industries to this list following prior studies (Durand & Vergne, Reference Durand and Vergne2015; Koh et al., Reference Koh, Qian and Wang2014; Mawby & Yarwood, Reference Mawby and Yarwood2016) and the empirical results remain consistent.

Foundation number is another independent variable that captures the number of social foundations located in a given province or municipality (divided by 100). The missions of such social foundations cover a broad range of social issues such as environment, poverty, education, and disability. The number of social foundations in a province is a reliable indicator of fund-raising entities because the vast majority of social foundations (73.3%) choose to register with a provincial civil affairs bureau.

Control variables

We include the following control variables in the models to control for a firm's governance attributes and structure (Wang & Coffey, Reference Wang and Coffey1992; Williams, Reference Williams2003). Blockholder ownership is the percentage of shares held by owners each holding at least 5% of a company's shares (Thomsen, Pedersen, & Kvist, Reference Thomsen, Pedersen and Kvist2006). CEO duality is an indicator variable that equals 1 if the CEO also chaired the board and 0 otherwise (Jia et al., Reference Jia, Huang and Zhang2019; Rediker & Seth, Reference Rediker and Seth1995). CEO ownership is the percentage of a firm's shares held by the CEO (He & Wang, Reference He and Wang2009).

We include the following variables to control for firms’ financial characteristics (Buchholtz, Amason, & Rutherford, Reference Buchholtz, Amason and Rutherford1999; Seifert, Morris, & Bartkus, Reference Seifert, Morris and Bartkus2004). Government subsidy is the amount of subsidy a firm receives from government bodies in a given year normalized by total assets. The values are small, so they are multiplied by 100. Financial slack is a firm's current assets divided by its current liabilities (Bromiley, Reference Bromiley1991). Financial leverage is the debt to total assets ratio of a firm (Barnett & Salomon, Reference Barnett and Salomon2006; Jia et al., Reference Jia, Huang and Zhang2019; Seifert et al., Reference Seifert, Morris and Bartkus2004).

We include the following variables to control for firm attributes and resources (Sharfman, Wolf, Chase, & Tansik, Reference Sharfman, Wolf, Chase and Tansik1988; Wang & Qian, Reference Wang and Qian2011). Firm size is defined as the natural logarithm of a firm's total assets. Firm age is the logarithm of the number of years since a firm was founded. ROA is the return on assets of a firm. Industry peer donation is the mean level of corporate philanthropy of industry peers (Cao, Liang, & Zhan, Reference Cao, Liang and Zhan2019). Market index provides a proxy for regional market development using the overall market development indices for China's 31 provinces, municipalities, and autonomous regions published each year by the National Economic Research Institute (Fan & Wang, Reference Fan and Wang2006). Lastly, in addition to firm fixed effects, year and industry fixed effects[11] are included in all of the regression models to control for any potential unobserved heterogeneity across different years of observation and industry sectors. All the independent and control variables are lagged by one year.

RESULTS

Table 1 provides the descriptive statistics and pairwise correlations among the variables. The variance inflation factors (VIFs) in all regressions have a mean of 1.47 and a maximum of 5.58. The variable socially contested industries is the only one with a VIF larger than 5 because of its strong correlation with some of the industry dummies. Dropping the industry dummies, its VIF reduces to 1.25 and the empirical results remain similar. Thus, multicollinearity is deemed not a serious issue in these analyses (O'Brien, Reference O'Brien2007).

Table 1. Summary statistics and correlations among the variables

Notes: N = 12543. Correlation coefficients greater than 0.02 are significant at p < 0.05 level.

Table 2 presents the coefficients of regression models predicting firms’ corporate philanthropy before and after the Wenchuan earthquake. The models include the moderating effects of intra-firm pay dispersion, socially contested industries, and foundation number. Model 1 is a baseline model which includes only the control variables. Model 2 adds private firm post-earthquake as a predictor to the regression model. The model shows that corporate philanthropy increases significantly (p < 0.001) by 69.35% for private (non-SOE) firms after the earthquake, relative to SOEs. This finding provides support for Hypothesis 1a.

Table 2. Coefficients of firm fixed effect models predicting corporate philanthropy

Notes: Robust standard errors clustered by firm are shown in parentheses and p values are shown in braces.

All tests are two-tailed. ***p < 0.001, **p < 0.01, *p < 0.05, †p < 0.1.

Hypothesis 1b suggests that the increase in private firms’ corporate philanthropy persists after 2008. To test it, several subsamples were created by keeping all the observations before 2008 and using observations that cover different time periods after 2008 – that is, (i) 2010–2016; (ii) 2011–2016; (iii) 2012–2016; (iv) 2013–2016; (v) 2014–2016; (vi) 2015–2016; and (vii) 2016 alone. As Models 1 to 7 in Table 3 show, for all of these subsamples, the change in corporate philanthropy was significant and positive. Therefore, Hypothesis 1b is supported. The results of those tests are available on request.

Table 3. Persistence of the earthquake's effect on corporate philanthropy

Notes: Robust standard errors clustered by firm are shown in parentheses and p values are shown in braces.

All tests are two-tailed. ***p < 0.001, **p < 0.01, *p < 0.05, †p < 0.1.

Figures 6a and 6b depict the average and median annual donations per firm over the period studied. They provide corroborating support for Hypothesis 1a and Hypothesis 1b. Figure 7 shows a standard DID temporal graph using the estimated temporal impact of the sudden event on donation amount. No significant pre-trends on corporate donations are observed before the 2008 earthquake. After the earthquake, there is a significant increase in donation amount and the amount stays at a higher level than before the earthquake.

Figure 7. Estimated temporal impact of the sudden event on donation amount

In Table 2, Model 3 tests for the interaction effect between private firm post-earthquake and intra-firm pay dispersion. The coefficient suggests a significant (p < 0.05) and positive effect of 81.39%. Thus, Hypothesis 2 is supported. Model 4 in Table 2 tests for the interaction effect between private firm post-earthquake and socially contested industries. The result shows a significant (p < 0.001) and positive effect of 67.36%. Therefore, Hypothesis 3 is supported. Model 5 includes the interaction term between private firm post-earthquake and foundation number in a province. The result suggests a significant (p < 0.05) and positive effect of 82.01%. Thus, Hypothesis 4 is supported. As an additional check, Model 6 includes the three sets of interaction terms (described above), control variables as well as firm fixed effects, year fixed effects and industry fixed effects. The results are consistent with those shown in Models 2 to 5, providing further support for Hypothesis 1a, Hypothesis 2, Hypothesis 3, and Hypothesis 4. Model 7 is similar to Model 6 except it does not include industry fixed effects. The results are again similar and consistent with those shown in Models 2 to 6.

Alternative Explanations and Robustness Analyses

A few events occurred around 2008 which could have confounded the analyses in our study. One event in 2008 was the hosting of the Beijing Olympic Games. There was evidence (Tilcsik & Marquis, Reference Tilcsik and Marquis2013) that corporate donations may increase before and after mega-events. Around the Olympics Games corporate donations were more for marketing, promoting brands, and corporate reputations. It unlikely drew public attention to the grieving social problems motivating social movements. In addition, although the Olympic Games might partially explain an increase in corporate philanthropy (Hypothesis 1a), the event's influence was expected to wane quickly (Tilcsik & Marquis, Reference Tilcsik and Marquis2013). The Olympics Games then could not explain the persistence of the increase (Hypothesis 1b) and the observed moderating effects (Hypothesis 2–Hypothesis 4). This conclusion was further validated in our interviews with the CEOs of several Chinese manufacturing firms. They believed that the Olympics Games might have affected corporate philanthropy around the period of the Olympics Games but not long afterward.

The financial crisis in 2008 is another potential source of influence. At the time, the Chinese government provided a ¥4 trillion economic stimulus package (SINA, 2020) which might have enabled some firms to increase their donations after 2008. To address this potential concern, we have controlled for government subsidy in all of the regression models. Although the financial crisis led to government interventions in several countries (Dale, Reference Dale2012; Watkins, Reference Watkins2017), it seems unlikely that a financial crisis would impel more corporate philanthropy in general. Unlike an earthquake which impacts primarily the finances of firms in the earthquake-affected region, the financial crisis negatively affects the majority of businesses on a much larger scale. It would deplete firms’ resources available for corporate philanthropy. Therefore, linkage between financial crisis and corporate philanthropy should be weak. In fact, China was not as badly affected by the financial crisis as many other economies. Although one may blame over-commodification as a cause of financial crisis, such sentiment was not widely expressed in China. A keyword search using both ‘financial crisis’ and ‘corporate philanthropy’ yields articles mostly about the negative impact of the financial crisis on corporate philanthropy due to firms’ difficult financial situations. There is little or no internet activism that linked the financial crisis to corporate donations (e.g., Luo et al., Reference Luo, Zhang and Marquis2016). Thus, the financial crisis did not generate widespread discussion of or reflection on social problems and the potential role of business in solving these problems as the earthquake did. In sum, we think that only the earthquake event generated enough public attention to and the social pressure on corporate philanthropy.

The finding that philanthropic donations significantly increase after the earthquake was based on a relatively long 15-year window. To ensure that the findings are robust, additional analyses use windows (subsamples) with observations three, four, and five years before and after 2008. The coefficients of variables of interest in these analyses remain consistent and highly significant, which strongly support Hypothesis 1a.

We also conducted logit regressions with corporate philanthropy as an indicator variable, where a value of 1 indicated a firm which engaged in any corporate philanthropy at all and 0 indicated those which did not. These regressions show that the likelihood of firms’ making donations increases significantly after the earthquake, further supporting Hypothesis 1a. Socially contested industries and the foundation number in a region also strongly and positively moderate the main relationship in these logit regressions.

In addition, donations scaled by a firm's total assets are employed as an alternative dependent variable and all the empirical results for the three hypotheses remained the same. We also tested two alternative measures for intra-firm pay dispersion. The first measure uses the average compensation of all top managers and directors divided by the average compensation of all the other employees. The second measure is intra-firm pay dispersion divided by the industry's median dispersion. The significant and positive moderating effects persisted, providing support for H2. To quantify the extent to which the Chinese public is aware of the intra-firm pay dispersion, we search and analyze the comments related to ‘income disparity between the managers and the employees’ in China's major online forums. Nine of the top ten comments discussed intra-firm pay dispersion, and some of them attracted hundreds of responses, suggest that the general public is well aware of the pay disparities in companies.

Finally, to rule out the effect of the central government's policy of ‘Scientific Outlook on Development’ starting from 2003, observations before 2003 are removed to rerun the regressions. The results remain consistent with those reported.

DISCUSSION

Based on the double movement perspective (Polanyi, [1944] Reference Polanyi2001), this study examines the effect of the Wenchuan earthquake that has accelerated the development of a countermovement in China, favoring a more embedded economy. We argue that the level of countermovement and its pressure on firms are contingent on the intra-firm pay disparities, whether or not these firms operate in socially contested industries and regardless the number of social foundations in a region. The empirical analyses find results consistent with those predictions.

This study makes several contributions to our understanding of the motivations underlying corporate philanthropy. The findings extend previous scholarship on the short-term influence of sudden events on firm philanthropy to a much longer time scale. Prior research has explored various antecedents of firms’ short-term philanthropic donations for the relief of disaster, including whether the firm was targeted by internet activists and the concerns over firm reputation (Luo et al., Reference Luo, Zhang and Marquis2016; Zhang & Luo, Reference Zhang and Luo2013). Other studies have explored the short-term consequences such as the investor or shareholder reactions to a firm's philanthropy for the relief of disasters (Muller & Kräussl, Reference Muller and Kräussl2011; Shu & Wong, Reference Shu and Wong2018). There has even been limited scholarly examination of how sudden events can bring changes to corporate philanthropy three or four years after a disaster by affecting community identification of a firm's decision-makers (Tilcsik & Marquis, Reference Tilcsik and Marquis2013). However, there is a lack of a systematic examination of persistent influence of such events on organizational field and firm behavior. This study fills that gap.

Comparing this work with that of Tilcsik and Marquis (Reference Tilcsik and Marquis2013) indicates that the effect of sudden events is contextual. It has been shown that a large-scale event may have a strong and persistent impact when corporate philanthropy has not yet been institutionalized in a context like China. In developed economies where CSR is more institutionalized (Flammer, Reference Flammer2013), sudden events may not bring such strong and persistent effects on corporate philanthropy because less social and structural change would be involved (Tilcsik & Marquis, Reference Tilcsik and Marquis2013). As such, this study advances our understanding of the antecedents of corporate philanthropy by examining sudden events and their institutional context. The findings from this study should be applicable in other contexts where the institutional foundations for corporate philanthropy are poorly developed, or where the tension between embedding and disembedding forces is strong.

In addition, these findings enhance our understanding of the multiple roles of sudden events in affecting firms’ philanthropic behavior. Prior studies have shown that sudden events can affect corporate philanthropy through mechanisms such as triggering community identification (Tilcsik & Marquis, Reference Tilcsik and Marquis2013), internet activism, and damage to a corporation's image (Luo et al., Reference Luo, Zhang and Marquis2016; Zhang & Luo, Reference Zhang and Luo2013). Indeed, they can also provide opportunities for reputation gains (Muller & Kräussl, Reference Muller and Kräussl2011). This study extends that understanding by incorporating the double movement perspective and emphasizes the long-term change in social context and attitudes of the public and a firm's stakeholders, resulting in the long-term effects on corporate philanthropy.

This study applied the double movement approach in a new area. Studies using this theoretical perspective have previously focused on countermovement pressure from governments, NGOs, the public, and the media (Bandelj et al., Reference Bandelj, Shorette and Sowers2011; Dale, Reference Dale2012; Levien, Reference Levien2007; Reisman, Reference Reisman2019; Watkins, Reference Watkins2017), but how the pressures affect firms’ behavior in a disembedded economy has been largely ignored. This study fills this gap in terms of corporate philanthropy in China. Moreover, we have shown that the effects of a countermovement are conditional on firm-level, industry-level, and region-level factors.

Incorporating the double movement approach to corporate behavior may help explain changes of organizational fields and organization practices from a new perspective. While the literature has shown that factors such as customer demands, efficiency, autonomy, and inter-organizational networks may lead to institutional changes and formation of new organizational practices (Davis, Diekmann, & Tinsley, Reference Davis, Diekman and Tinsley1994; Greenwood & Suddaby, Reference Greenwood and Suddaby2006; Huybrechts & Haugh, Reference Huybrechts and Haugh2017; Rao, Monin, & Durand, Reference Rao, Monin and Durand2003), less attention has been paid to how the infighting between disembedding and re-embedding forces leads to such changes in corporate behaviors. While this study has linked this perspective to changes in corporate philanthropic behaviors, future research may explore other relevant corporate behaviors, especially in China where the opposing forces of disembedding and re-embedding are salient and dynamic. For instance, future research may pay attention to how firms and stakeholders respond to environmental sustainability such as carbon neutrality under such a perspective. Researchers may also look into how firms establish practices to reduce corporate misconducts such as unfair employee treatment when re-embedding forces advocate more social protections of the stakeholders and general public. While digitalization and platform firms develop quickly in China these years, they bring serious problems such as digital addiction and data monopoly. Thus, how re-embedding forces affect societal attitudes toward such firms can be an interesting research question.

Previous studies have analyzed shocks such as the Great Depression of the 1930s and the 2008 financial crisis, viewing them as endogenous and having been triggered by disembedding in society (Dale, Reference Dale2012; Polanyi, [1944] Reference Polanyi2001; Watkins, Reference Watkins2017). Much less attention has been paid to the effects of an exogenous shock such as a natural disaster on countermovement development in a specific domain. This study has extended the application of the double movement perspective to such exogenous sudden events. By linking the sudden events to the embedding and disembedding movement in terms of their effects on corporate behaviors, this study sheds lights on the underlying mechanisms through which companies continuously interact with social and institutional environments. The study also illustrates that the double movement perspective can be a useful lens for stakeholders’ analysis through which firm behaviors can be better understood. Future studies can extend the direction of inquiry and investigate, for example, how firms or their stakeholders drive the embedding or disembedding movement, or how other types of events (e.g., US-China trade conflicts, COVID-19 pandemic, or Ukraine wars) can affect this process.

Managerial and Policy Implications

The findings suggest some practical implications for firm managers. Chinese firms should pay greater attention to countermovement trends in society and their demands with respect to corporate social behavior in order to avoid destructive criticism, damage to the firm's image, or even social punishment. This is especially pertinent for firms with activities or features which draw attention such as those with a high level of intra-firm pay disparity or operating in polluting industries. Our study shows that the effect on corporate philanthropy can persist in the long run, and it would be naive for a manager attempting to treat this as a short-term effect or restore philanthropical actions to the pre-crisis level. Managers should recognize that a new normal might have emerged after the sudden events and enable the firm to adapt. The recent philanthropic behavior of Chinese firms seems consistent with this suggestion. Three weeks after the COVID-19 epidemic broke out in China in 2020, Chinese firms had donated ¥16.65 billion, amounting for 83% of the total donations (TENCENT, 2020). In comparison, half a year after the outbreak of severe acute respiratory syndrome in 2003, Chinese firms and individuals together had donated only ¥2.74 billion for the relief of SARS (Bai, Reference Bai2003). In sum, managers should pay attention to sudden events that can have persistent and long-term impacts on their firms and stakeholders.

These findings also have policy implications for governments. To begin with, governments should try to be as adaptive as firms when sudden events occur which can change deep-rooted social structure and public opinions. Policymakers in the Chinese government should pay particular attention to the countermovement as they try to mobilize resources to achieve societal goals such as the current emphasis on ‘common prosperity’. Governments may prioritize their attention and policy development efforts in accordance with embedding forces. For example, they could set up regulations to encourage firms in high-income sectors to donate more to society. Meanwhile, as this study shows, social change and movement could be uneven in different domains or areas (e.g., strong pressure on firms with income disparity issues or those in polluting industries but weak pressure on other firms). Thus, governments should reduce such unevenness by directing public attention to those firms with weak pressure and thus encouraging their corporate philanthropy.

Moreover, this study shows the critical role played by social media and general public. With the intensified digitalization efforts in China, policymakers may consider building up credible platforms to encourage public voice on topics such as CSR or how to realize ‘common prosperity’. People can contribute innovative insights on such topics, and the government can provide the media outlet and infrastructure for the general public to participate in such social movements. In addition, as our study highlights, governments could further encourage the development of social foundations in a region. This could stimulate corporate donations targeting social issues. Lastly, policymakers may leverage the social trends and pressures to reduce corporate misconducts such as environmental pollutions and mistreatments of female employees.

Limitations and Future Research Directions

This study has a few limitations which could suggest potentially fruitful avenues for future research. First, while the current study has focused on corporate philanthropy, other corporate social behavior may also have changed after the earthquake. Legitimacy spillover could be an interesting area to explore. Future research might examine how a sudden change in one aspect of an organization's environment might lead to the evolution in several related areas. This study focuses on pay disparities and polluting industries. Future studies might usefully explore other firm characteristics that may be associated with concerns about production safety, food safety, and other pressing social issues.

Second, we acknowledge that the control group in our DID analyses is not perfect because some SOEs could be more profit-driven than commonly assumed as they could also emphasize efficiency and market-orientation. To the extent that SOEs are typically less attuned to market demands and public opinion than private firms, they make reasonably suitable control group in this study. Nevertheless, future research might consider choosing other contexts and thus control group of firms or individuals to explore the utility of the double movement perspective for explaining firm behavior and understanding causal relationships.

CONCLUSION

Applying the double movement perspective, this study has provided empirical evidence that the Wenchuan earthquake increased firms’ philanthropy in China over the long term. In addition, it has shown that the long-term effect of the earthquake on corporate philanthropy depends on intra-firm pay disparities, the industry in which a firm operates and number of social foundations in the provincial region the firm is located.

DATA AVAILABILITY STATEMENT

Replication code for this article has been published in Open Science Framework at: https://osf.io/x8f46/